Email

Email Print

Print

Automotive Connector Market - Forecast(2024 - 2030)

Overview

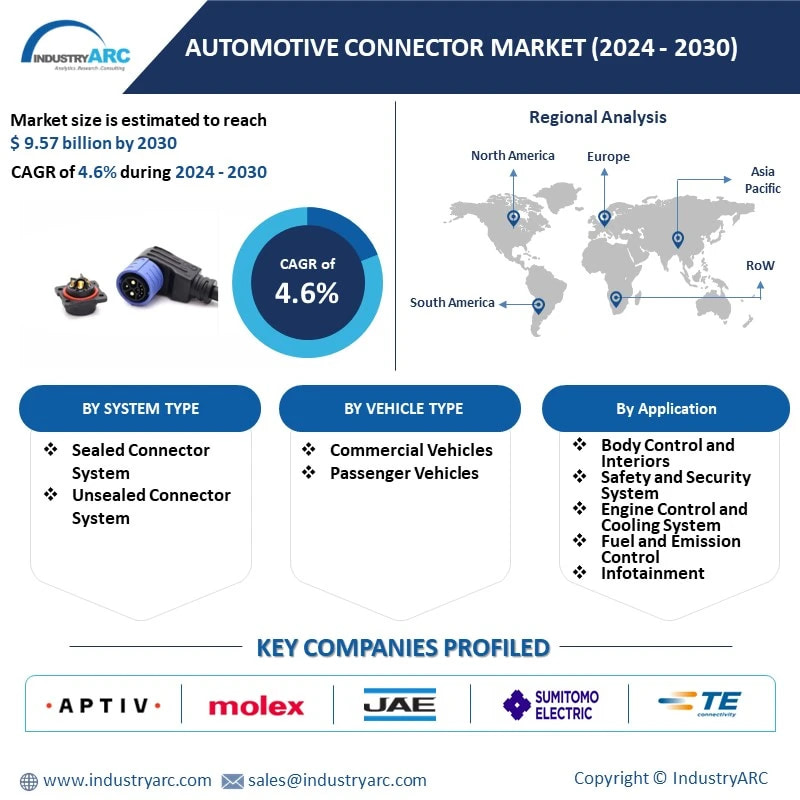

The Automotive Connector Market size was valued at USD 6.42 Billion in 2023 and is likely to reach USD 9.57 Billion by 2030, expanding at a CAGR of 4.60% during the forecast period, 2024–2030. The growth of the market is attributed to increasing demand for convenience, connectivity, and safety features in commercial vehicles as well as passenger cars Advancements in technology have resulted in many features that provide better safety and enhance the driving experience. An automotive electrical connector refers to a device that connects electrical terminations to form a circuit. Increasing consumer safety issues, combined with security-related measures from government agencies has elevated the need for a reliable connector in different vehicle systems. For example, safety devices such as seatbelts, airbags, and brakes used in automobiles include a connection system that requires a retainer and system connector for safety restraints. The growing demand for automotive safety systems thus has a direct effect on the demand for automotive connectors, particularly sealed connector systems, which in turn drives market growth. In addition, the use of electronics in other applications, such as advanced and convenient systems such as automatic transmissions and infotainment, has also increased. Which, in turn, drives the demand for automotive cable harnesses in automobiles, thereby boosting the need for connectors in these systems and this helps in the growth of the market of automotive connectors. The rising adoption of wire-to-wire connectors and printed circuit boards (PCB) device connections will drive market growth. Increasing consumer safety issues, combined with security-related measures from government agencies has elevated the need for a reliable connector in different vehicle systems. For example, safety devices such as seatbelts, airbags, and brakes used in automobiles include a connection system that requires a retainer and system connector for safety restraints. The growing demand for automotive safety systems thus has a direct effect on the demand for automotive connectors, particularly sealed connector systems, which in turn drives market growth. In addition, the use of electronics in other applications, such as advanced and convenient systems such as automatic transmissions and infotainment, has also increased. Which, in turn, drives the demand for automotive cable harnesses in automobiles, thereby boosting the need for connectors in these systems and this helps in the growth of the market of automotive connectors. The rising adoption of wire-to-wire connectors and printed circuit boards (PCB) device connections will drive market growth.

The report: “Automotive Connector

Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth

analysis of the following segments of the Barium Sulphate Industry. Market.

By System Type: Sealed Connector System, Unsealed Connector System.

By Vehicle Type: Passenger Cars, Commercial Vehicles

By Application: Body Control and Interiors, Safety and Security System, Engine

Control and Cooling System, Fuel and Emission Control, Infotainment, Navigation

& Instrumentation, Others.

By Geography:

North America, South America, Europe, APAC,

and RoW.

Market Snapshot:

Key Takeaways

- Growing consumer

safety concerns, coupled with government agencies' protection initiatives,

have elevated the need for a reliable connector in various vehicle

systems.

- The adoption of

automobile safety and security systems is expected to increase with

growing regulations for vehicle safety specifications in Europe, resulting

in increased demand and usage of connectors over the forecast period.

- The growing adoption

of electronic content in modern vehicles is one of the key factors

expected to drive growth in demand in the years ahead. With the growing

electrification of mechanical components the automotive industry has seen

increased adoption of electronics solutions.

- The development of

combined connector technology and the growing adoption of electronic

content are some of the important reasons which reinforce the growth of

the automotive connector market.

By Geography - Segment Analysis

Asia-Pacific

region dominated the Automotive Connector Market share by 40 % in the year 2023,

the Asia Pacific region led the market by generating the highest revenue share.

Asian nations, including China, Taiwan, and Japan, are the primary

manufacturers of electronic components for both passenger and commercial

vehicles. Due to the availability of low-cost labor, improved manufacturing

facilities, and convenient access to raw materials, the region is a hub for

exporting various types of automotive parts.

the Asia Pacific region led the market by generating the highest revenue

share. Asian nations, including China, Taiwan, and Japan, are the primary

manufacturers of electronic components for both passenger and commercial

vehicles. Due to the availability of low-cost labor, improved manufacturing

facilities, and convenient access to raw materials, the region is a hub for

exporting various types of automotive parts.Asian countries such as China,

Taiwan, and Japan are leading manufacturers of electronic components for both

passenger cars as well as commercial vehicles. The region is an export hub for

various types of automotive parts, owing to availability of low-cost labor,

enhanced manufacturing facilities, and ready availability of raw material.

For More Details on This Report - Request for Sample

End

Use - Segment Analysis

The dominance of the market was primarily influenced by the sales of passenger cars. Anticipated increases in car sales in countries such as India and China are expected to be key drivers for market expansion. In contrast, the commercial vehicles sector, encompassing large trucks, buses, and smaller commercial vehicles, is projected to witness substantial growth by 2030. This growth is attributed to heightened safety regulations for commercial vehicles. The passenger cars segment held the market stronghold in 2022, securing the highest share of revenue. Connectors play a pivotal role in fostering communication among safety systems, including airbags, anti-lock braking systems (ABS), electronic stability control (ESC), and collision avoidance systems. These systems heavily depend on the exchange of precise and timely data to enhance passenger safety. The expansion of this market segment is attributed to the surging sales of passenger vehicles. Due to the shifting focus on consumers from conventional vehicles to modern connected vehicles, the passenger cars segment dominated the growth of the global automobile connectors market. Growing passenger vehicle demand in developing and developed countries is expected to drive the segment's revenue growth over the forecast period. Increasing automobile sales are expected to boost market growth in developing countries such as India and China.

Automotive Connector Market Segment Analysis

– By Application

The navigation segment is anticipated to exhibit the highest CAGR of 9.8% from 2024 to 2030. Increasing accuracy of GPS-enabled devices and implementation of advanced software such as Apple Carplay and Android Auto has fostered the use of navigational applications in both commercial and passenger vehicles. Increasing the adoption in the vehicle of GPS-enabled devices and advanced navigation software is expected to help the growth of this market over the forecast period. Increasing accuracy of GPS-enabled systems and advanced software implementation such as Apple Carplay and Android Auto have facilitated the use of navigational applications in both commercial and passenger vehicles and thus it is expected to boost the market growth of automotive connectors.

Automotive Connector Market Drivers

Growing adoption of electronic contents in modern vehicles

The rising adoption of electronic content in modern vehicles is one of the main factors that are expected to stimulate demand growth in the years ahead. The automotive industry has seen increased adoption of electronics solutions with the increasing electrification of mechanical components. Electronic manufacturers have witnessed increasing demand for high-speed wiring, connectors, and other electronic technology in modern vehicles to allow telematics and infotainment systems. Technologies such as copper connectivity solutions are also gaining prominence because of lower weight and more options for connectivity within the vehicle. Advanced automotive systems use memory and data storage connectors in connected vehicles to support new Wi-Fi capabilities. Growing electronic content in vehicles will help fuel Automotive Connector market growth.

Development of combined connector technology

The development of combined connector technology is one of the main trends that are expected to gain market traction. This technology improves the ability to maintain wire and to connect PCBs to provide robust resistance to extreme temperatures, shock, vibration and long lifetime thermal expansion. Combined connectors are also more reliable than conventional cables for connecting two nearby PCBs but not in the same orientation or location of alignment. The development of this technology is also expected to meet the growing demand for reliable and efficient connectors in harsh environments for automotive applications. The development of combined connector technology and the increasing adoption of electronic content are therefore some of the important reasons that strengthen the growth of the market for automotive connectors.

Increasing Advancement in Infotainment System

The increasing incorporation of advanced security features in automobiles, as well as the rising demand for electric vehicles (EVs), is the primary factor driving the market growth. Furthermore, the increasing sophistication of automotive sensors and infotainment systems has increased the global demand for automotive wiring harnesses and connectors. Plastic optical fiber (POF) is replacing copper cables in automobiles to improve data transmission and design flexibility while also reducing overall vehicle weight. POF requires automotive connectors to function properly.

In addition to this, the evolution of air conditioning systems and HVAC systems, owing to technological proliferation, is expected to favorably impact connectors' growth during the forecast period. Major players in the market are manufacturing the connectors and entering acquisitions to meet the features in the vehicles.

Challenges –

To meet reliability and durability standards:-

The automotive connector market faces the ongoing challenge of meeting heightened expectations for reliability and durability, primarily due to the increasing integration of heavy electronic components in modern vehicles. With advancements in automotive technology, vehicles are equipped with sophisticated electronic systems for monitoring vital functions such as airbags, GPS navigation, engine control units, and various sensors The rising complexity of electronic components in vehicles poses a challenge for manufacturers. Connectors play a critical role in ensuring the seamless functioning of these systems, and meeting the demand for increased electronic integration requires robust and reliable connector solutions. Vehicles operate in diverse environmental conditions, including temperature variations, vibrations, and exposure to moisture. Connectors need to be durable enough to withstand these conditions and maintain performance over an extended period.2024 -2030.

Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in Automotive Connectors Market. Automotive Connectors Market is expected to be dominated by major companies such as Aptiv, Molex, Japan Aviation Electronics Industry, Sumitomo Electric Industries, TE Connectivity, Yazaki, Amphenol Corporation, J.S.T. Mfg. Co. Ltd, Delphi Technologies

Developments:

Ø In On January 2023, Mouser Electronics,Inc., an authorized global distributor of the rearmost semiconductors and electronic factors, announced a new distribution agreement with YAZAKI Corporation North America, a leading manufacturer of connectors, and numerous other quality products for the automotive assiduity.

Ø On September 2022,

TE Connectivity (TE), a world leader in connectivity and sensors, has developed

the PicoMQS small automotive connector system. The PicoMQS connector is

designed for tight signal connections that require automotive durability,

optimized performance.