Email

Email Print

Print

Synthetic Resin Market Overview

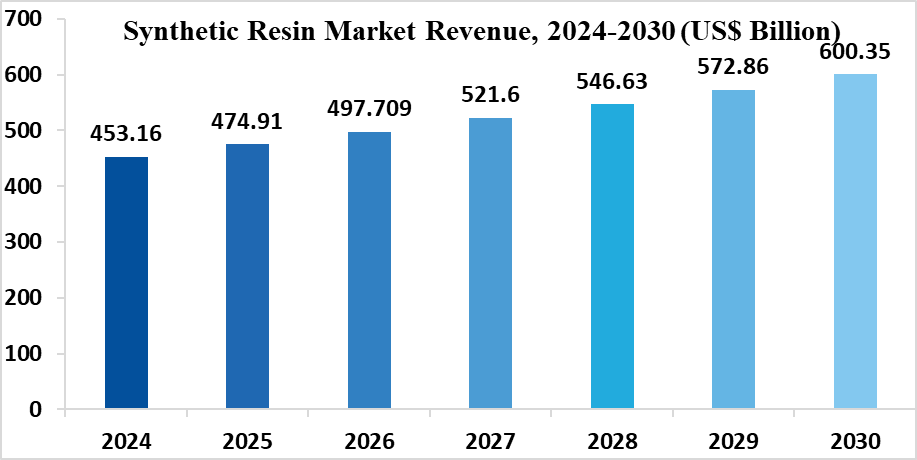

The Synthetic Resin Market size is projected to reach a value of US$600.35 billion by the end of 2030 after growing at a CAGR of 4.8% during the forecast period 2024-2030. A synthetic resin is a chemical substance that is synthesized to closely resemble the properties of its natural counterpart. Synthetic resins based on polyethylene, polyvinyl chloride, formaldehyde, aliphatic, and glycidyl amine occur in a wide range of products, such as plastics, paints, and varnishes. Products that are manufactured with synthetic resins provide better long-term corrosion protection of metal substrates because of their increased durability, owing to which its market demand is being spurred. The growth can be attributed to the increasing demand for paints, coatings, adhesives, and sealants from the bolstering building and construction industry across various regions globally. However, the increasing adoption of bio-based resins as an eco-friendly alternative over the coming years is anticipated to impede the global synthetic resins market growth over the forecast period.

Synthetic resins, which are either derived from plant sources or synthetically manufactured in laboratories, are extensively used in these industries. However, the rise of bio-based resins as an eco-friendly alternative could potentially impede the growth of the synthetic resins market. Despite the challenges, the market presents opportunities for innovation, particularly in the development of bio-based resins. It’s always a good idea to conduct your own research or consult with a market research professional for more detailed insights.

Synthetic Resin Market COVID-19 Impact

The COVID-19 epidemic negatively impacted the synthetic resin demand in a variety of end-use industries, including automotive, aerospace, construction, and more. Due to the closure of non-essential businesses, the outbreak had a significant impact on the aerospace, automotive, and construction industries. As demand for automobiles and aircraft dwindled, production was abruptly halted. For instance, according to the International Organization of Motor Vehicle Manufacturers, global automotive production will fall by 16 percent in 2020. Due to the impact of the COVID-19 pandemic, Toyota Motor Corporation's global vehicle manufacturing in 2020 was flat at 12.6 percent year over year. Furthermore, during the pandemic, construction output was drastically decreased. However rapid industrialization in emerging economies, is expected to drive the demand for synthetic resins. The growth of industries such as automotive, construction, and packaging in these regions is likely to contribute to market growth. In conclusion, the synthetic resin market is expected to witness significant growth in the coming years, driven by increasing demand from various end-use industries, technological advancements, and the trend towards sustainability.

Report Coverage

The report: “Synthetic Resin Market Report – Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments of the Synthetic Resin Market.

By Form: Solid, Liquid, Emulsion, and Dispersion.

By Type: Thermosetting Resins (Polyester, Vinyl Ester, Epoxy, Phenolic, Urethane, and Others), and Thermoplastic Resins (Polycarbonate, Acrylic, Nylon, Polyethylene, Polyvinyl Chloride, Polyethylene Terephthalate, Polypropylene, Polybutylene Terephthalate, Vinyl, and Others).

By Application: Packaging, Printing Inks, Pipes & Hoses, Walls & Floors, Wood Finishes, Sheets & Films, Medical Devices, Paint & Coatings, Adhesives & Sealants, Electronic Fabrications, Transportation Components, and Others.

By End-use Industry: Transportation (Automotive, Aerospace, Locomotive, and Marine), Food & Beverage (Fruits & Vegetables, Dairy, Bakery, Confectionery, Poultry, Drinking Water, Soft Drinks, and Others), Personal Care & Cosmetic (Body Care, Face Care, Eye Care, Nail Care, Fragrances, and Others), Building & Construction (Residential, Commercial, Industrial, and Infrastructural), Oil & Gas (On-shore, and Off-shore), Energy Generation (Wind Energy, Solar Energy, and Others), Electrical & Electronics (Generators, Transformers, Circuit Breakers, and Others), Military & Defense (Helmets, Bulletproof Jackets, and Others), Medical & Healthcare (Connectors, Surgical Equipment, Blood Reservoirs, and Others), and Others.

By Geography: North America (USA, Canada, and Mexico), Europe (UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia, and Rest of APAC), South America (Brazil, Argentina, Colombia, Chile, and Rest of South America), Rest of the World (the Middle East, and Africa).

Key Takeaways

• Asia-Pacific dominates the Synthetic Resin Market, owing to the increasing transportation and construction industry in the region. The increasing per capita income and evolving lifestyle of individuals coupled with the rising population are the major factors expanding the transportation and construction industry in APAC.

• Excellent properties such as toughness, resistance to several environmental factors, stability, and flame resistance, are making synthetic resin more popular in the electrical and electronics industries for manufacturing components such as printed circuit boards, electrical encapsulation circuits, components, and assembly materials.

• Synthetic resins are being used in the oil & gas industry as they are an ideal match for the challenges of withstanding high-pressure, high-temperature environments. Thermoset resins have excellent thermal stability in high-pressure and high-temperature environments, allowing for more modular and robust product offerings with longer service existences.

• However, increasing the adoption of bio-based resins over synthetic resins on account of their eco-friendly nature is acting as a major challenge for the global synthetic resins market during the forecast period

For More Details on This Report - Request for Sample

Synthetic Resin Market Segment Analysis – by Type

The thermoplastic resins segment held the largest share in the Synthetic Resin Market in 2023 and is forecasted to grow at a CAGR of 4.9% during the forecast period 2024-2030. Reheating, remolding, and cooling thermoplastics without causing chemical changes is possible. The primary benefit of thermoplastics is their broad range of uses. Thermoplastics are materials with high strength, low weight, and low processing costs. Furthermore, thermoplastic materials are relatively simple to manufacture in large quantities and with high precision. Thus, all these advantages associated with thermoplastic resins are majorly contributing to its segment growth. However, the main disadvantage of using thermoplastics instead of metals is that they have a lower melting point. When low-quality thermoplastics are exposed to the sun for long periods, they can melt. This factor is restricting the thermoplastic resin segment growth over the forecast period.

Synthetic Resin Market Segment Analysis – by End-use Industry

The transportation segment held a significant share in the Synthetic Resin Market in 2023 and is forecasted to grow at a CAGR of 5.6% during the forecast period 2024-2030, owing to the increasing usage of synthetic resins in the transportation component. The transportation industry demand high-reliability synthetic resins. Synthetic resins are known to provide excellent mechanical strength, structural support, and durability. The synthetic resin manufactured components withstand the initial impact force of installation, as well as the repeated stress of inspections and repairs. They also have high shear, compressive, flexural, and tensile strength to withstand the stresses of takeoff, flight, and landing. Synthetic resins even exhibit high strength at elevated operating temperatures and also provide insulation from heat when used to separate two components due to which they are extensively used in the transportation sector. Moreover, synthetic resins offer excellent electrical insulation properties and low toxicity/burn characteristics which minimize the damage and risk in the case of fire or explosion. Due to all these extensive characteristics of synthetic resins, it is being widely used in the transportation sector, which is anticipated to drive the Synthetic Resin Market during the forecast period.

Synthetic Resin Market Segment Analysis – by Geography

Asia-Pacific region held the largest share in the Synthetic Resin Market in 2023 up to 45% and is forecasted to grow at a CAGR of 6.2% during the forecast period 2024-2030, owing to the increasing transportation industry in APAC countries. According to the Japan Automobile Manufacturers Association (JAMA), automobile production in Japan increased in November from 6,67,462 units in October to 6,90,311 units. Thus, the growth of the global Synthetic Resin Market in the region is being aided by the increasing transportation sector in APAC, thereby dominating the market in the Asia-Pacific region.

Synthetic Resin Market Drivers

Government Initiatives Bolstering the Growth of the Building & Construction Sector

Government initiatives are playing a crucial role in bolstering the growth of the building & construction sector, which in turn is driving the synthetic resin market. These initiatives include support for green construction, post-pandemic recovery efforts, and infrastructure development.

Synthetic resin-based paints, coatings, adhesives, and sealants are often employed in residential buildings in applications such as windows, walls, doors, floors, and more. The governments are taking initiatives to increase building & construction activities. For instance, Kansai International Airport in Japan will spend about 100 billion yen ($911 million) by 2025 to upgrade the larger terminal, to increase space for international flights at the country's No. 2 hub. A fraction of this budget will go toward the planning and construction of the Limpopo Central Hospital in Polokwane, which is set to open in 2025/26. The Ministry of Housing and Urban Development (MoHUA) has been given Rs 50,000 crore (US$6.8 billion), and a fund of Rs 25,300 crore (US$3.5 billion) has been set up to help complete stalled housing projects. Such government initiatives are set to increase the demand for paints, coatings, adhesives, and sealants in the residential construction sector, and further drive the Synthetic Resin Market growth during the forecast period.

Bolstering Growth of Personal Care & Cosmetics and Food & Beverages Sector

Synthetic resins are often used to manufacture packaging materials for various end-use industries such as food, cosmetics, pharma, and more. Due to rising consumer demand and increasing per-capita income of individuals, the personal care & cosmetics and food & beverage industry is booming in various regions. According to the India Brand Equity Foundation (IBEF), the beauty, cosmetics, and grooming market in India in 2025 will have grown from US$6.5 billion to US$20 billion. According to the International Trade Administration, Thailand's beauty and personal care goods market was valued at around US$8.21 billion in 2023 and is projected to grow to US$10.45 billion by 2030. Since the personal care & cosmetics and food & beverage sector industries are booming, the demand for packaging is also significantly increasing. Thus, the increasing personal care & cosmetics and food & beverage sector act as a driver for the synthetic resins market during the forecast period.

Synthetic Resin Market Challenge

Shift Towards Bio-based Resins

Many resin manufacturers have shifted away from synthetic resins to bio-based resins due to the globalization of the economy, increased awareness of carbon footprints, increased emphasis on sustainable systems, and the evolution of product lifecycle analysis. Bio-resins have a lot of potential. They reduce reliance on petrochemicals and allow manufacturers who use them to promote greener products due to price volatility. Furthermore, they have a better entire life cycle than petrochemical-based resins, with a lower carbon footprint, lower manufacturing toxicity, and less reliance on fossil fuels. Businesses are constantly launching bio-resins in the market as a result of this shift. SABIC, for example, launched a new portfolio of bio-based ULTEMTM resins in Saudi Arabia, which offers sustainability benefits while delivering the same high performance and processability as incumbent ULTEM materials. These ground-breaking polyetherimide (PEI) materials are the industry's first certified renewable high-performance, amorphous polymers. Thus, such advantages of bio-based resins over synthetic counterparts and constant product launches of bio-based resins are anticipated to restrict the Synthetic Resin Market growth.

Synthetic Resin Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the Synthetic Resin Market. Synthetic Resin Market's top 10 companies are:

- Sinopec Group (China Petrochemical Corporation)

- Covestro AG

- Jiangsu Sanmu Group

- SABIC

- The Dow Chemical Company

- Nan Ya Plastics Corporation

- Kukdo Chemical Co. Ltd.

- Huntsman Corporation

- Formosa Petrochemical Corporation

- BASF SE and others

Acquisitions/Technology Launches

• In January 2023 BASF acquired the polyamide business of Solvay for €1.6 billion. This acquisition strengthens BASF's position in the engineering plastics market, particularly in high-performance polyamides.

• In March 2023 Eastman Chemical Company acquired the coatings additives business of AkzoNobel for $1.4 billion. This acquisition expands Eastman's portfolio of performance additives used in paints and coatings.

• In July 2023 LyondellBasell Industries acquired the polyolefins business of A. Schulman Inc. for $2.25 billion. This deal strengthens LyondellBasell's position in the polyolefins market, particularly in polypropylene and polyethylene.

• In October 2023 SABIC acquired the specialty resins and chemicals business of Dow Chemical for $5.4 billion. This acquisition expands SABIC's portfolio of high-performance polymers and specialty chemicals.

• In December 2023 Chevron Phillips Chemical Company acquired the olefins and derivatives business of Nova Chemicals for $5 billion. This deal expands Chevron Phillips's position in the ethylene and polyethylene markets.

• In January 2024 Dow Chemical acquired the silicones business of DuPont for $3.8 billion. This acquisition expands Dow's portfolio of silicone-based materials used in a variety of applications.

For more Chemicals and Materials Market reports, please click here

1. Synthetic Resin Market - Market Overview

1.1 Definitions and Scope

2. Synthetic Resin Market - Executive Summary

2.1 Key Trends by Form

2.2 Key Trends by Type

2.3 Key Trends by Application

2.4 Key Trends by End-use Industry

2.5 Key Trends by Geography

3. Synthetic Resin Market – Comparative analysis

3.1 Market Share Analysis - Major Companies

3.2 Product Benchmarking - Major Companies

3.3 Top 5 Financials Analysis

3.4 Patent Analysis - Major Companies

3.5 Pricing Analysis (ASPs will be provided)

4. Synthetic Resin Market - Startup companies Scenario Premium Premium Premium

4.1 Major startup company analysis:

4.1.1 Investment

4.1.2 Revenue

4.1.3 Product portfolio

4.1.4 Venture Capital and Funding Scenario

5. Synthetic Resin Market – Industry Market Entry Scenario Premium Premium Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Successful Venture Profiles

5.4 Customer Analysis – Major companies

6. Synthetic Resin Market - Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Porters Five Force Model

6.3.1 Bargaining Power of Suppliers

6.3.2 Bargaining Powers of Buyers

6.3.3 Threat of New Entrants

6.3.4 Competitive Rivalry

6.3.5 Threat of Substitutes

7. Synthetic Resin Market – Strategic Analysis

7.1 Value Chain Analysis

7.2 Opportunity Analysis

7.3 Product/Market Life Cycle

7.4 Distributor Analysis – Major Companies

8. Synthetic Resin Market - By Form (Market Size - US$ Million/Billion)

8.1 Solid

8.2 Liquid

8.3 Emulsion

8.4 Dispersion

9. Synthetic Resin Market - By Type (Market Size - US$ Million/Billion)

9.1 Thermosetting Resins

9.1.1 Polyester

9.1.1.1 Saturated Polyester Resins

9.1.1.2 Unsaturated Polyester Resins

9.1.2 Vinyl Ester

9.1.3 Epoxy

9.1.4 Phenolic

9.1.5 Urethane

9.1.6 Others

9.2 Thermoplastic Resins

9.2.1 Polycarbonate

9.2.2 Acrylic

9.2.3 Nylon

9.2.4 Polyethylene

9.2.4.1 High-Density Polyethylene (HDPE)

9.2.4.2 Low-Density Polyethylene (LDPE)

9.2.4. Others

9.2.5 Polyvinyl Chloride

9.2.6 Polyethylene Terephthalate

9.2.7 Polypropylene

9.2.7.1 Homopolymer Polypropylene

9.2.7.2 Copolymer Polypropylene

9.2.8 Polybutylene Terephthalate

9.2.9 Vinyl

9.2.10 Others

10. Synthetic Resin Market - By Application (Market Size - US$ Million/Billion)

10.1 Packaging

10.2 Printing Inks

10.3 Pipes & Hoses

10.4 Walls & Floors

10.5 Wood Finishes

10.6 Sheets & Films

10.7 Medical Devices

10.8 Paint & Coatings

10.9 Adhesives & Sealants

10.10 Electronic Fabrications

10.11 Transportation Components

10.12 Others

11. Synthetic Resin Market - By End-use Industry (Market Size - US$ Million/Billion)

11.1 Transportation

11.1.1 Automotive

11.1.1.1 Passenger Vehicles (PV)

11.1.1.2 Light Commercial Vehicles (LCV)

11.1.1.3 Heavy Commercial Vehicles (HCV)

11.1.2 Aerospace

11.1.2.1 Commercial

11.1.2.2 Military

11.1.2.3 Others

11.1.3 Locomotive

11.1.4 Marine

11.1.4.1 Passenger

11.1.4.2 Cargo

11.1.4.3 Others

11.2 Food & Beverage

11.2.1 Fruits & Vegetables

11.2.2 Dairy

11.2.3 Bakery

11.2.4 Confectionery

11.2.5 Poultry

11.2.6 Drinking Water

11.2.7 Soft Drinks

11.2.8 Others

11.3 Personal Care & Cosmetic

11.3.1 Body Care

11.3.2 Face Care

11.3.3 Eye Care

11.3.4 Nail Care

11.3.5 Fragrances

11.3.6 Others

11.4 Building & Construction

11.4.1 Residential

11.4.1.1 Private Dwellings

11.4.1.2 Row Houses

11.4.1.3 Apartments

11.4.2 Commercial

11.4.2.1 Hospital

11.4.2.2 Airports

11.4.2.3 Offices

11.4.2.4 Retail

11.4.2.5 Others

11.4.3 Industrial

11.4.3.1 Manufacturing Facilities

11.4.3.2 Warehouses

11.4.3.3 Others

11.4.4 Infrastructural

11.4.4.1 Roads

11.4.4.2 Bridges

11.4.4.3 Highways

11.4.4.4 Dams & Tunnels

11.4.4.5 Others

11.5 Oil & Gas

11.5.1 On-shore

11.5.2 Off-shore

11.6 Energy Generation

11.6.1 Wind Energy

11.6.2 Solar Energy

11.6.3 Others

11.7 Electrical & Electronics

11.7.1 Generators

11.7.2 Transformers

11.7.3 Circuit Breakers

11.7.4 Others

11.8 Military & Defense

11.8.1 Helmets

11.8.2 Bulletproof Jackets

11.8.3 Others

11.9 Medical & Healthcare

11.9.1 Connectors

11.9.2 Surgical Equipment

11.9.3 Blood Reservoirs

11.9.4 Others

11.10 Others

12. Synthetic Resin Market - By Geography (Market Size - US$ Million/Billion)

12.1 North America

12.1.1 USA

12.1.2 Canada

12.1.3 Mexico

12.2 Europe

12.2.1 UK

12.2.2 Germany

12.2.3 France

12.2.4 Italy

12.2.5 Netherlands

12.2.6 Spain

12.2.7 Russia

12.2.8 Belgium

12.2.9 Rest of Europe

12.3 Asia-Pacific

12.3.1 China

12.3.2 Japan

12.3.3 India

12.3.4 South Korea

12.3.5 Australia and New Zealand

12.3.6 Indonesia

12.3.7 Taiwan

12.3.8 Malaysia

12.3.9 Rest of APAC

12.4 South America

12.4.1 Brazil

12.4.2 Argentina

12.4.3 Colombia

12.4.4 Chile

12.4.5 Rest of South America

12.5 Rest of the World

12.5.1 Middle East

12.5.1.1 Saudi Arabia

12.5.1.2 UAE

12.5.1.3 Israel

12.5.1.4 Rest of the Middle East

12.5.2 Africa

12.5.2.1 South Africa

12.5.2.2 Nigeria

12.5.2.3 Rest of Africa

13. Synthetic Resin Market – Entropy

13.1 New Product Launches

13.2 M&As, Collaborations, JVs and Partnerships

14. Synthetic Resin Market – Industry/Segment Competition Landscape Premium

14.1 Company Benchmarking Matrix – Major Companies

14.2 Market Share at Global Level - Major companies

14.3 Market Share by Key Region - Major companies

14.4 Market Share by Key Country - Major companies

14.5 Market Share by Key Application - Major companies

14.6 Market Share by Key Product Type/Product category - Major companies

15. Synthetic Resin Market – Key Company List by Country Premium Premium Premium

16. Synthetic Resin Market Company Analysis - Business Overview, Product Portfolio, Financials and Developments

16.1. Sinopec Group (China Petrochemical Corporation)

16.2. Covestro AG

16.3. Jiangsu Sanmu Group

16.4. SABIC

16.5. The Dow Chemical Company

16.6. Nan Ya Plastics Corporation

16.7. Kukdo Chemical Co. Ltd.

16.8. Huntsman Corporation

16.9. Formosa Petrochemical Corporation

16.10. BASF SE and others

17. Synthetic Resin Market – Acquisitions/Technology Launches-

"Financials to the Private Companies would be provided on best-effort basis."

Connect with our experts to get customized reports that best suit your requirements. Our

reports include global-level data, niche markets and competitive landscape.

LIST OF TABLES

1.Global Synthetic Resin Market, by Type Market 2019-2024 ($M)2.Global Synthetic Resin Market Analysis and Forecast by Type and Application Market 2019-2024 ($M)

3.Global Synthetic Resin Market, by Type Market 2019-2024 (Volume/Units)

4.Global Synthetic Resin Market Analysis and Forecast by Type and Application Market 2019-2024 (Volume/Units)

5.North America Synthetic Resin Market, by Type Market 2019-2024 ($M)

6.North America Synthetic Resin Market Analysis and Forecast by Type and Application Market 2019-2024 ($M)

7.South America Synthetic Resin Market, by Type Market 2019-2024 ($M)

8.South America Synthetic Resin Market Analysis and Forecast by Type and Application Market 2019-2024 ($M)

9.Europe Synthetic Resin Market, by Type Market 2019-2024 ($M)

10.Europe Synthetic Resin Market Analysis and Forecast by Type and Application Market 2019-2024 ($M)

11.APAC Synthetic Resin Market, by Type Market 2019-2024 ($M)

12.APAC Synthetic Resin Market Analysis and Forecast by Type and Application Market 2019-2024 ($M)

13.MENA Synthetic Resin Market, by Type Market 2019-2024 ($M)

14.MENA Synthetic Resin Market Analysis and Forecast by Type and Application Market 2019-2024 ($M)

LIST OF FIGURES

1.US Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)2.Canada Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

3.Mexico Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

4.Brazil Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

5.Argentina Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

6.Peru Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

7.Colombia Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

8.Chile Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

9.Rest of South America Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

10.UK Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

11.Germany Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

12.France Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

13.Italy Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

14.Spain Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

15.Rest of Europe Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

16.China Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

17.India Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

18.Japan Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

19.South Korea Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

20.South Africa Global Synthetic Resin Industry Market Revenue, 2019-2024 ($M)

21.North America Global Synthetic Resin Industry By Application

22.South America Global Synthetic Resin Industry By Application

23.Europe Global Synthetic Resin Industry By Application

24.APAC Global Synthetic Resin Industry By Application

25.MENA Global Synthetic Resin Industry By Application