Email

Email Print

Print

Bisphenol A (Bpa) Market- By Application (Polycarbonate Resins, Epoxy Resins, Unsaturated Polyester Resins, Flame Retardants, Polyacrylate, Polysulfone resins, Polyetherimide, Others), By Geography - Global Opportunity Analysis & Industry Forecast, 2024-2030

Bisphenol A (Bpa) Market Overview

Bisphenol A (Bpa) Market size is forecast to reach $30.4 Billion by 2030, after growing at a CAGR of 5.3% during 2024-2030. Bisphenol A (BPA) is used primarily as an enhancer in polycarbonate plastic and epoxy resins, a colorless crystalline material that is found in the Organic compound class. BPA is used primarily for polycarbonate processing, and growing demand is anticipated to be a significant market factor for polycarbonates in food and medical goods. In addition, rising building industry and increasing demand for BPA are estimated to further increase market growth in the automotive industry.

Bisphenol A (BPA) experiences surging demand across pivotal sectors such as automotive, electronics, construction, and packaging due to its multifaceted utility in polycarbonate plastics and epoxy resins. Its versatile applications drive a steady need within these industries. BPA serves as a crucial component, enabling diverse functionalities in manufacturing processes, aligning with the stringent requisites of automotive, electronics, construction, and packaging sectors, fuelling its consistent market demand.

The increasing environmental consciousness drives a pivot toward sustainable solutions and eco-conscious replacements, prompting extensive exploration into BPA-free materials. Amid mounting environmental apprehensions, industries are actively pursuing environmentally friendly alternatives, fostering robust research endeavors to develop materials devoid of Bisphenol A (BPA). This heightened focus on sustainability underscores the pursuit of eco-friendly substitutes in response to the burgeoning environmental concerns.

Report Coverage

The report “Bisphenol A (Bpa) Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the Bisphenol (Bpa) Industry.

By End-Use Industry: Automotive Industry, Electronics Industry, Packaging Industry, Construction Industry, Others

By Application: Polycarbonate Resins, Epoxy Resins, Unsaturated Polyester Resins, Flame Retardants, Polyacrylate, Polysulfone resins, Polyetherimide, Others

By Geography: North America, South America, Europe, APAC, Middle East and Africa

Key Takeaways

- Epoxy resins and other plastics are made from BPA. Plastic from BPA is ideally adapted to the manufacture of a range of consumer goods such as sports gear, electrical devices, water bottles, DVDs, and CDs, including heat & solvent stability, resistance, and stability at low temperatures.

- Future demand for BPA is dependent on the global economic health, since the end-use segment includes the construction, automobile, and computer sectors. In various industrial applications, the demand driver for epoxy resins, vinyl ester resins, tetrabromobisphenol a, nitrate reductase, is its good quality efficiency in terms of thermal stability, corrosion resistance, moisture resistivity, mechanical strength, and adhesion.

- Increasing investments in research and development is supposed to have a massive business potential.

- The global COVID-19 pandemic resulted in a sudden halt to manufacturing operations worldwide which affected the demand for and development of plastics. Automotive & transport, household products, heavy machinery, manufacturing, and telecommunications are the most significantly impacted end usage categories of the plastics market. Covid19 will be the main contributor to this market

Application - Segment Analysis

Polycarbonate Resins segment holds the largest share in Bisphenol (Bpa) Market in 2023, is growing at a CAGR of 6.98% during forecast period 2024-2030. Polycarbonates are a high-performance thermoplastic commonly used to create and construct. Throughout a range of skylight and window uses, polycarbonate sheets may be used as a glass alternative. These are often known as opaque coverings, canopies, cross walls, façades, roofs for sporting facilities, roofs and roofing domes. These can also be used as opaque coverings. The usage of polycarbonate products in greenhouses in recent years has increased considerably. There are broad greenhouse growing areas throughout Europe, such as Germany, the Netherlands, Spain and France. Europe's urban industrial greenhouse sector accounts for nearly 25%.

The increasing popularity of polycarbonates is expected to drive the polycarbonate market during the forecast period due to their advantages over other standard materials (including glass and other plastics). In addition, polycarbonate is used in the automobile industry to retain strength, minimize weight, withstand shock for bumpers, restrict the explosion of danger through the usage of fuel tanks, seat belts, airbags, door and benches, subsystems, bumpers, components for under-bonnet, exterior trims etc. At present, 10 kg of polycarbonate is used in different ways to manufacture a standard four-wheel vehicle.

Geography - Segment Analysis

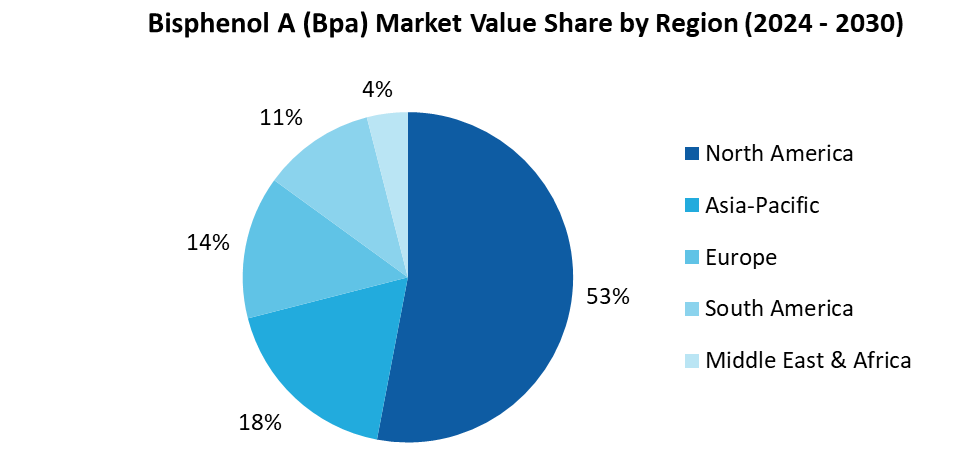

North America dominated the Bisphenol (Bpa) Market share with more than 52.6% in 2023, followed by APAC and Europe. According to the developments in glazing construction the steady growth of the trade industry, primarily in the construction of offices, is likely to have positive effects on the polycarbonate business. In the next few years, the country's office space demand is expected to rise almost by 10%, effectively growing the scale of the industry for bisphenol A (BPA). Throughout the past five years, demand has been rising consistently in the United States and automotive revenues have been steadily increasing.

This rapid development contributed to improved consumer demand for sunroofs, window frames, grips, inner lenses, handles of doors, headlight bezels, inner focus points and flammable radiator brows, which are being used in manufacture of polycarbonates. This emerging market for polycarbonates is expected to raise the bisphenol A (BPA) supply demand. The US Power Department plans to produce 404 GW of wind power by 2050. The rising market for composites fuels new developments including the production of low-cost carbon fibers and high-performance glass fibers.

For more details on this report - Request for Sample

Drivers – Bisphenol A (Bpa) Market

Increasing demand along with growing investment

In future years, the industry will be powered by rising demand for epoxy resins and polycarbonates with its numerous end-user applications. Among other places, low-cost synthetic fibers, robust glass fibers, and rotor blade composites provide other choices for utilizing BPA in the untapped market. These composites are used in windmills. Windmills need long-term productivity in the operation of sharp rotor blades coated with epoxy resin. The US Department of Energy the nation is estimated to have a potential of more than 400 GW of wind energy by 2050. There has been a major revolution inside the windmill sector owing to renewable power demands, which would have an impact on the businesses utilizing BPA.

The use to package food and drinks constitutes only around 4% of global polycarbonate use, and the market for BPA does not decline as there are already many applications. Asia Pacific is the industry leader in Bisphenol A and is projected to remain as wide end consumer industries in this field throughout its forecast period.

Challenges – Bisphenol A (Bpa) Market

Regulations

The limitation of the BPA industry is correlated with cancer-related health consequences. Increased public, environmental and media concern led to the gradual elimination of BPA as a result of food and beverage applications. The government has also regulated the use of BPA with these factors.

Market Landscape

Technology launches, acquisitions and R&D activities are key strategies adopted by players in the Bisphenol A (Bpa) Market. Major players in the Bisphenol A (Bpa) Market are Bayer Material Science, Chang Chun Plastics Co., Dow Chemicals, Kumho P&B Chemicals, LG Chemical Co., Mitsubishi Chemical Holding Corp., Nan Ya Plastics Corp., PTT Phenol Co., Sabic Innovative Plastics, Saudi Kayan Petrochemical Co, Samyang Innochem and Teijin Ltd., and among other.

For more Chemicals and Materials Market reports, please click here

1. Bisphenol A (Bpa) Market- Market Overview

1.1 Definitions and Scope

2. Bisphenol A (Bpa) Market- Executive Summary

2.1 Market Revenue, Market Size and Key Trends by Company

2.2 Key Trends by Application

2.3 Key Trends by Geography

3. Bisphenol A (Bpa) Market- Landscape

3.1 Comparative analysis

3.1.1 Market Share Analysis- Top Companies

3.1.2 Product Benchmarking- Top Companies

3.1.3 Top 5 Financials Analysis

3.1.4 Patent Analysis- Top Companies

3.1.5 Pricing Analysis

4. Bisphenol A (Bpa) Market- Startup companies Scenario Premium

4.1 Top startup company Analysis by

4.1.1Investment

4.1.2 Revenue

4.1.3 Market Shares

4.1.4 Market Size and Application Analysis

4.1.5 Venture Capital and Funding Scenario

5. Bisphenol A (Bpa) Market– Industry Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing business index

5.3 Case studies of successful ventures

5.4 Customer Analysis - Top companies

6. Bisphenol A (Bpa) Market- Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Market Opportunities

6.4 Porters five force model

6.4.1 Bargaining power of suppliers

6.4.2 Bargaining powers of customers

6.4.3 Threat of new entrants

6.4.4 Rivalry among existing players

6.4.5 Threat of substitutes

7. Bisphenol A (Bpa) Market-Strategic analysis

7.1 Value chain analysis

7.2 Opportunities analysis

7.3 Market life cycle

7.4 Suppliers and distributors Analysis

8. Bisphenol A (Bpa) Market– By Application (Market Size -$Million)

8.1 Polycarbonate Resins

8.2 Epoxy Resins

8.3 Unsaturated Polyester Resins

8.4 Flame Retardants

8.5 Polyacrylate

8.6 Polysulfone resins

8.7 Polyetherimide

8.8 Others

9. Bisphenol A (Bpa) Market- By Geography (Market Size -$Million)

9.1 North America

9.1.1 U.S.

9.1.2 Canada

9.1.3 Mexico

9.2 South America

9.2.1 Brazil

9.2.2 Argentina

9.2.3 Colombia

9.2.4 Chile

9.2.5 Rest OF South America

9.3 Europe

9.3.1 U.K

9.3.2 Germany

9.3.3 Italy

9.3.4 France

9.3.5 Spain

9.3.6 Netherlands

9.3.7 Russia

9.3.8 Belgium

9.3.9 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 India

9.4.3 Australia and New Zealand

9.4.4 Japan

9.4.5 South Korea

9.4.6 Rest of Asia Pacific

9.5 Middle East & Africa

9.5.1 Middle East

9.5.1.1 Saudi Arabia

9.5.1.2 UAE

9.5.1.3 Israel

9.5.1.4 Rest of Middle East

9.5.2 Africa

10.1.1.1 South Africa

10.1.1.2 Nigeria

10.1.1.3 Rest of South Africa

10. Bisphenol A (Bpa) Market- Entropy

10.1 New Product Launches

10.2 M&A’s, Collaborations, JVs and Partnerships

11. Market Share Analysis

11.1 Market Share by Country- Top companies

11.2 Market Share by Region- Top companies

11.3 Market Share by type of Product / Product category- Top companies

11.4 Market Share at global level- Top companies

11.5 Best Practices for companies

12. Bisphenol A (Bpa) Market- List of Key Companies by Country

13. Bisphenol A (Bpa) Market- Company Analysis

13.1 Market Share, Company Revenue, Products, M&A, Developments

13.2 Bayer Material Science

13.3 Chang Chun Plastics Co.

13.4 Dow Chemicals

13.5 Kumho P&B Chemicals

13.6 LG Chemical Co.

13.7 Mitsubishi Chemical Holding Corp.

13.8 Nan Ya Plastics Corp.

13.9 PTT Phenol Co.

13.10 Sabic Innovative Plastics

13.11 Saudi Kayan Petrochemical Co.

"*Financials would be provided on a best-efforts basis for private companies"