Email

Email Print

Print

Air Filtration Market Overview:

Air Filtration Market size is forecast to reach $25.69 billion by 2030, after growing at a CAGR of 7.3% during 2024-2030. This growth is driven by the rising demand for nanofiber filters is a notable trend in the air filtration market, fueled by the imperative for more effective filtration solutions amidst escalating levels of air pollution. Nanofiber filters are gaining traction due to their exceptional capability to capture ultrafine particles, including pollutants, allergens, and pathogens, with higher efficiency compared to conventional filters. As concerns over air quality intensify globally, industries such as automotive, healthcare, and manufacturing are increasingly adopting nanofiber filtration technology to improve indoor air quality, enhance worker safety, and comply with stringent regulatory standards, driving significant growth in the air filtration market.

Additionally, the adoption of smart air filters embedded with sensors and Internet of Things (IoT) technology represents a significant trend in the air filtration market. These advanced filters offer real-time monitoring of air quality, allowing users to track pollutant levels and ensure optimal indoor air quality. With the capability to automatically adjust filtration settings and provide alerts for timely filter replacements, smart air filters enhance convenience, efficiency, and effectiveness in air purification systems. As concerns over indoor air pollution and health continue to grow, the demand for smart air filtration solutions is expected to surge, driving innovation and growth in the air filtration market.

Air Filtration Market - Report Coverage:

The “Air Filtration Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Air Filtration Market.

By Filter Type: Cabin, Bag, Panel, Compact, Packed Bed, Combination, Pleated, Others

By Technology: Static, Dynamic, Electrostatic, Ionic, Others

By Filter Media: Activated Carbon, fiberglass, Metal, Filter Paper, Potassium Permanganate, Non-woven, Others

By System Type: HEPA Filtration, Dust Collectors, Mist Collectors, Bag House Filter, Others

By End Users: Food & Beverage, Industrial, Healthcare, Commercial, HVAC, Marine, Automotive, Aerospace and Defense, Residential, Chemical, Energy & Power Systems, Others

By Geography: North America, South America, Europe, APAC, and RoW.

COVID-19 / Ukraine Crisis - Impact Analysis:

• The COVID-19 pandemic has significantly impacted the Air Filtration Market. With a heightened focus on indoor air quality to curb virus transmission, demand for advanced filtration systems surged. Increased awareness of airborne contaminants and the importance of clean air in preventing respiratory illnesses drove market growth. The adoption of high-efficiency particulate air (HEPA) filters and advanced air purification technologies witnessed a substantial uptick. The pandemic accelerated innovation, pushing companies to develop cutting-edge solutions, making air filtration a crucial component in mitigating health risks in various sectors.

• The Russia-Ukraine crisis has disrupted the Air Filtration Market, primarily affecting the supply chain of essential raw materials. Sanctions, geopolitical tensions, and trade restrictions have led to increased costs and uncertainties for market players. Industries reliant on-air filtration systems, such as manufacturing and construction, face challenges in securing timely and cost-effective solutions. This geopolitical instability underscores the interconnectedness of global markets, urging businesses to diversify supply sources and adapt to dynamic geopolitical landscapes for a resilient Air Filtration Market.

Key Takeaways:

• The dominance of the Asia-Pacific (APAC) region in the Air Filtration Market significantly influences the industry's dynamics. With robust industrialization, urbanization, and increasing awareness of air quality, APAC leads in market demand. Rapid economic growth fuels sectors like manufacturing and automotive, driving the need for advanced air filtration solutions. As a result, key market players concentrate efforts on catering to APAC's expanding requirements, fostering innovation and strategic partnerships to address diverse air quality challenges and capitalize on the region's dominant position in the global Air Filtration Market.

• The Air Filtration Market witnesses a notable surge in the adoption of Baghouse Dust Collectors for large-scale industries. Driven by stringent environmental regulations and a focus on workplace safety, these collectors offer efficient particulate matter removal. Industries like cement, metal, and mining find these systems vital for maintaining air quality and complying with standards. The rise in industrial activities worldwide amplifies the demand, reflecting a growing awareness of the importance of effective air filtration systems in ensuring healthier work environments and sustainable industrial practices.

• The Air Filtration Market experiences a surge in demand due to the growing adoption of air filters in automotive applications. Stringent emissions regulations and heightened awareness of air quality drive the automotive industry to integrate advanced filtration systems. Cabin air filters, essential for maintaining indoor air quality within vehicles, witness increased deployment. This trend is not only enhancing passenger comfort but also addressing health concerns, positioning air filtration as a pivotal component in automotive design, signalling a promising growth trajectory in the market.

Air Filtration Market Segment Analysis – By Filter Type

The Air Filtration Market is witnessing a paradigm shift with 35% of market share in 2023, Dust Collectors are emerging as crucial components driving new market opportunities, particularly in industries like manufacturing, mining, and construction, where maintaining air quality is paramount for regulatory compliance and employee well-being. As businesses prioritize sustainability and compliance, the demand for efficient air filtration solutions is set to rise. Technological advancements, such as smart and connected Dust Collectors with sensor and monitoring capabilities, are gaining traction. These innovations enable real-time data analysis, predictive maintenance, and improved operational efficiency, appealing to industries seeking sustainable and cost-effective solutions. This presents a significant opportunity for businesses in the Air Filtration Market to diversify their product portfolios and tap into new revenue streams by addressing evolving industry needs and challenges proactively.

Air Filtration Market Segment Analysis – By Technology

Automotive has been the primary application for Air Filtration market and is expected to grow at a CAGR of 8.1% during forecast period 2024-2030. In the dynamic landscape of the Air Filtration Market, the automotive sector stands out as the primary application driver. The relentless pursuit of cleaner air, coupled with stringent emissions standards globally, has propelled the automotive industry to invest significantly in advanced air filtration technologies. Cabin air filters, in particular, have become integral components, ensuring the delivery of purified air to vehicle interiors. Automakers are increasingly prioritizing air quality within vehicles, not only for health and comfort but also as a competitive differentiator. The surge in electric vehicle adoption further accentuates the importance of efficient air filtration systems, as these vehicles often rely on advanced interior air quality solutions to compensate for the absence of traditional internal combustion engine emissions. Moreover, as consumers become more environmentally conscious, the demand for vehicles equipped with superior air filtration systems is on the rise. Original Equipment Manufacturers (OEMs) and aftermarket suppliers are responding by innovating and incorporating cutting-edge filtration technologies, such as high-efficiency particulate air (HEPA) filters, into their products. Beyond the automotive sector's direct impact on the Air Filtration Market, it also serves as a bellwether for other industries. The emphasis on clean air in automotive applications sets a precedent for heightened expectations in various sectors, driving innovation and growth in the broader air filtration industry. As regulatory standards evolve and consumers become increasingly discerning, the automotive industry's commitment to air quality is likely to sustain its role as a key influencer in the ongoing evolution of the Air Filtration Market.

Air Filtration Market Segment Analysis – By Filter Media

Nonwoven fabric has emerged as the fastest-growing filter media in the Air Filtration Market, owing to its numerous advantages and versatile applications. Nonwoven fabrics offer exceptional filtration efficiency, high dirt-holding capacity, and low airflow resistance, making them ideal for various air filtration applications. Their fibrous structure enables efficient particle capture, including fine particulate matter and allergens, contributing to improved indoor air quality. Additionally, nonwoven fabrics are lightweight, cost-effective, and easy to manufacture, providing a practical solution for air filtration needs across industries such as automotive, healthcare, and HVAC systems. As concerns over air pollution, allergens, and airborne contaminants escalate, the demand for nonwoven fabric filters continues to rise. Furthermore, advancements in nonwoven fabric technology, including the development of electrostatically charged and antimicrobial fabrics, further enhance their filtration performance and expand their market potential, positioning nonwoven fabric as a key growth driver in the air filtration market.

Air Filtration Market Segment Analysis – By System Type

HEPA (High Efficiency Particulate Air) filtration has emerged as the fastest-growing system type in the air filtration market, driven by increasing concerns over air quality and health impacts of airborne pollutants. HEPA filters are renowned for their exceptional ability to capture microscopic particles, including allergens, dust, bacteria, and viruses, with high efficiency. As industries and consumers alike prioritize cleaner indoor air environments, HEPA filtration systems have gained significant traction across various sectors, including healthcare, residential, commercial, and automotive. Moreover, stringent regulatory standards and guidelines mandating improved indoor air quality further fuel the demand for HEPA filtration solutions. The COVID-19 pandemic has also accelerated adoption, with a heightened focus on virus mitigation measures. Additionally, advancements in HEPA filter technology, such as compact designs, energy-efficient models, and smart features, contribute to their popularity. This trend underscores the growing importance of HEPA filtration in addressing air quality challenges and driving market growth.

Air Filtration Market Segment Analysis – By End Users

The industrial sector stands out as the fastest-growing end user in the air filtration market, driven by stringent regulatory standards, increasing awareness of environmental sustainability, and a growing emphasis on occupational health and safety. Industries such as manufacturing, mining, construction, and automotive production rely heavily on air filtration systems to maintain clean air environments, ensuring compliance with regulations and safeguarding worker well-being. With industrial processes generating various airborne contaminants, including dust, fumes, and volatile organic compounds (VOCs), the demand for efficient air filtration solutions is escalating rapidly. Furthermore, technological advancements such as smart and connected filtration systems equipped with sensors and real-time monitoring capabilities are gaining traction in the industrial sector, enabling predictive maintenance and improved operational efficiency. As industries prioritize sustainability and employee welfare, the industrial sector is expected to continue driving growth in the air filtration market, creating opportunities for innovation and expansion among industry players.

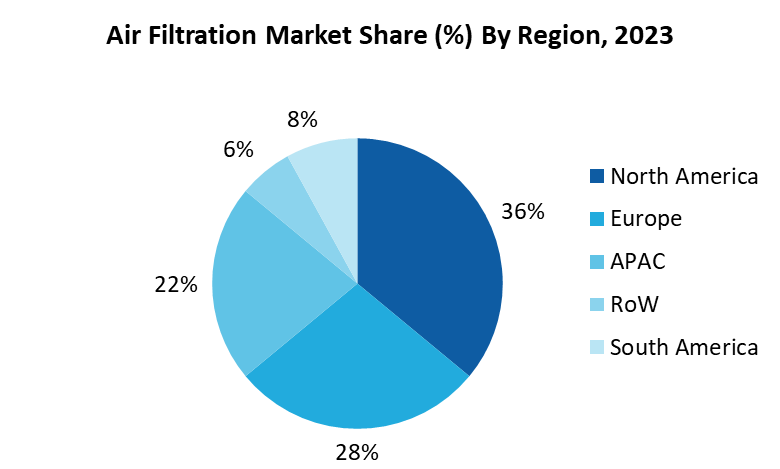

Air Filtration Market Segment Analysis – By Geography

APAC dominated the Air Filtration market with a share of 35.27%, followed by Europe and North America. This robust presence underscores the region's increasing industrialization, urbanization, and stringent air quality regulations. APAC's economic growth, particularly in manufacturing sectors, has fueled the demand for efficient air filtration solutions to address escalating pollution concerns. Following APAC, Europe and North America secure noteworthy positions in the market share hierarchy. Europe, renowned for its emphasis on environmental sustainability, exhibits a 29.84% share, reflecting a commitment to stringent regulatory frameworks and heightened awareness of the importance of air quality management. Meanwhile, North America closely trails with a 28.11% share, driven by a combination of industrial expansion and a growing focus on health and safety standards. These regional dynamics underscore the global nature of the Air Filtration Market, with each region grappling with unique challenges and opportunities. APAC's dominance is poised to persist as emerging economies in the region continue their industrial ascent, demanding cutting-edge air filtration technologies. Meanwhile, Europe and North America are likely to see sustained growth fueled by ongoing investments in environmental stewardship and advancements in filtration technologies. Navigating this diverse landscape requires industry stakeholders to adapt strategies tailored to regional nuances and capitalize on the evolving demands for cleaner air across the globe.

For more details on this report - Request for Sample

Drivers – Air Filtration Market

Increasingly stringent environmental regulations worldwide

The Air Filtration Market is significantly influenced by the ever-increasing stringency of environmental regulations globally. Governments and regulatory bodies worldwide are intensifying their focus on air quality standards to address the escalating concerns about pollution and its impact on public health. Stricter emissions limits and regulations compel industries to adopt advanced air filtration technologies to mitigate the release of particulate matter, pollutants, and harmful gases into the atmosphere. In response to the pressing need for environmental conservation, regulatory authorities are imposing stringent norms on various industries, including manufacturing, energy production, and transportation. These regulations are designed to curb emissions, reduce air pollution, and create healthier living conditions. Consequently, industries are compelled to invest in sophisticated air filtration systems that can efficiently capture and eliminate pollutants, ensuring compliance with these stringent standards. This regulatory-driven demand has spurred innovation in the Air Filtration Market, leading to the development of high-performance filtration technologies capable of meeting and exceeding the prescribed environmental standards. As a result, manufacturers and suppliers in the air filtration sector play a crucial role in assisting industries to adhere to these regulations, fostering the growth of a dynamic and responsive market that aligns with global environmental objectives. The trend towards increasingly stringent regulations positions the Air Filtration Market as a critical player in the broader movement towards sustainable and environmentally conscious industrial practices.

The growing awareness of health and safety, both in industrial settings and public spaces

The Air Filtration Market is witnessing a significant surge in demand, propelled by the escalating awareness of health and safety considerations in both industrial settings and public spaces. This heightened awareness stems from a growing understanding of the adverse effects of poor air quality on human health. Individuals, communities, and organizations are increasingly recognizing the importance of breathing clean air to prevent respiratory issues and safeguard overall well-being. In industrial settings, where workers are exposed to various pollutants and airborne particles, the emphasis on health and safety has led to a substantial uptake of advanced air filtration systems. Employers are investing in robust filtration technologies to create healthier work environments, reduce the risk of occupational illnesses, and comply with occupational health and safety standards. Similarly, in public spaces such as commercial buildings, educational institutions, healthcare facilities, and transportation hubs, there is a rising commitment to ensuring air quality. The ongoing global health challenges, including the COVID-19 pandemic, have further accentuated the need for effective air filtration to mitigate the spread of airborne contaminants. As a major market driver, this increased awareness underscores the pivotal role of air filtration in enhancing overall quality of life. The Air Filtration Market is poised to grow as businesses and communities prioritize clean air solutions, fostering a safer and healthier environment for occupants across diverse settings.

Challenges – Air Filtration Market

Supply Chain Disruptions a Major Threat to the Market Growth

Supply chain disruptions emerge as a major threat to the growth of the Air Filtration Market, posing challenges to the industry's stability and operational efficiency. The sector heavily relies on a complex network of suppliers and manufacturers for raw materials, components, and advanced filtration technologies. However, global events such as natural disasters, geopolitical tensions, and health crises like the COVID-19 pandemic have exposed the vulnerability of these supply chains. The unpredictability and suddenness of disruptions can lead to severe consequences, including delays in manufacturing processes, increased production costs, and a shortage of essential components. This, in turn, hampers the ability of companies within the Air Filtration Market to meet the escalating demand for air filtration solutions driven by environmental regulations and increasing awareness of health and safety. To navigate these challenges, companies must implement robust risk management strategies, including diversifying suppliers, adopting digital technologies for real-time visibility into the supply chain, and establishing contingency plans. Proactive measures are essential to ensure a resilient supply chain that can withstand unforeseen events, safeguarding the continuous availability of air filtration products and supporting the market's sustainable growth in the face of global uncertainties.

Market Landscape

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Air Filtration Market. The top 10 companies in this industry are: Camfil AB, Donaldson Company, Inc., 3M Company, Parker, Hannifin Corporation, Honeywell International Inc., Freudenberg Group, MANN+HUMMEL Group, AAF International, K&N Engineering, Inc., Daikin Industries Ltd.

Developments:

In April 2023, Camfil, a leading player in the Air Filtration Market, unveiled a groundbreaking sustainable air filtration solution. Leveraging cutting-edge materials and design innovations, the company introduced a series of eco-friendly filters that reduce environmental impact without compromising performance. This development aligns with the growing global emphasis on sustainable practices, reflecting Camfil's commitment to delivering effective air filtration solutions while prioritizing environmental responsibility.

In August 2023, 3M unveiled an advanced filtration media technology, enhancing particle-capturing capabilities for improved air filtration efficiency. The breakthrough caters to diverse industries like healthcare and manufacturing, meeting the escalating demand for superior filtration solutions. 3M's commitment to research and development reaffirms its leadership in air filtration innovation. This exemplifies key players' efforts in the Air Filtration Market to introduce sustainable and technologically advanced solutions, aligning with evolving industry needs.

For more Automation and Instrumentation Market reports, please click here

1. Air Filtration Market - Overview

1.1. Definitions and Scope

2. Air Filtration Market - Executive Summary

3. Air Filtration Market - Comparative Analysis

3.1. Company Benchmarking - Key Companies

3.2. Global Financial Analysis - Key Companies

3.3. Market Share Analysis - Key Companies

3.4. Patent Analysis

3.5. Pricing Analysis

4. Air Filtration Market - Start-up Companies Scenario (Premium)

4.1. Key Start-up Company Analysis by

4.1.1. Investment

4.1.2. Revenue

4.1.3. Venture Capital and Funding Scenario

5. Air Filtration Market – Market Entry Scenario Premium (Premium)

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Case Studies of Successful Ventures

6. Air Filtration Market - Forces

6.1. Market Drivers

6.2. Market Constraints

6.3. Market Challenges

6.4. Porter's Five Force Model

6.4.1. Bargaining Power of Suppliers

6.4.2. Bargaining Powers of Customers

6.4.3. Threat of New Entrants

6.4.4. Rivalry Among Existing Players

6.4.5. Threat of Substitutes

7. Air Filtration Market – Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Market Life Cycle

8. Air Filtration Market – By Filter Type (Market Size – $Million/$Billion)

8.1. Cabin

8.2. Bag

8.3. Panel

8.4. Compact

8.5. Packed Bed

8.6. Combination

8.7. Pleated

8.8. Others

9. Air Filtration Market – By Technology (Market Size – $Million/$Billion)

9.1. Static

9.2. Dynamic

9.3. Electrostatic

9.4. Ionic

9.5. Others

10. Air Filtration Market – By Filter Media (Market Size – $Million/$Billion)

10.1. Activated Carbon

10.2. Fiber Glass

10.3. Metal

10.4. Filter Paper

10.5. Potassium Permagnate

10.6. Non-woven

10.7. Others

11. Air Filtration Market – By System Type (Market Size – $Million/$Billion)

11.1. HEPA Filtration

11.2. Dust Collectors

11.3. Mist Collectors

11.4. Bag House Filter

11.5. Others

12. Air Filtration Market – By End Users (Market Size – $Million/$Billion)

12.1. Food & Beverage

12.2. Industrial

12.3. Healthcare

12.4. Commercial

12.5. HVAC

12.6. Marine

12.7. Automotive

12.8. Aerospace and Defense

12.9. Residential

12.10. Chemical

12.11. Energy & Power Systems

12.12. Others

13. Air Filtration Market – by Geography (Market Size – $Million/$Billion)

13.1. North America

13.1.1. The U.S.

13.1.2. Canada

13.1.3. Mexico

13.2. Europe

13.2.1. UK

13.2.2. Germany

13.2.3. France

13.2.4. Italy

13.2.5. Spain

13.2.6. Russia

13.2.7. Rest of Europe

13.3. Asia-Pacific

13.3.1. China

13.3.2. India

13.3.3. Japan

13.3.4. South Korea

13.3.5. Australia & New Zealand

13.3.6. Rest of Asia-Pacific

13.4. South America

13.4.1. Brazil

13.4.2. Argentina

13.4.3. Chile

13.4.4. Colombia

13.4.5. Rest of South America

13.5. Rest of the World

13.5.1. Middle East

13.5.2. Africa

14. Air Filtration Market – Entropy

15. Air Filtration Market – Industry/Segment Competition Landscape Premium

15.1. Market Share Analysis

15.1.1. Market Share by Filter Type – Key Companies

15.1.2. Market Share by Region – Key Companies

15.1.3. Market Share by Country – Key Companies

15.2. Competition Matrix

15.3. Best Practices for Companies

16. Air Filtration Market – Key Company List by Country Premium Premium

17. Air Filtration Market - Company Analysis

17.1. Camfil AB

17.2. Donaldson Company, Inc.

17.3. 3M Company

17.4. Parker Hannifin Corporation

17.5. Honeywell International Inc.

17.6. Freudenberg Group

17.7. MANN+HUMMEL Group

17.8. AAF International

17.9. K&N Engineering, Inc.

17.10. Daikin Industries Ltd.

"Financials to the Private Companies would be provided on best-effort basis."Connect with our experts to get customized reports that best suit your requirements. Our reports include global-level data, niche markets and competitive landscape.