Email

Email Print

Print

Polyethylene Wax Market Overview

The Polyethylene Wax market size is forecast to reach US$1.923 billion by 2030, after growing at a CAGR of 4.2% during the forecast period 2024-2030. Polyethylene can be divided into multiple categories such as high-density polyethylene, low-density polyethylene, oxidized polyethylene, and more. They are used for a wide range of applications which include plastic additives, hot melt adhesive, lubricants, digital printing inks, textile treatment, rubber, cosmetics, and other similar applications. The global industrial packaging industry is expected to grow by an annual rate of 5.1% within the forecast period of 2024-2030. An increase in demand for polyethylene wax from the packaging and textile industries acts as the major driver for the market. On the other hand, volatility in raw material prices and strict environmental regulations regarding the use of plastics may confine the growth of the market.

Polyethylene-based wax can be synthesized using various methods. One approach involves directly polymerizing ethylene under specific conditions to control molecular weight, resulting in polyethylene wax. Alternatively, high molecular weight polyethylene can be fractionated into lower molecular weight fractions to yield polyethylene wax.

Polyethylene wax boasts a high melting point, linear structure, low molecular weight, robust lubrication, chemical resistance, and anti-blocking properties. Consequently, it is highly sought after as an additive in applications requiring lubrication or physical modification in their formulations.

COVID-19 Impact

There is no doubt that the COVID-19 lockdown has significantly reduced manufacturing, and production activities as a result of the country-wise shutdown of manufacturing sites, shortage of labor, and the decline of supply and demand chain all over the world, thus, affecting the market. Studies show that the outbreak of COVID-19 sharply declined the production of raw materials in 2020 due to a lack of operations across multiple countries around the world. However, the COVID-19 pandemic has increased the demand for packaging all over the world. For instance, recent insights from Flexible Packaging states that the food packaging industry witnessed a sharp increase in demand during the pandemic due to a high number of consumers turning into online groceries shopping. By the end of 2023, U.S. online grocery sales accounted for 14.4% of the country’s overall e-commerce sales. It further states that the U.S. digital grocery buyers grew up to 145.7 million in 2023. Supermarkets witnessed a huge surge in demand for packaging materials for the wrapping of food and other grocery products. Hence, such an increase in demand for packaging is expected to increase the demand for polyethylene wax as it is primarily used as plastic additives in the production of plastics used for packaging. This is most likely to lead to market growth in the forecast period.

Report Coverage

The report: “Polyethylene Wax Market – Forecast (2024-2030)”, by IndustryARC covers an in-depth analysis of the following segments of the Polyethylene Wax Industry.

By Type: High Density Polyethylene, Low Density Polyethylene, Oxidized Polyethylene, Others.

By Manufacturing Process: High Pressure Polymerization, Low Pressure Polymerization, Others.

By Form: Flakes, Granules, Powder, Others.

By Application: Plastics, Hot Melt Adhesive, Lubricants, Rubber, Cosmetics, Paints & Coatings, Textile, Others.

By Geography: North America (USA, Canada, and Mexico), Europe (the UK, Germany, France, Italy, Netherlands, Spain, Russia, Belgium, and the Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, and New Zealand, Indonesia, Taiwan, Malaysia, and the Rest of Asia-Pacific), South America (Brazil, Argentina, Colombia, Chile and the Rest of South America), the Rest of the World (the Middle East, and Africa).

Key Takeaways

• Low Density Polyethylene segment in Polyethylene Wax Market is expected to see the fastest growth, especially during the forecast period. Its wide range of characteristics and advantages made it stand out in comparison to other types of polyethylene in the market.

• Polyethylene wax has a wide range of properties which include excellent thermal stability, high softening point, high melting point, high chemical resistance, perfect lubrication, which makes it ideal for use in the production of plastics, hot melt adhesive, lubricants, digital printing inks, and textile treatment.

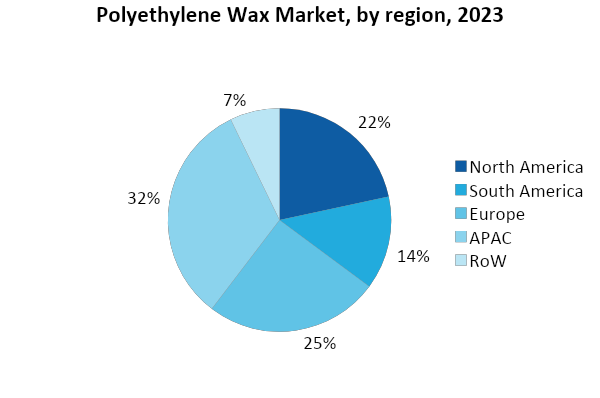

• Asia-Pacific dominated the Polyethylene Wax Market in 2023, owing to the increasing demand for polyethylene wax from the packaging sector of the region. According to a recent study published on Interpack, Asia accounted for the highest world share of packaging sales in 2023.

For more details on this report - Request for Sample

Polyethylene Wax Market Segment Analysis – By Type

Low Density Polyethylene type held the largest share in the Polyethylene Wax Market in 2023 and is expected to grow at a CAGR of 4.4% between 2024 and 2030, owing to its increasing demand due to the characteristics and benefits it offers over other types of polyethylene. Low Density Polyethylene provides better resistance to moisture, chemical resistance, impact resistance, and provide high resistance to temperature in comparison to high density polyethylene, and oxidized polyethylene. Moreover, low density polyethylene is more flexible with low tensile strength, is a poor conductor of electricity which makes them shock-proof in comparison to high density polyethylene, oxidized polyethylene, and other types of polyethylene. In addition to this, they are more economical, cost-effective, and recyclable. Hence, all of these properties are driving its demand over other types of polyethylene, which in turn, is expected to boost the market growth in the upcoming years.

Polyethylene Wax Market Segment Analysis – By Application

The Hot Melt Adhesive application held the largest share in the Polyethylene Wax Market in 2023 and is expected to grow at a CAGR of 4.6% between 2024 and 2030, owing to the increasing demand for adhesives from the construction and packaging sectors in multiple regions across the world. The adhesives sector saw an increase in the production of adhesives across multiple regions. Asia-Pacific saw an increase of 3.8%, Europe by 3.5%, North America by 3.1%, the Middle East by 3.3%, and Africa by 3.1% in 2023. This, in turn, increased the demand for polyethylene wax, since it is primarily used for the production of these adhesives.

Polyethylene Wax Market Segment Analysis – By Geography

The Asia Pacific held the largest share in the Polyethylene Wax Market in 2023 around 30%. The consumption of Polyethylene Wax is particularly high in this region due to its increasing demand from the packaging industry. For instance, China holds the largest market share around the world when it comes to food packaging. According to a recent study published on Interpack, the consumption of food packaging increased to around 447 billion in 2023. Likewise, it also states that the Chinese packaging companies such as 3D, SIP, and WLCSP alone achieved a revenue of around US$6.88 billion with end packaging.

According to the Packaging Industry Association of India, the Indian packaging industry was valued at around US$ 58.5 billion in 2023 and is expected to increase up to US$ 204.81 billion by the end of 2025. It further states that packaging is considered to be one of the industries with high growth in India and is rising at 22-25% per year. In this way, an increase in packaging activities will require the use of polyethylene wax as it is primarily used as plastic additives in the production of plastics used for packaging. This is most likely to lead to market growth in the forecast period.

Polyethylene Wax Market Drivers

An increase in demand from the packaging industry is most likely to increase demand for the product:

The North American beverage industry is expected to increase by 4.5% from 2024 to 2030, with the United States leading the beverage packaging sector. Likewise, recent insights from the Packaging Federation of the United Kingdom states that the UK packaging manufacturing industry reached an annual sale of US$ 17.2 billion in 2023, owing to the increasing demand for packaging from multiple sectors of the region. In this way, an increase in demand for packaging activities will require the use of polyethylene wax during the production of plastics required for packaging. This is most likely to lead to the growth of the market in the upcoming years.

An increase in demand from the textile industry is most likely to increase demand for the product:

Polyethylene wax emulsions are primarily used as softeners and sizing aids in the textile industry. The polyethylene wax emulsion generates bright color, high gloss, high tensile strength, and high elasticity in the fabric. For instance, as of June 13, 2023, Avgol India is expanding its non-woven fabric manufacturing in Himachal Pradesh with a total investment of INR 1690 million (US$ 20.35 million). A recent article published on fibre2fashion states that Vietnam’s garment manufacturing business accounts for around 70% of the majority of businesses. They also stated that the import of textiles and clothing by the United States increased by 16.03% up to US$132.201 billion during 2023. Likewise, the value of U.S. man-made fiber, textile, and clothing shipments reached about $74.4 billion in 2023. In this way, an increase in demand for various textile operations across the world would also increase the requirement of polyethylene wax for post-finishing of textiles in order to make the fabric have excellent smoothness, softness, and gloss. This is most likely to drive market growth in the upcoming years.

Polyethylene Wax Market Challenges

Volatility in raw material prices can cause an obstruction to the market growth:

When the availability of crude oil, additives, or other materials that are primarily used in the production of polyethylene resin fluctuates, the overall cost of producing the polyethylene resin increases. HDPE prices in North America initially surged in October 2023, but then depreciated by the end of the quarter. In December 2023, the European High-Density Polyethylene market saw a marginal decline of about 3%. In the first half of 2023, LDPE prices in the Asian market had been fluctuating and had mostly been on the lower side. In China, the spot prices of LDPE film grade fell from about $1317 USD/MT in January to about $1183 USD/MT in June 2023. Hence, such fluctuating prices of raw materials may confine the market growth.

Strict environmental regulations regarding the use of plastics can cause an obstruction to the market growth

According to the United States Environmental Protection Agency (EPA) Plastics Molding and Forming Effluent Guidelines and Standards (40 CFR Part 463), the guidelines are applicable to any plastics molding and forming process that releases or may release pollutants to waters or that releases pollutants into a publicly owned treatment works. Research and development laboratories that generate plastic products by making use of plastic molding processes are also subject to the discharge limitations guidelines and standards. None of the processes should release any discharge over the permissible limit or it will be charged with a penalty. Hence, strict regulations regarding the use of plastics may confine the market growth.

Polyethylene Wax Industry Outlook

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in this market. Polyethylene Wax top 10 companies include:

1. Mitsui Chemicals, Inc.

2. BASF SE

3. Arya Chem Inc.

4. Berkshire Hathaway (The Lubrizol Corporation)

5. Innospec Inc.

6. Huber Engineering Materials (Micro Powders Inc.)

7. Kerax Limited

8. Clariant

9. China Petrochemical Corporation (Sinopec)

10. WIWAX

Recent Developments

• In March 2022, Sasol, an energy and chemical company, sold its subsidiary Sasol Wax GmbH, to AWAX S.p.A, which specializes in development, production and distribution of wax products.

Relevant Reports

Report Code: CMR 0604

Report Code: CMR 64362

For more Chemicals and Materials related reports, please click here

1. Polyethylene Wax Market- Market Overview

1.1 Definitions and Scope

2. Polyethylene Wax Market - Executive Summary

2.1 Key Trends by Type

2.2 Key Trends by Manufacturing Process

2.3 Key Trends by Form

2.4 Key Trends by Application

2.5 Key Trends by Geography

3. Polyethylene Wax Market – Comparative analysis

3.1 Market Share Analysis- Major Companies

3.2 Product Benchmarking- Major Companies

3.3 Top 5 Financials Analysis

3.4 Patent Analysis- Major Companies

3.5 Pricing Analysis (ASPs will be provided)

4. Polyethylene Wax Market - Startup companies Scenario Premium Premium

4.1 Major startup company analysis:

4.1.1 Investment

4.1.2 Revenue

4.1.3 Product portfolio

4.1.4 Venture Capital and Funding Scenario

5. Polyethylene Wax Market – Industry Market Entry Scenario Premium Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Successful Venture Profiles

5.4 Customer Analysis – Major companies

6. Polyethylene Wax Market - Market Forces

6.1 Market Drivers

6.2 Market Constraints

6.3 Porters Five Force Model

6.3.1 Bargaining Power of Suppliers

6.3.2 Bargaining Powers of Buyers

6.3.3 Threat of New Entrants

6.3.4 Competitive Rivalry

6.3.5 Threat of Substitutes

7. Polyethylene Wax Market – Strategic Analysis

7.1 Value/Supply Chain Analysis

7.2 Opportunity Analysis

7.3 Product/Market Life Cycle

7.4 Distributor Analysis – Major Companies

8. Polyethylene Wax Market – By Type (Market Size - US$ Million/Billion)

8.1 High Density Polyethylene

8.2 Low Density Polyethylene

8.3 Oxidized Polyethylene

8.4 Others

9. Polyethylene Wax Market - By Manufacturing Process (Market Size - US$ Million/Billion)

9.1 High Pressure Polymerization

9.2 Low Pressure Polymerization

9.3 Others

10. Polyethylene Wax Market - By Form (Market Size - US$ Million/Billion)

10.1 Flakes

10.2 Granules

10.3 Powder

10.4 Others

11. Polyethylene Wax Market – By Application (Market Size - US$ Million/Billion)

11.1 Plastics

11.2 Hot Melt Adhesive

11.3 Lubricants

11.4 Rubber

11.5 Cosmetics

11.6 Paints & Coatings

11.7 Textile

11.8 Others

12. Polyethylene Wax Market - By Geography (Market Size - US$ Million/Billion)

12.1 North America

12.1.1 USA

12.1.2 Canada

12.1.3 Mexico

12.2 Europe

12.2.1 UK

12.2.2 Germany

12.2.3 France

12.2.4 Italy

12.2.5 Netherlands

12.2.6 Spain

12.2.7 Russia

12.2.8 Belgium

12.2.9 Rest of Europe

12.3 Asia-Pacific

12.3.1 China

12.3.2 Japan

12.3.3 India

12.3.4 South Korea

12.3.5 Australia and New Zealand

12.3.6 Indonesia

12.3.7 Taiwan

12.3.8 Malaysia

12.3.9 Rest of APAC

12.4 South America

12.4.1 Brazil

12.4.2 Argentina

12.4.3 Colombia

12.4.4 Chile

12.4.5 Rest of South America

12.5 Rest of the World

12.5.1 Middle East

12.5.2 Africa

13. Polyethylene Wax Market – Entropy

13.1 New Product Launches

13.2 M&As, Collaborations, JVs and Partnerships

14. Polyethylene Wax Market – Industry/Segment Competition Landscape Premium

14.1 Company Benchmarking Matrix – Major Companies

14.2 Market Share by Key Geography - Major companies

14.3 Market Share at Country Level - Major companies

14.4 Market Share by Key Product Type/Product category - Major companies

15. Polyethylene Wax Market – Key Company List by Country Premium Premium

16. Polyethylene Wax Market Company Analysis - Business Overview, Product Portfolio, Financials, and Developments

16.1 Mitsui Chemicals, Inc.

16.2 BASF SE

16.3 Arya Chem Inc.

16.4 Berkshire Hathaway (The Lubrizol Corporation)

16.5 Innospec Inc.

16.6 Huber Engineering Materials (Micro Powders Inc.)

16.7 Kerax Limited

16.8 Clariant

16.9 China Petrochemical Corporation (Sinopec)

16.10 WIWAX

"*Financials would be provided on a best-efforts basis for private companies"