Email

Email Print

Print

U.S Microgrid Market - Overview

The U.S Microgrid Market size is forecast to reach USD 10.6 billion by 2030, after growing at a CAGR of 13.1% during the forecast period 2023-2030. Microgrids are small scale localized power stations that have their own storage resource, generating plant and defined boundaries. The system can be powered by batteries, renewable sources and distributed generators based on the fuel requirement, application area and easy availability of generation source. The U.S. microgrid market is experiencing significant growth, driven by several key factors. Firstly, the increasing demand for reliable and resilient energy solutions has spurred the adoption of microgrids, which provide localized and decentralized power generation. This trend is particularly prominent in regions prone to extreme weather events, where microgrids offer a more robust and resilient energy infrastructure. Additionally, the integration of renewable energy sources, such as solar and wind, into microgrid systems aligns with the broader sustainability goals pursued by businesses and communities. According to the Center for Climate and Energy Solutions, the United States had 692 microgrids installed at the beginning of 2023, with a total capacity of nearly 4.4 gigawatts. This indicates a significant contribution to the U.S. energy landscape. It's worth noting that the microgrid capacity has seen substantial growth in recent years.

Report Coverage

The report “U.S Microgrid Market – Forecast (2023-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the U.S Microgrid Market.

By Components: Hardware, Software and Services.

By Grid Type: Grid-Connected, Off Grid, Hybrid

By Area: Urban/Metropolitan, Semi Urban, Rural

By Grid Power: AC Microgrid, DC Microgrid, Hybrid

By Business Model: Purchase Power Agreement (PPA), Utility Rate Base, Owner Financing, Others

By Power Rating: <1MW, 1MW to 5MW, 5MW to 10MW, Above 10MW

By Source: Non-Renewable, Renewable, Storage System, Others

By End User: Commercial/Industrial, Community, Utility Distribution, Institutional/Campus, Military, Remote

By Region: Northeast, Southwest, West, Midwest, Southeast, Alaska/Hawaii

Key Takeaways

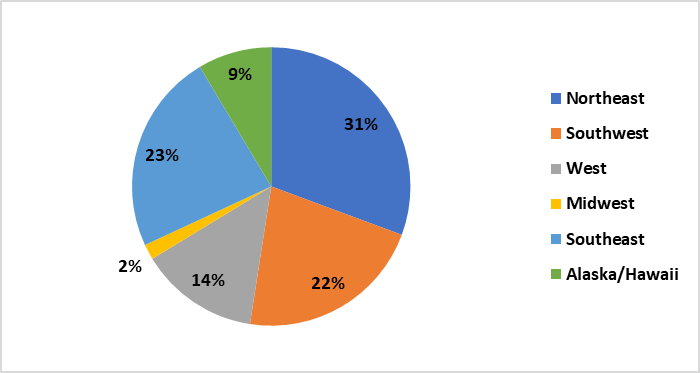

• Northeast held the largest market share with 31% in 2022. Microgrids are able to power individual buildings, or entire cities even if the surrounding power grid is facing outage. The U.S. Northeast is one major region that has been witnessing an increased number of power outages in recent years due to natural calamities and bad weather.

• The pandemic has made healthcare and senior facilities particularly attuned to the importance of reliable power. Hospitals have emergency backup generators, but a majority do not have enough to back up their entire facility. Therefore, microgrids are gaining popularity in US.

• In 2022, Citizens Medical Center, a hospital in Victoria, Texas, in partnership with Texas-based Enchanted Rock announced its plans to install 2.8 MW microgrid, to keep the hospital fully powered during a grid failure, however due to some issues the plan delayed. The project is expected to be commissioned shortly. As the COVID-19 pandemic has further highlighted the importance of microgrid in healthcare facilities.

By Components - Segment Analysis

Hardware segment dominated the U.S Microgrid Market in 2022. Functional elements, such as the CPU module, digital input module, digital output module, analogue input / output module, local controller, data logger, data recorder, relays, metres, and communication network are the hardware components of the microgrid control panel. The growing number of major power plant microgrid projects and high demand from process industries such as construction, oil & gas, refining, steel and chemical industries will push the hardware segment of the market for microgrid control systems. In December 2023, Cuyahoga County, Ohio, launched the first microgrid electrical utility in the United States. The initiative, approved by County Council, involves a 10-year contract with Compass Energy Platform of Los Angeles for design and financing. Construction on the initial three microgrids is projected to start in 2025, with completion and operation expected in 2026 and 2027. In a microgrid, one of the most critical aspects is the operation of power converters, with multiple distributed generators (DGs), energy storage systems and loads. These converters add interfaces between the microgrid bus and the DGs. In addition to improving control algorithms, inverters help to achieve greater functionality, performance and reliability.

By End User - Segment Analysis

Institutional/Campus dominated the U.S Microgrid Market in 2022. A wide range of institutions are using microgrids in order to boost electricity reliability, green energy supply, lower cost and to improve efficiency. In the U.S, the colleges and universities are regarded as the early adopters of microgrid technology, as they provide a campus with reliable and affordable power supply. Educational institutions often require microgrid, as it keeps their critical facilities running cost effectively especially university research labs which often requires temperature-sensitive specimens and power outages that may incur high cost. Additionally, colleges and universities are widely installing microgrids in order to achieve climate goals and to train students for energy related jobs. In the US, the healthcare institutions are also bringing intelligence and efficiency to hospital’s energy planning which is enhancing the demand for microgrid. This is also leading to the need for an advanced microgrid controller that can optimize and synchronize the various pieces of energy equipment. Moreover, the growing need for reliable power generation with low cost in institutions including healthcare and educational in the US will further boost the demand for the US Microgrid Market.

By Region - Segment Analysis

Northeast Microgrid Market generated a revenue of $1.2 billion in 2022 and is projected to reach a revenue of $3.1 billion by 2030 growing at a CAGR of 12.1% during 2023-2030. The Northeast Microgrid Market is projected to experience significant growth during the forecast period. The North East region of the United States has positioned itself as the fastest-growing hub in the U.S. microgrid market, exhibiting a remarkable surge in microgrid installations and developments. Several factors contribute to this notable growth trajectory. Firstly, the North East is home to a cluster of densely populated urban areas, where the demand for reliable and resilient energy solutions is particularly pronounced. The region's vulnerability to extreme weather events, such as hurricanes and nor'easters, has intensified the focus on robust energy infrastructure, making microgrids an increasingly attractive option. Additionally, state-level initiatives and supportive policies, driven by a commitment to clean energy and sustainability goals, have created a conducive environment for microgrid projects. States like New York, Massachusetts, and Connecticut have implemented forward-thinking policies, offering financial incentives and regulatory support for microgrid deployment.

U.S Microgrid Market Share (%) By Region, 2022

Drivers – U.S Microgrid Market

• Increasing Energy Resilience

The U.S. microgrid market is witnessing a surge driven by the growing emphasis on energy resilience. In an era marked by increasing climate uncertainties and the rising frequency of extreme weather events, businesses and communities are recognizing the paramount importance of resilient energy solutions. Microgrids, with their decentralized and localized power generation capabilities, offer a strategic response to this need. The ability of microgrids to operate autonomously or in conjunction with the main grid during disruptions enhances energy security and ensures uninterrupted power supply, making them a critical asset for various sectors. The Northeast region, with its vulnerability to severe weather, is particularly embracing microgrid solutions to fortify its energy infrastructure. State-level policies, such as those in New York and Massachusetts, supporting the development of microgrids further fuel this trend. Technological advancements, such as smart grid integration and energy storage systems, amplify the effectiveness of microgrids, making them an attractive investment for entities seeking energy resilience in an increasingly uncertain environment. According to U.S. Energy Information Administration, as of the end of 2022, the total nameplate power capacity of operational utility-scale battery energy storage systems (BESSs) in the United States was 8,842 MW and the total energy capacity was 11,105 MWh

• Electrification of Transportation

The growing popularity of electric vehicles is driving the need for an expanded charging infrastructure. Microgrids provide an efficient and localized solution for managing the increased electricity demand associated with widespread EV adoption, ensuring reliable and sustainable charging options. The mass deployment of EVs poses challenges to the centralized grid, such as increased peak demand and the need for additional grid infrastructure. Microgrids can support EV charging stations by managing the load and providing localized power generation, reducing strain on the grid and enhancing grid stability. According to The International Energy Agency (IEA), In the United States, the Inflation Reduction Act (IRA) has triggered a rush by global electromobility companies to expand US manufacturing operations. Between August 2022 and March 2023, major EV and battery makers announced cumulative post-IRA investments of USD 52 billion in North American EV supply chains, of which 50% is for battery manufacturing, and about 20% each for battery components and EV manufacturing.

Challenges – U.S Microgrid Market

High installation costs of microgrids

The initial costs involved in the installation and maintenance of microgrids are relatively higher than traditional grids. The installation costs of microgrids are 25–30% higher than that of the conventional electricity grids. They include costs for setting up a complete microgrid infrastructure, right from the deployment of communication systems to the installation of smart meters, as well as their regular maintenance. The costs of installing smart meters are 50% higher than the costs involved in installing electric meters. Distributed energy resources (DERs) used in microgrids are costlier than the ones used in traditional centralized power stations. This acts as a barrier to the growth of the microgrid market. As microgrids can store, convert, and recycle energy, as well as offer better reliability and power quality than traditional grids, their costs are higher than traditional grid. Additionally, the installation of renewable energy sources, such as solar panels and wind turbines, involves not only equipment expenses but also intricacies related to site-specific requirements. The permitting and regulatory processes, varying across states and municipalities, add complexity and can extend project timelines, amplifying costs.

Market Landscape

Product launches, acquisitions activities are key strategies adopted by players in the U.S Microgrid Market. in 2022, The major players in the U.S Microgrid Market are Hitachi Energy Ltd, General Electric Company, Siemens, Schneider Electric. IBM, and Others.

Developments:

In May 2023, Schneider Electric announced the EcoStruxure Microgrid Flex, an industry-first, innovative standardized microgrid solution designed to significantly reduce project timeline across the journey, delivering a greater return on investment for the system.

In December 2022, E Grid Solutions and LineVision, the global leader in Dynamic Line Ratings (DLR), have formed a partnership to deliver the world's first integrated suite of Grid Enhancing Technologies (GETs), providing utilities with an end-to-end Dynamic System Rating (DSR)..

For more Electonics Market reports, please click here

1. U.S Microgrid Market- Overview

1.1. Definitions and Scope

2. U.S Microgrid Market- Executive Summary

3. U.S Microgrid Market- Comparative Analysis

3.1. Market Share Analysis - Key Companies

3.2. Company Benchmarking - Key Companies

3.3. Global Financial Analysis - Key Companies

3.4. Patent Analysis

3.5. Pricing Analysis

4. U.S Microgrid Market- Start-up Companies Scenario Premium

4.1. Key Start-up Company Analysis by

4.1.1. Investment

4.1.2. Revenue

4.1.3. Venture Capital and Funding Scenario

5. U.S Microgrid Market– Market Entry Scenario Premium Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Case Studies of Successful Ventures

6. U.S Microgrid Market- Forces

6.1. Market Drivers

6.2. Market Challenges

6.3. Porter's Five Force Model

6.3.1. Bargaining Power of Suppliers

6.3.2. Bargaining Powers of Customers

6.3.3. Threat of New Entrants

6.3.4. Rivalry Among Existing Players

6.3.5. Threat of Substitutes

7. U.S Microgrid Market– Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Market Life Cycle

7.4. Regulatory Scenario

7.5. Tariff Dates

7.6. Microgrid Project Analysis

8. U.S Microgrid Market– by Grid Type (Market Size – $Million/$Billion)

8.1. Grid-Connected

8.2. Off Grid

8.3. Hybrid

9. U.S Microgrid Market– by Components (Market Size – $Million/$Billion)

9.1. Hardware

9.1.1. Inverter

9.1.2. Microgrid Controller

9.1.3. Battery

9.1.4. Others

9.2. Software

9.3. Services

10. U.S Microgrid Market– by Area (Market Size – $Million/$Billion)

10.1. Urban/Metropolitan

10.2. Semi Urban

10.3. Rural

11. U.S Microgrid Market– by Grid Power (Market Size – $Million/$Billion)

11.1. AC Microgrid

11.2. DC Microgrid

11.3. Hybrid

12. U.S Microgrid Market– by Business Model (Market Size – $Million/$Billion)

12.1. Purchase Power Agreement (PPA)

12.2. Utility Rate Base

12.3. Owner Financing

12.4. Others

13. U.S Microgrid Market– by Power Rating (Market Size – $Million/$Billion)

13.1. <1MW

13.2. 1MW to 5MW

13.3. 5MW to 10MW

13.4. Above 10MW

14. U.S Microgrid Market– by Source (Market Size – $Million/$Billion)

14.1. Non-Renewable

14.1.1. Fuel Cells

14.1.2. Natural Gas

14.1.3. Diesel

14.1.4. CHP and Micro CHP

14.2. Renewable

14.2.1. PV cells

14.2.2. Hydropower

14.2.3. Wind based

14.3. Storage System

14.3.1. Li-Ion Batteries

14.3.2. Lead Acid Batteries

14.3.3. Flow Batteries

14.3.4. Fly Wheels Energy Storage

14.4. Others

15. U.S Microgrid Market– by End User (Market Size – $Million/$Billion)

15.1. Commercial/Industrial

15.2. Community

15.3. Utility Distribution

15.4. Institutional/Campus

15.5. Military

15.6. Remote

16. U.S Microgrid Market – by Geography (Market Size – $Million/$Billion)

16.1. Northeast

16.2. Southwest

16.3. West

16.4. Midwest

16.5. Southeast

16.6. Alaska/Hawaii

17. U.S Microgrid Market– Entropy

18. U.S Microgrid Market– Industry/Segment Competition Landscape Premium

18.1. Market Share Analysis

18.1.1. Market Share by Product Type – Key Companies

18.1.2. Market Share by Region – Key Companies

18.1.3. Market Share by Country – Key Companies

18.2. Competition Matrix

18.3. Best Practices for Companies

19. U.S Microgrid Market– Key Company List by Country Premium Premium

20U.S Microgrid Market- Company Analysis

20.1. Hitachi Energy Ltd

20.2. General Electric Company

20.3. Siemens

20.4. Schneider Electric

20.5. Honeywell

20.6. Eaton Corporation plc

20.7. AWS TruePower

20.8. S&C Electric Company

20.9. Bloom Energy

20.10. BoxPower Inc.

"Financials to the Private Companies would be provided on best-effort basis."

Connect with our experts to get customized reports that best suit your requirements. Our

reports include global-level data, niche markets and competitive landscape.