Email

Email Print

Print

Aerospace Interior Adhesive Market - Forecast(2024 - 2030)

Aerospace Interior Adhesive Market Overview

The Aerospace Interior Adhesive Market size is projected to reach US$3.1 billion by 2027, after growing at a CAGR of 5.3% during the forecast period 2022-2027. The booming aircraft industry is the primary reason for the Aerospace Interior Adhesive Market growth. The interior adhesive for aerospace uses a variety of adhesive technologies, including film, liquid & web, resins (including epoxy, acrylic and polyurethane), mounting, attachment, laminating, skin-to-core adhesives and more. It provides minimal surface preparation and quick cure times to maintain continuous interior application lines in aerospace. Also, it improves overall interior durability and attractiveness through resistance to various pressures like impact, scratches and scuffs. However, in 2020, major aircraft manufacturing companies such as Boeing, Airbus and more halted the production of aircraft for a short period. This created ripples in the growth of the aerospace interior adhesive industry. In 2021, the aerospace manufacturers resumed their operations and surged aircraft production. As a result, accelerated the aerospace interior adhesive industry. Moreover, the surge in the production of rotorcraft is fueling the demand for aerospace interior adhesive. This factor is aiding the growth of the Aerospace Interior Adhesive Market size.

Report Coverage

The "Aerospace Interior Adhesive Market Report–Forecast (2022-2027)” by IndustryARC, covers an in-depth analysis of the following segments in the Aerospace Interior Adhesive Market.

Key Takeaways

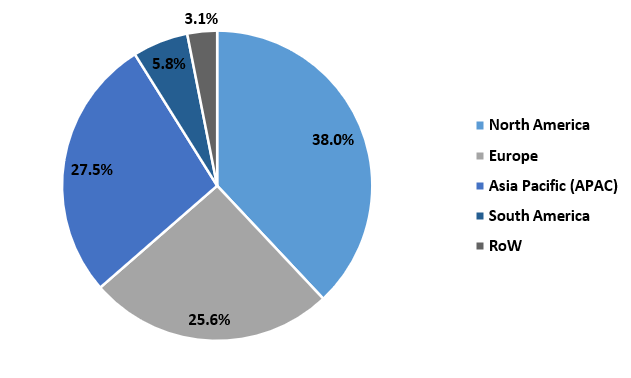

- North America dominated the Aerospace Interior Adhesive Market, owing to the growth of the aerospace industry in the region. For instance, according to the Aerospace Industries Association, in 2019, the sales related to aircraft in the US were US$387 billion, an increase of 6.7% over 2018.

- The surging new technological advancements related to Aerospace Interior Adhesives are driving the market growth.

- Moreover, the government initiatives for the Aerospace industry are fueling the production activities related to the aircraft. This, in turn, is accelerating market growth.

- However, the stringent government regulations related to Aerospace Interior Adhesives may restrict the market growth in the coming years.

Figure: Aerospace Interior Adhesive Market Revenue Share, By Geography, 2021 (%)

For More Details on This Report - Request for Sample

Aerospace Interior Adhesive Market Segment Analysis – by Resin

The epoxy segment held the largest Aerospace Interior Adhesive Market share in 2021 and is expected to grow at a CAGR of 5.1% during the forecast period 2022-2027. Epoxy resins have several exceptional qualities, including high wearability, scratch resistance, abrasion resistance and impact resistance. The primary benefit of epoxy adhesives is their high resistance to physical and chemical influences. They also have a high level of long-term stability due to their minimal tendency to creep. Epoxy resin can resist continuous temperatures ranging from 200°F (95°C) to 390°F (200°C), depending on the type. Thus, owing to these benefits, the adoption of epoxy resin-based aircraft adhesives for interior applications is rising. This factor is propelling the Aerospace Interior Adhesive Market growth.

Aerospace Interior Adhesive Market Segment Analysis – by Aircraft Type

The aircraft segment held the largest Aerospace Interior Adhesive Market share in 2021 and is projected to grow at a CAGR of 5.5% during the forecast period 2022-2027. The adhesives used in aircraft interiors provide the optimal stiffness-to-weight ratio, high impact resistance and superior structural performance. In addition to these, there are several advantages to employing adhesives for interior applications, including cost-effectiveness, bonding a wide variety of substrates, design freedom, reduced weight in structural assemblies, stress distribution in joints and more. Thus, owing to these properties and benefits of adhesives, it is frequently utilized in aircraft. The international partnerships between the countries are proliferating the aircraft industry growth. For instance, in September 2021, the production of 1st widebody aircraft started in China. The widebody aircraft, which COMAC and UAC jointly developed, is comparable in size to the Boeing 787 and was designed to lessen China's and Russia's reliance on long-range passenger aircraft. Commercial aircraft under the joint COMAC and UAC program should start flying in 2023. Hence, the growth of the aircraft industry is fueling the demand for Aerospace Interior Adhesive. As a result, spurring the market growth.

Aerospace Interior Adhesive Market Segment Analysis – by Geography

North America was the most dominating region in the Aerospace Interior Adhesive Market in 2021 with a market share of up to 38%. The factors such as increasing technological advancement, new aerospace manufacturing facilities, etc. are the key determinants driving the growth of the aircraft industry in the North American region. According to recent insights from the International Air Transport Association, Boeing, a leading aircraft manufacturer based in the U.S., has around 400 737 MAX aircraft in its inventory that has not yet been delivered. The company has even declared plans to boost the model's production to 31 per month by the end of 2022. Moreover, according to the Federal Aviation Administration (FAA), the U.S. would produce 8,270 commercial aircraft in total by the end of 2037. As a result of the country's expanding air freight industry. Therefore, the bolstering aircraft manufacturing industry in North America is expected to boost the demand for aerospace interior adhesive. This, in turn, would benefit the Aerospace Interior Adhesive Market size growth during the forecast period of 2022-2027.

Aerospace Interior Adhesive Market Drivers

Increasing Partnerships & Government Initiatives for Aerospace Industry

Governments at the global level are taking initiatives for the aerospace industry by increasing the manufacturing of aircraft in the country, increasing self-reliance and more. These governmental measures are benefiting the growth of the aerospace industry. For instance, in September 2021, Airbus and Tata Aircraft joined forces to produce airplanes in India. By the end of 2022, the new facility's construction would start and it would be finished by the end of 2023. Furthermore, the "Make in India" policy-supported aerospace industry encourages foreign businesses to invest in and improve the manufacturing process. Also, in July 2022, the Canadian government contributed US$7 million to Firan Technology Group Corporation (FTG) under the Aerospace Regional Recovery Initiative (ARRI) to boost productivity and diversify its product portfolio. Hence, such new partnerships and government initiatives related to the aerospace industry are boosting aircraft production. This, in turn, is fueling the demand for Aerospace Interior Adhesive, thereby, aiding the market growth.

New Technological Advancements related to Aerospace Interior Adhesive

The new adhesives are developed for use in Aerospace Interiors to comply with REACH and EH&S regulations as well as Boeing Process Specification BAC 5568. Moreover, the recent technological development related to aerospace interior adhesive also fulfills industry standards for fire retardancy, smoke density and toxicity (FST). In May 2019, new adhesives and composites technologies called EPOCAST 1648 and EPOCAST 1649 were introduced by Huntsman Corporation to be used in building aircraft interiors. The products are low in density, quick to cure and comply with flame, smoke and toxicity (FST) standards. The substance would be used for edge filling, ditch potting, insert potting and strengthening honeycomb constructions. Thus, such new technological advancements related to Aerospace Interior Adhesive are driving the market growth.

Aerospace Interior Adhesive Market Challenge:

Stringent Government Regulations related to the use of Aerospace Interior Adhesive

Regulations governing flame retardancy (FR) and fire, smoke and toxicity testing are overseen by the Federal Aviation Administration (FAA) and the European Aviation Safety Agency (EASA) (FST). The FAA regulation that applies to compartment interiors is 14CFR 25.853, which focuses on flame retardancy and is the main emphasis of the US regulations. These regulations comply with aerospace interior adhesives. Therefore, such stringent government regulations related to the use of adhesives for aerospace interior applications. This factor would restrict the growth of the Aerospace Interior Adhesive industry during the projected forecast period.

Aerospace Interior Adhesive Industry Outlook

Technology launches, acquisitions and increased R&D activities are key strategies adopted by players in the Aerospace Interior Adhesive Market. The top 10 companies in the Aerospace Interior Adhesive market are:

- 3M

- Akzo Nobel N.V.

- Solvay

- Arkema

- Henkel Adhesives Technologies India Private Limited

- Huntsman International LLC.

- AVERY DENNISON CORPORATION.

- Hexcel Corporation

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Master Bond Inc

Recent Developments

- In June 2021, Henkel in partnership with Aerospace giant Boeing launched a two-part epoxy adhesive, Loctite 9365FST. The adhesive complies with international EH7S and REACH regulations and meets industrial standards for fire retardancy, smoke density and toxicity (FST). This adhesive has application in Aerospace Interiors.

- In December 2020, Hexcel Corporation strengthened its strategic cooperation with Aerospace contractor Safran to cover a wider range of commercial aerospace applications. Hexcel has long been Safran's reliable source for high-tech, high-performance composites like carbon fiber, dry textiles and adhesives.

- In June 2019, the Adhesive Technologies business segment of Henkel opened a new production facility in Montornés, Spain, for aerospace applications. The new facility would boost Henkel's production capacity and enable the company to fulfill the growing demand for high-performance solutions from the Aerospace sector.

Relevant Reports

Report Code: CMR 0689

Report Code: CMR 0262

Report Code: CMR 75872

For more Chemicals and Materials Market reports, please click here

LIST OF TABLES

1.Global Aerospace Interior Adhesives Market By Resin Type Market 2019-2024 ($M)1.1 Epoxy Resin Market 2019-2024 ($M) - Global Industry Research

1.1.1 Cyanoacrylate Market 2019-2024 ($M)

1.1.2 Polyurethane Market 2019-2024 ($M)

1.1.3 Acrylic Market 2019-2024 ($M)

1.1.5 Single Aisle Market 2019-2024 ($M)

1.1.6 Small Wide Body Market 2019-2024 ($M)

1.1.7 Medium Wide Body Market 2019-2024 ($M)

1.1.8 Large Wide Body Market 2019-2024 ($M)

1.1.9 Regional Jets Market 2019-2024 ($M)

1.1.10 Seating Market 2019-2024 ($M)

1.1.11 Inflight Entertainment Market 2019-2024 ($M)

1.1.12 Galley Market 2019-2024 ($M)

1.1.13 Stowage Bins Market 2019-2024 ($M)

1.1.14 Lavatory Market 2019-2024 ($M)

1.1.15 Panels Market 2019-2024 ($M)

2.Global Aerospace Interior Adhesives Market By Aircraft Type Market 2019-2024 ($M)

3.Global Aerospace Interior Adhesives Market By Product Type Market 2019-2024 ($M)

4.Global Aerospace Interior Adhesives Market By Resin Type Market 2019-2024 (Volume/Units)

4.1 Epoxy Resin Market 2019-2024 (Volume/Units) - Global Industry Research

4.1.1 Cyanoacrylate Market 2019-2024 (Volume/Units)

4.1.2 Polyurethane Market 2019-2024 (Volume/Units)

4.1.3 Acrylic Market 2019-2024 (Volume/Units)

4.1.5 Single Aisle Market 2019-2024 (Volume/Units)

4.1.6 Small Wide Body Market 2019-2024 (Volume/Units)

4.1.7 Medium Wide Body Market 2019-2024 (Volume/Units)

4.1.8 Large Wide Body Market 2019-2024 (Volume/Units)

4.1.9 Regional Jets Market 2019-2024 (Volume/Units)

4.1.10 Seating Market 2019-2024 (Volume/Units)

4.1.11 Inflight Entertainment Market 2019-2024 (Volume/Units)

4.1.12 Galley Market 2019-2024 (Volume/Units)

4.1.13 Stowage Bins Market 2019-2024 (Volume/Units)

4.1.14 Lavatory Market 2019-2024 (Volume/Units)

4.1.15 Panels Market 2019-2024 (Volume/Units)

5.Global Aerospace Interior Adhesives Market By Aircraft Type Market 2019-2024 (Volume/Units)

6.Global Aerospace Interior Adhesives Market By Product Type Market 2019-2024 (Volume/Units)

7.North America Aerospace Interior Adhesives Market By Resin Type Market 2019-2024 ($M)

7.1 Epoxy Resin Market 2019-2024 ($M) - Regional Industry Research

7.1.1 Cyanoacrylate Market 2019-2024 ($M)

7.1.2 Polyurethane Market 2019-2024 ($M)

7.1.3 Acrylic Market 2019-2024 ($M)

7.1.5 Single Aisle Market 2019-2024 ($M)

7.1.6 Small Wide Body Market 2019-2024 ($M)

7.1.7 Medium Wide Body Market 2019-2024 ($M)

7.1.8 Large Wide Body Market 2019-2024 ($M)

7.1.9 Regional Jets Market 2019-2024 ($M)

7.1.10 Seating Market 2019-2024 ($M)

7.1.11 Inflight Entertainment Market 2019-2024 ($M)

7.1.12 Galley Market 2019-2024 ($M)

7.1.13 Stowage Bins Market 2019-2024 ($M)

7.1.14 Lavatory Market 2019-2024 ($M)

7.1.15 Panels Market 2019-2024 ($M)

8.North America Aerospace Interior Adhesives Market By Aircraft Type Market 2019-2024 ($M)

9.North America Aerospace Interior Adhesives Market By Product Type Market 2019-2024 ($M)

10.South America Aerospace Interior Adhesives Market By Resin Type Market 2019-2024 ($M)

10.1 Epoxy Resin Market 2019-2024 ($M) - Regional Industry Research

10.1.1 Cyanoacrylate Market 2019-2024 ($M)

10.1.2 Polyurethane Market 2019-2024 ($M)

10.1.3 Acrylic Market 2019-2024 ($M)

10.1.5 Single Aisle Market 2019-2024 ($M)

10.1.6 Small Wide Body Market 2019-2024 ($M)

10.1.7 Medium Wide Body Market 2019-2024 ($M)

10.1.8 Large Wide Body Market 2019-2024 ($M)

10.1.9 Regional Jets Market 2019-2024 ($M)

10.1.10 Seating Market 2019-2024 ($M)

10.1.11 Inflight Entertainment Market 2019-2024 ($M)

10.1.12 Galley Market 2019-2024 ($M)

10.1.13 Stowage Bins Market 2019-2024 ($M)

10.1.14 Lavatory Market 2019-2024 ($M)

10.1.15 Panels Market 2019-2024 ($M)

11.South America Aerospace Interior Adhesives Market By Aircraft Type Market 2019-2024 ($M)

12.South America Aerospace Interior Adhesives Market By Product Type Market 2019-2024 ($M)

13.Europe Aerospace Interior Adhesives Market By Resin Type Market 2019-2024 ($M)

13.1 Epoxy Resin Market 2019-2024 ($M) - Regional Industry Research

13.1.1 Cyanoacrylate Market 2019-2024 ($M)

13.1.2 Polyurethane Market 2019-2024 ($M)

13.1.3 Acrylic Market 2019-2024 ($M)

13.1.5 Single Aisle Market 2019-2024 ($M)

13.1.6 Small Wide Body Market 2019-2024 ($M)

13.1.7 Medium Wide Body Market 2019-2024 ($M)

13.1.8 Large Wide Body Market 2019-2024 ($M)

13.1.9 Regional Jets Market 2019-2024 ($M)

13.1.10 Seating Market 2019-2024 ($M)

13.1.11 Inflight Entertainment Market 2019-2024 ($M)

13.1.12 Galley Market 2019-2024 ($M)

13.1.13 Stowage Bins Market 2019-2024 ($M)

13.1.14 Lavatory Market 2019-2024 ($M)

13.1.15 Panels Market 2019-2024 ($M)

14.Europe Aerospace Interior Adhesives Market By Aircraft Type Market 2019-2024 ($M)

15.Europe Aerospace Interior Adhesives Market By Product Type Market 2019-2024 ($M)

16.APAC Aerospace Interior Adhesives Market By Resin Type Market 2019-2024 ($M)

16.1 Epoxy Resin Market 2019-2024 ($M) - Regional Industry Research

16.1.1 Cyanoacrylate Market 2019-2024 ($M)

16.1.2 Polyurethane Market 2019-2024 ($M)

16.1.3 Acrylic Market 2019-2024 ($M)

16.1.5 Single Aisle Market 2019-2024 ($M)

16.1.6 Small Wide Body Market 2019-2024 ($M)

16.1.7 Medium Wide Body Market 2019-2024 ($M)

16.1.8 Large Wide Body Market 2019-2024 ($M)

16.1.9 Regional Jets Market 2019-2024 ($M)

16.1.10 Seating Market 2019-2024 ($M)

16.1.11 Inflight Entertainment Market 2019-2024 ($M)

16.1.12 Galley Market 2019-2024 ($M)

16.1.13 Stowage Bins Market 2019-2024 ($M)

16.1.14 Lavatory Market 2019-2024 ($M)

16.1.15 Panels Market 2019-2024 ($M)

17.APAC Aerospace Interior Adhesives Market By Aircraft Type Market 2019-2024 ($M)

18.APAC Aerospace Interior Adhesives Market By Product Type Market 2019-2024 ($M)

19.MENA Aerospace Interior Adhesives Market By Resin Type Market 2019-2024 ($M)

19.1 Epoxy Resin Market 2019-2024 ($M) - Regional Industry Research

19.1.1 Cyanoacrylate Market 2019-2024 ($M)

19.1.2 Polyurethane Market 2019-2024 ($M)

19.1.3 Acrylic Market 2019-2024 ($M)

19.1.5 Single Aisle Market 2019-2024 ($M)

19.1.6 Small Wide Body Market 2019-2024 ($M)

19.1.7 Medium Wide Body Market 2019-2024 ($M)

19.1.8 Large Wide Body Market 2019-2024 ($M)

19.1.9 Regional Jets Market 2019-2024 ($M)

19.1.10 Seating Market 2019-2024 ($M)

19.1.11 Inflight Entertainment Market 2019-2024 ($M)

19.1.12 Galley Market 2019-2024 ($M)

19.1.13 Stowage Bins Market 2019-2024 ($M)

19.1.14 Lavatory Market 2019-2024 ($M)

19.1.15 Panels Market 2019-2024 ($M)

20.MENA Aerospace Interior Adhesives Market By Aircraft Type Market 2019-2024 ($M)

21.MENA Aerospace Interior Adhesives Market By Product Type Market 2019-2024 ($M)

LIST OF FIGURES

1.US Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)2.Canada Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

3.Mexico Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

4.Brazil Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

5.Argentina Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

6.Peru Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

7.Colombia Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

8.Chile Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

9.Rest of South America Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

10.UK Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

11.Germany Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

12.France Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

13.Italy Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

14.Spain Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

15.Rest of Europe Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

16.China Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

17.India Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

18.Japan Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

19.South Korea Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

20.South Africa Aerospace Interior Adhesive Market Revenue, 2019-2024 ($M)

21.North America Aerospace Interior Adhesive By Application

22.South America Aerospace Interior Adhesive By Application

23.Europe Aerospace Interior Adhesive By Application

24.APAC Aerospace Interior Adhesive By Application

25.MENA Aerospace Interior Adhesive By Application

26.Henkel AG & Co. KGaA, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.Arkema S.A., Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.3M Company, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.Huntsman Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Solvay S.A., Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Avery Dennison Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Hexcel Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Delo Industrie Klebstoffe GmbH & Co KGaA, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Master Bond Inc., Sales /Revenue, 2015-2018 ($Mn/$Bn)

35.Perma Bond LLC, Sales /Revenue, 2015-2018 ($Mn/$Bn)