Email

Email Print

Print

Cardiovascular Information System Market- Industry Analysis, Market Size, Share, Trends, Application Analysis, Growth And Forecast 2024-2030

Cardiovascular Information System Market Overview:

Cardiovascular Information System Market Size is estimated to reach $2.1 billion by 2030. Furthermore, it is poised to grow at a CAGR of 6.9% over the forecast period of 2024-2030. The Cardiovascular Information System (CVIS) market encompasses the industry focused on the development, distribution, and implementation of integrated software and hardware solutions designed to manage and streamline cardiovascular care. These systems facilitate the storage, retrieval, analysis, and sharing of cardiovascular patient data, including diagnostic images, reports, and treatment plans.

The key trend in the CVIS market is the increasing adoption of cloud-based solutions. Cloud-based CVIS platforms offer several advantages, including scalability, cost-effectiveness, and accessibility from any location with internet connectivity. These solutions allow healthcare providers to store and access large volumes of cardiovascular data securely, facilitating better collaboration and data sharing among medical professionals. Cloud-based CVIS also supports the integration of telemedicine, enabling remote monitoring and consultations, which have become especially important in the context of the COVID-19 pandemic. The trend towards cloud adoption is driven by the need for flexible, reliable, and efficient cardiovascular information management systems that can adapt to the evolving demands of modern healthcare environments.

Market Trends:

Adoption of Cloud-Based Solutions:

The adoption of cloud-based solutions is a major trend in the Cardiovascular Information System (CVIS) market. Cloud-based CVIS platforms offer significant benefits, including enhanced data storage capabilities, scalability, and cost-effectiveness. These systems enable healthcare providers to access cardiovascular data from any location with internet connectivity, facilitating better collaboration among medical professionals and improving patient care. The flexibility of cloud-based solutions supports the integration of telemedicine, which has become crucial in the wake of the COVID-19 pandemic. Cloud platforms also provide robust data security measures and compliance with healthcare regulations, ensuring patient information is protected. As healthcare organizations seek to reduce IT infrastructure costs and improve operational efficiency, the shift towards cloud-based CVIS is expected to continue growing. This trend is driven by the need for adaptable, reliable, and efficient systems that can keep pace with the evolving demands of modern healthcare.

Enhanced Interoperability and Integration:

Enhanced interoperability and integration are critical trends in the Cardiovascular Information System (CVIS) market. Interoperability refers to the ability of different healthcare systems and devices to communicate and share data seamlessly. In the context of CVIS, this means integrating cardiovascular data with other health information systems, such as Electronic Health Records (EHRs), Picture Archiving and Communication Systems (PACS), and laboratory information systems. Improved interoperability enables comprehensive patient data to be accessible in a unified platform, facilitating holistic patient care and better clinical decision-making. Regulatory initiatives and standards, such as the Health Level Seven International (HL7) and Fast Healthcare Interoperability Resources (FHIR), are driving the push towards greater interoperability. As healthcare providers seek to optimize patient outcomes and streamline workflows, the trend towards enhanced interoperability and integration in CVIS is set to grow, making cardiovascular data more accessible and actionable.

Market Snapshot:

Cardiovascular Information System Market - Report Coverage:

The “Cardiovascular Information System Market Report - Forecast (2024-2030)” by IndustryARC, covers an in-depth analysis of the following segments in the Cardiovascular Information System Market.

| Attribute | Segment |

|---|---|

|

By System Type |

|

|

By Component |

|

|

By Deployment Mode |

|

|

By Application |

|

|

By End-User |

|

|

By Geography |

|

COVID-19 / Ukraine Crisis - Impact Analysis:

- The COVID-19 pandemic significantly impacted the growth of the Cardiovascular Information System (CVIS) market, accelerating its adoption and expansion. As healthcare systems worldwide faced unprecedented challenges, there was a heightened need for efficient, digital solutions to manage cardiovascular care. Hospitals and clinics, overwhelmed by the surge in COVID-19 cases, sought to minimize in-person interactions, leading to an increased reliance on telemedicine and remote monitoring technologies. CVIS, with its ability to integrate and manage cardiology data electronically, became crucial in maintaining continuity of care for cardiovascular patients while reducing the risk of virus transmission. Additionally, the pandemic underscored the importance of having robust, interoperable systems to quickly access and share patient information, further driving investment in digital health infrastructure. Consequently, the CVIS market experienced accelerated growth as healthcare providers adapted to the new demands imposed by the pandemic, emphasizing the need for advanced, integrated cardiovascular information systems to enhance patient care and operational efficiency.

- The Russia-Ukraine war has had a complex impact on the growth of the Cardiovascular Information System (CVIS) market, primarily through its disruption of global supply chains and healthcare infrastructure. The conflict has caused significant instability in the region, leading to damaged healthcare facilities and strained medical resources in Ukraine, which in turn has impeded the adoption and implementation of advanced healthcare technologies like CVIS. Additionally, the war has exacerbated global supply chain challenges, resulting in delays and increased costs for the procurement of necessary hardware and software components. Economic sanctions on Russia and the diversion of funds towards military efforts have also redirected investment away from healthcare innovations. Moreover, the general climate of uncertainty and geopolitical tension has caused some hesitation among investors and companies in expanding their operations in the affected regions. Despite these challenges, the ongoing need for robust healthcare systems and the global emphasis on digital health solutions may still drive demand for CVIS in more stable markets, though growth in conflict-affected areas is likely to be significantly hindered.

Key Takeaways:

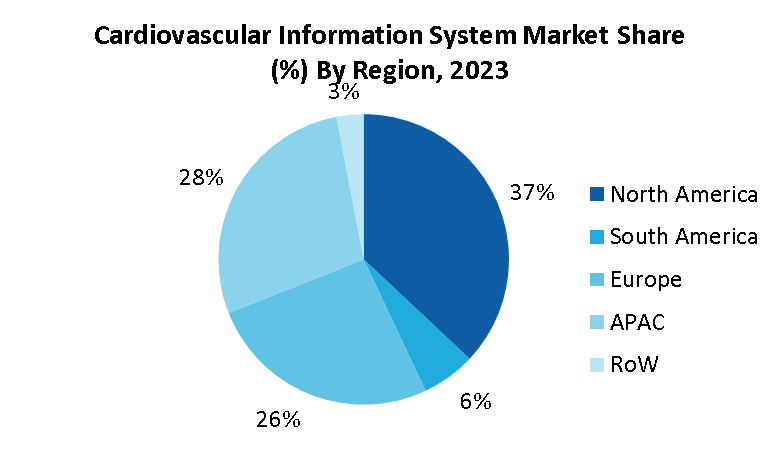

Dominance of North America

North America held a dominant market share of 37% in the year 2023 due to its advanced healthcare infrastructure, high prevalence of cardiovascular diseases, and strong focus on healthcare innovation. The region boasts a high adoption rate of cutting-edge medical technologies and robust investment in healthcare IT, driven by both private and public sectors. The presence of leading healthcare institutions and technology companies facilitates the rapid integration of CVIS solutions, enhancing clinical workflows and patient care. Furthermore, North America's regulatory environment, which emphasizes patient data security and interoperability, supports the deployment of comprehensive cardiovascular information systems. On February 2024, A new American Heart Association presidential advisory celebrates the scientific foundation of 100 years of lifesaving work while addressing challenges still ahead in the fight against heart disease and stroke. Dramatic advances in the understanding and treatment of cardiovascular diseases have saved millions of lives in the 100 years since the founding in 1924 of the American Heart Association, the world’s leading voluntary organization focused on heart and brain health for all. As heart disease and stroke remain the top causes of death worldwide, the solutions to challenges of the next century must combine lessons of the past with innovations of the future, according to The American Heart Association

The Cloud-Based segment to have Highest Growth Rate

The cloud-based segment has the highest growth rate during 2024-2030 period at 7.9% CAGR due to its numerous advantages over traditional on-premise systems. Cloud-based CVIS solutions offer unparalleled scalability, allowing healthcare providers to easily expand their data storage and processing capabilities as needed without significant upfront capital investment. They also provide greater accessibility, enabling medical professionals to access patient data from any location with internet connectivity, which is crucial for facilitating telemedicine and remote patient monitoring. This accessibility improves collaboration among healthcare teams and ensures continuity of care. Moreover, cloud-based systems typically include robust security measures and compliance with healthcare regulations, ensuring that patient data is protected and managed according to legal standards. The cost-effectiveness of cloud solutions, which reduce the need for extensive IT infrastructure and maintenance, further drives their adoption. As healthcare organizations continue to seek efficient, flexible, and secure data management solutions, the cloud-based segment remains the dominant force in the CVIS market, capturing the largest market share.

The Hospital segment to Hold Largest Market Share

The Hospital segment held a dominant market share of 49% in the year 2023 owing to the several factors that underscore its significance in cardiovascular care delivery. Hospitals serve as primary hubs for diagnosing and treating cardiovascular diseases, offering a wide range of cardiology services, including imaging, diagnostic tests, interventions, and long-term management. As a result, hospitals require comprehensive and integrated information systems to efficiently manage the vast amount of cardiovascular patient data generated across various departments and specialties. CVIS solutions provide hospitals with the tools needed to streamline workflows, improve clinical decision-making, and enhance patient care coordination. These systems enable seamless integration with electronic health records (EHRs), picture archiving and communication systems (PACS), and other hospital information systems, ensuring the seamless flow of patient data across different departments and care settings.

On July 2022, Apollo Hospitals collaborated with ConnectedLife, leaders in the application of motor state diagnostics, to integrate Apollo’s AICVD tool with ConnectedLife’s digital solutions for wellness, condition management and other health-focused applications. The AICVD tool can predict the risk of cardiovascular disease. This will empower healthcare providers with the tools to predict the risk of cardiac disease in their patients and initiate intervention early enough to make a real difference. Moreover, hospitals often have greater financial resources and infrastructure to invest in advanced healthcare technologies like CVIS, driving market growth in this segment. As cardiovascular diseases continue to pose significant healthcare challenges globally, hospitals remain at the forefront of cardiovascular care, fueling the demand for innovative CVIS solutions and solidifying their position as the leading segment in the market.

Rising Prevalence of Cardiovascular Diseases is boosting the market growth

The rising prevalence of cardiovascular diseases (CVDs) is a major driver of the Cardiovascular Information System (CVIS) market. Cardiovascular diseases, including heart attacks, strokes, and hypertension, remain the leading cause of mortality globally. With the aging population and lifestyle factors such as poor diet, lack of exercise, and smoking, the incidence of CVDs is on the rise. This surge in cardiovascular conditions necessitates advanced and efficient management systems to handle the growing patient load. CVIS enables healthcare providers to efficiently manage large volumes of cardiovascular data, streamline workflows, and improve diagnostic accuracy and treatment planning. The need for comprehensive cardiovascular care and efficient data management systems is pushing healthcare facilities to adopt CVIS, driving market growth. The ongoing burden of CVDs continues to underline the importance of robust cardiovascular information systems in enhancing patient outcomes and optimizing clinical operations.

Integration with Artificial Intelligence (AI) and Machine Learning (ML) is driving the market growth

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into Cardiovascular Information Systems (CVIS) is transforming the market. AI and ML algorithms can analyze vast amounts of cardiovascular data to identify patterns, predict outcomes, and assist in clinical decision-making. This integration enhances the accuracy of diagnoses, optimizes treatment plans, and improves patient outcomes. For example, AI-driven tools can help in the early detection of cardiovascular diseases by analyzing imaging data and identifying anomalies that may be missed by human eyes. Additionally, ML models can personalize patient care by predicting individual responses to treatments based on historical data. The incorporation of AI and ML into CVIS also streamlines administrative tasks, such as automating data entry and reporting, reducing the workload for healthcare providers. As the healthcare industry increasingly embraces digital transformation, the trend towards AI and ML integration in CVIS is expected to accelerate, driving innovation and improving cardiovascular care.

The American Heart Association encourages research and development of artificial intelligence (AI) and other related tools and services that may support and enable more precise approaches to cardiovascular and stroke research, prevention and care. On February 2024, Artificial intelligence (AI) may transform cardiovascular medicine. For now, though, many challenges remain, and few AI tools have been proven to improve care, according to a new American Heart Association scientific statement published in Circulation, the Association’s flagship, peer-reviewed journal. AI and machine learning digital tools currently exist that help to improve screening and help researchers to better understand optimal health and to develop precision treatments for complex health conditions. However, there is an urgent need to better understand how best to implement these tools into medical care in ways that are equitable, generalizable, ethical and cost-effective.

Data Security and Privacy Concerns challenges the growth of the Cardiovascular Information System market

One major challenge facing the Cardiovascular Information System (CVIS) market is the heightened focus on data security and privacy concerns. The sensitive nature of cardiovascular patient data, including medical records, imaging studies, and diagnostic reports, makes it a prime target for cyber threats and breaches. Healthcare organizations must navigate stringent regulations and compliance requirements, such as the Health Insurance Portability and Accountability Act (HIPAA) in the United States and the General Data Protection Regulation (GDPR) in Europe, to ensure the protection of patient information. Additionally, the increasing sophistication of cyberattacks poses a significant challenge, as hackers constantly evolve their tactics to exploit vulnerabilities in CVIS systems. Addressing data security and privacy concerns requires robust encryption measures, access controls, regular security audits, and employee training to mitigate risks and safeguard patient confidentiality. Failure to adequately address these challenges can result in significant financial and reputational damage to healthcare providers, hindering the adoption and growth of CVIS solutions.

For More Details on This Report - Request for Sample

Key Market Players:

Product/Service launches, approvals, patents and events, acquisitions, partnerships and collaborations are key strategies adopted by players in the Cardiovascular Information System Market. The top 10 companies in this industry are listed below:

- AGFA-Gevaert Group (Cardiology ecosystem)

- Philips Healthcare (Cardiovascular Workspace, Interventional Cardiovascular Workspace (Xper IM))

- GE HealthCare (MUSE Cardiology Information System)

- Siemens Healthineers AG (Cardiovascular Care)

- Merative ( CVIS for cardiology imaging)

- Fujifilm Medical Systems (Synapse® Select)

- Esaote SPA (Suitestensa Cardio Surgery)

- Central Data Networks PTY Ltd (Cardio Vascular Information System)

- Infinitt Healthcare Co Ltd (Infinitt Cardiology PACS)

- Lumedx (LUMEDX HealthView Cardiac Cath Workflow)

Scope of Report:

| Report Metric | Details |

|---|---|

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

CAGR |

6.9% |

|

Market Size in 2030 |

$2.1 billion |

|

Segments Covered |

Building Type, Component, Technology, Application and Region |

|

Geographies Covered |

North America (U.S., Canada and Mexico), Europe (Germany, France, UK, Italy, Spain, Netherlands and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia & New Zealand and Rest of Asia-Pacific), South America (Brazil, Argentina, Colombia and Rest of South America), Rest of the World (Middle East and Africa). |

|

Key Market Players |

|

For more Lifesciences and Healthcare related reports, please click here

1. Cardiovascular Information System Market- Overview

1.1. Definitions and Scope

2. Cardiovascular Information System Market- Executive Summary

3. Cardiovascular Information System Market–Comparative Analysis

3.1. Company Benchmarking – Key Companies

3.2. Financials Analysis–Key Companies

3.3. Market Share Analysis- Key Companies

3.4. Patent Analysis - Global

3.5. Pricing Analysis–Average Pricing

4. Cardiovascular Information System Market– Startup companies Scenario Premium

4.1. Investments

4.2. Revenue

4.3. Venture Capital and Funding Scenario

5. Cardiovascular Information System Market– Industry Market Entry Scenario Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Case studies of successful ventures

6. Cardiovascular Information System Market - Forces

6.1. Market Drivers

6.2. Market Constraints & Challenges

6.3. Porters Five Force Model

6.3.1. Bargaining power of suppliers

6.3.2. Bargaining powers of customers

6.3.3. Threat of new entrants

6.3.4. Rivalry among existing players

6.3.5. Threat of substitutes

7. Cardiovascular Information System Market- Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Market Life Cycle Analysis

8. Cardiovascular Information System Market- By System Type

8.1. Cardiovascular Information Systems (CVIS)

8.2. Cardiology Picture Archiving and Communication Systems (CPACS)

8.3. Vendor Neutral Archives (VNA)

8.4. Electronic Medical Records (EMR)

8.5. Others

9. Cardiovascular Information System Market- By Component

9.1. Hardware

9.2. Software

9.3. Services

10. Cardiovascular Information System Market- By Deployment Type

10.1. On-Premise

10.2. Cloud-Based

11. Cardiovascular Information System Market- By Application

11.1. Catheterization Lab

11.2. Electrocardiogram (ECG) Data Management

11.3. Echocardiography Lab

11.4. Nuclear Cardiology

11.5. Electrophysiology Lab

11.6. Cardiothoracic Center

11.7. ECG/Holter Monitoring

11.8. Pacemaker/ICD Lab

11.9. Heart Failure Center

11.10. Outpatient Clinic

11.11. Others

12. Cardiovascular Information System Market- By End-User

12.1. Hospitals

12.1.1. Small and Medium-sized Hospitals

12.1.2. Large Hospitals

12.2. Diagnostic Centers

12.3. Ambulatory Surgical Centers

12.4. Others

13. Cardiovascular Information System Market- By Geography

13.1. North America

13.1.1. U.S.

13.1.2. Canada

13.1.3. Mexico

13.2. Europe

13.2.1. U.K.

13.2.2. Germany

13.2.3. France

13.2.4. Italy

13.2.5. Spain

13.2.6. Rest of Europe

13.3. Asia-Pacific

13.3.1. China

13.3.2. Japan

13.3.3. South Korea

13.3.4. India

13.3.5. Australia & New Zealand

13.3.6. Rest of Asia-Pacific

13.4. South America

13.4.1. Brazil

13.4.2. Argentina

13.4.3. Rest of South America

13.5. Rest of the World

13.5.1. Middle East

13.5.2. Africa

14. Cardiovascular Information System Market – Entropy

15. Cardiovascular Information System Market – Industry/Segment Competition Landscape

15.1. Market Share Analysis

15.1.1. Market Share by Region – Key companies

15.1.2. Market Share by Countries – Key Companies

15.2. Competition Matrix

15.3. Best Practices for Companies

16. Cardiovascular Information System Market– Key Company List by Country Premium

17. Cardiovascular Information System Market Company Analysis (Overview, Financials, Developments, Product Portfolio)

17.1. AGFA-Gevaert Group

17.2. Philips Healthcare

17.3. GE HealthCare

17.4. Siemens Healthineers AG

17.5. Merative

17.6. Fujifilm Medical Systems

17.7. Esaote SPA

17.8. Central Data Networks PTY Ltd

17.9. Infinitt Healthcare Co Ltd

17.10. Lumedx

"*Financials would be provided on a best-efforts basis for private companies"

LIST OF TABLES

1.Global Cardiovascular Information System Market, By System Type Market 2023-2030 ($M)

1.1 Cvis Market 2023-2030 ($M) - Global Industry Research

1.2 Cpacs Market Market 2023-2030 ($M) - Global Industry Research

2.Global Cardiovascular Information System Market, By Component Market 2023-2030 ($M)

2.1 Software Market 2023-2030 ($M) - Global Industry Research

2.2 Service Market 2023-2030 ($M) - Global Industry Research

2.3 Hardware Market 2023-2030 ($M) - Global Industry Research

3.Global Cardiovascular Information System Market, By Mode Of Operation Market 2023-2030 ($M)

3.1 Web-Based Cvis Market 2023-2030 ($M) - Global Industry Research

3.2 Onsite Cvis Market 2023-2030 ($M) - Global Industry Research

3.3 Cloud-Based Market 2023-2030 ($M) - Global Industry Research

4.Global Cardiovascular Information System Market, By End User Market 2023-2030 ($M)

4.1 Hospital Market 2023-2030 ($M) - Global Industry Research

4.1.1 Small Hospital Market 2023-2030 ($M)

4.1.2 Medium-Sized Hospital Market 2023-2030 ($M)

4.1.3 Large Hospital Market 2023-2030 ($M)

4.2 Diagnostic Center Market 2023-2030 ($M) - Global Industry Research

5.Global Cardiovascular Information System Market, By System Type Market 2023-2030 (Volume/Units)

5.1 Cvis Market 2023-2030 (Volume/Units) - Global Industry Research

5.2 Cpacs Market Market 2023-2030 (Volume/Units) - Global Industry Research

6.Global Cardiovascular Information System Market, By Component Market 2023-2030 (Volume/Units)

6.1 Software Market 2023-2030 (Volume/Units) - Global Industry Research

6.2 Service Market 2023-2030 (Volume/Units) - Global Industry Research

6.3 Hardware Market 2023-2030 (Volume/Units) - Global Industry Research

7.Global Cardiovascular Information System Market, By Mode Of Operation Market 2023-2030 (Volume/Units)

7.1 Web-Based Cvis Market 2023-2030 (Volume/Units) - Global Industry Research

7.2 Onsite Cvis Market 2023-2030 (Volume/Units) - Global Industry Research

7.3 Cloud-Based Market 2023-2030 (Volume/Units) - Global Industry Research

8.Global Cardiovascular Information System Market, By End User Market 2023-2030 (Volume/Units)

8.1 Hospital Market 2023-2030 (Volume/Units) - Global Industry Research

8.1.1 Small Hospital Market 2023-2030 (Volume/Units)

8.1.2 Medium-Sized Hospital Market 2023-2030 (Volume/Units)

8.1.3 Large Hospital Market 2023-2030 (Volume/Units)

8.2 Diagnostic Center Market 2023-2030 (Volume/Units) - Global Industry Research

9.North America Cardiovascular Information System Market, By System Type Market 2023-2030 ($M)

9.1 Cvis Market 2023-2030 ($M) - Regional Industry Research

9.2 Cpacs Market Market 2023-2030 ($M) - Regional Industry Research

10.North America Cardiovascular Information System Market, By Component Market 2023-2030 ($M)

10.1 Software Market 2023-2030 ($M) - Regional Industry Research

10.2 Service Market 2023-2030 ($M) - Regional Industry Research

10.3 Hardware Market 2023-2030 ($M) - Regional Industry Research

11.North America Cardiovascular Information System Market, By Mode Of Operation Market 2023-2030 ($M)

11.1 Web-Based Cvis Market 2023-2030 ($M) - Regional Industry Research

11.2 Onsite Cvis Market 2023-2030 ($M) - Regional Industry Research

11.3 Cloud-Based Market 2023-2030 ($M) - Regional Industry Research

12.North America Cardiovascular Information System Market, By End User Market 2023-2030 ($M)

12.1 Hospital Market 2023-2030 ($M) - Regional Industry Research

12.1.1 Small Hospital Market 2023-2030 ($M)

12.1.2 Medium-Sized Hospital Market 2023-2030 ($M)

12.1.3 Large Hospital Market 2023-2030 ($M)

12.2 Diagnostic Center Market 2023-2030 ($M) - Regional Industry Research

13.South America Cardiovascular Information System Market, By System Type Market 2023-2030 ($M)

13.1 Cvis Market 2023-2030 ($M) - Regional Industry Research

13.2 Cpacs Market Market 2023-2030 ($M) - Regional Industry Research

14.South America Cardiovascular Information System Market, By Component Market 2023-2030 ($M)

14.1 Software Market 2023-2030 ($M) - Regional Industry Research

14.2 Service Market 2023-2030 ($M) - Regional Industry Research

14.3 Hardware Market 2023-2030 ($M) - Regional Industry Research

15.South America Cardiovascular Information System Market, By Mode Of Operation Market 2023-2030 ($M)

15.1 Web-Based Cvis Market 2023-2030 ($M) - Regional Industry Research

15.2 Onsite Cvis Market 2023-2030 ($M) - Regional Industry Research

15.3 Cloud-Based Market 2023-2030 ($M) - Regional Industry Research

16.South America Cardiovascular Information System Market, By End User Market 2023-2030 ($M)

16.1 Hospital Market 2023-2030 ($M) - Regional Industry Research

16.1.1 Small Hospital Market 2023-2030 ($M)

16.1.2 Medium-Sized Hospital Market 2023-2030 ($M)

16.1.3 Large Hospital Market 2023-2030 ($M)

16.2 Diagnostic Center Market 2023-2030 ($M) - Regional Industry Research

17.Europe Cardiovascular Information System Market, By System Type Market 2023-2030 ($M)

17.1 Cvis Market 2023-2030 ($M) - Regional Industry Research

17.2 Cpacs Market Market 2023-2030 ($M) - Regional Industry Research

18.Europe Cardiovascular Information System Market, By Component Market 2023-2030 ($M)

18.1 Software Market 2023-2030 ($M) - Regional Industry Research

18.2 Service Market 2023-2030 ($M) - Regional Industry Research

18.3 Hardware Market 2023-2030 ($M) - Regional Industry Research

19.Europe Cardiovascular Information System Market, By Mode Of Operation Market 2023-2030 ($M)

19.1 Web-Based Cvis Market 2023-2030 ($M) - Regional Industry Research

19.2 Onsite Cvis Market 2023-2030 ($M) - Regional Industry Research

19.3 Cloud-Based Market 2023-2030 ($M) - Regional Industry Research

20.Europe Cardiovascular Information System Market, By End User Market 2023-2030 ($M)

20.1 Hospital Market 2023-2030 ($M) - Regional Industry Research

20.1.1 Small Hospital Market 2023-2030 ($M)

20.1.2 Medium-Sized Hospital Market 2023-2030 ($M)

20.1.3 Large Hospital Market 2023-2030 ($M)

20.2 Diagnostic Center Market 2023-2030 ($M) - Regional Industry Research

21.APAC Cardiovascular Information System Market, By System Type Market 2023-2030 ($M)

21.1 Cvis Market 2023-2030 ($M) - Regional Industry Research

21.2 Cpacs Market Market 2023-2030 ($M) - Regional Industry Research

22.APAC Cardiovascular Information System Market, By Component Market 2023-2030 ($M)

22.1 Software Market 2023-2030 ($M) - Regional Industry Research

22.2 Service Market 2023-2030 ($M) - Regional Industry Research

22.3 Hardware Market 2023-2030 ($M) - Regional Industry Research

23.APAC Cardiovascular Information System Market, By Mode Of Operation Market 2023-2030 ($M)

23.1 Web-Based Cvis Market 2023-2030 ($M) - Regional Industry Research

23.2 Onsite Cvis Market 2023-2030 ($M) - Regional Industry Research

23.3 Cloud-Based Market 2023-2030 ($M) - Regional Industry Research

24.APAC Cardiovascular Information System Market, By End User Market 2023-2030 ($M)

24.1 Hospital Market 2023-2030 ($M) - Regional Industry Research

24.1.1 Small Hospital Market 2023-2030 ($M)

24.1.2 Medium-Sized Hospital Market 2023-2030 ($M)

24.1.3 Large Hospital Market 2023-2030 ($M)

24.2 Diagnostic Center Market 2023-2030 ($M) - Regional Industry Research

25.MENA Cardiovascular Information System Market, By System Type Market 2023-2030 ($M)

25.1 Cvis Market 2023-2030 ($M) - Regional Industry Research

25.2 Cpacs Market Market 2023-2030 ($M) - Regional Industry Research

26.MENA Cardiovascular Information System Market, By Component Market 2023-2030 ($M)

26.1 Software Market 2023-2030 ($M) - Regional Industry Research

26.2 Service Market 2023-2030 ($M) - Regional Industry Research

26.3 Hardware Market 2023-2030 ($M) - Regional Industry Research

27.MENA Cardiovascular Information System Market, By Mode Of Operation Market 2023-2030 ($M)

27.1 Web-Based Cvis Market 2023-2030 ($M) - Regional Industry Research

27.2 Onsite Cvis Market 2023-2030 ($M) - Regional Industry Research

27.3 Cloud-Based Market 2023-2030 ($M) - Regional Industry Research

28.MENA Cardiovascular Information System Market, By End User Market 2023-2030 ($M)

28.1 Hospital Market 2023-2030 ($M) - Regional Industry Research

28.1.1 Small Hospital Market 2023-2030 ($M)

28.1.2 Medium-Sized Hospital Market 2023-2030 ($M)

28.1.3 Large Hospital Market 2023-2030 ($M)

28.2 Diagnostic Center Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Cardiovascular Information System Market Revenue, 2023-2030 ($M)

2.Canada Cardiovascular Information System Market Revenue, 2023-2030 ($M)

3.Mexico Cardiovascular Information System Market Revenue, 2023-2030 ($M)

4.Brazil Cardiovascular Information System Market Revenue, 2023-2030 ($M)

5.Argentina Cardiovascular Information System Market Revenue, 2023-2030 ($M)

6.Peru Cardiovascular Information System Market Revenue, 2023-2030 ($M)

7.Colombia Cardiovascular Information System Market Revenue, 2023-2030 ($M)

8.Chile Cardiovascular Information System Market Revenue, 2023-2030 ($M)

9.Rest of South America Cardiovascular Information System Market Revenue, 2023-2030 ($M)

10.UK Cardiovascular Information System Market Revenue, 2023-2030 ($M)

11.Germany Cardiovascular Information System Market Revenue, 2023-2030 ($M)

12.France Cardiovascular Information System Market Revenue, 2023-2030 ($M)

13.Italy Cardiovascular Information System Market Revenue, 2023-2030 ($M)

14.Spain Cardiovascular Information System Market Revenue, 2023-2030 ($M)

15.Rest of Europe Cardiovascular Information System Market Revenue, 2023-2030 ($M)

16.China Cardiovascular Information System Market Revenue, 2023-2030 ($M)

17.India Cardiovascular Information System Market Revenue, 2023-2030 ($M)

18.Japan Cardiovascular Information System Market Revenue, 2023-2030 ($M)

19.South Korea Cardiovascular Information System Market Revenue, 2023-2030 ($M)

20.South Africa Cardiovascular Information System Market Revenue, 2023-2030 ($M)

21.North America Cardiovascular Information System By Application

22.South America Cardiovascular Information System By Application

23.Europe Cardiovascular Information System By Application

24.APAC Cardiovascular Information System By Application

25.MENA Cardiovascular Information System By Application

26.Mckesson Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)

27.Ge Healthcare, Sales /Revenue, 2015-2018 ($Mn/$Bn)

28.Siemens Healthcare, Sales /Revenue, 2015-2018 ($Mn/$Bn)

29.Merge Healthcare, Sales /Revenue, 2015-2018 ($Mn/$Bn)

30.Agfa Healthcare, Sales /Revenue, 2015-2018 ($Mn/$Bn)

31.Lumedx, Sales /Revenue, 2015-2018 ($Mn/$Bn)

32.Digisonics, Sales /Revenue, 2015-2018 ($Mn/$Bn)

33.Fujifilm Medical System, Sales /Revenue, 2015-2018 ($Mn/$Bn)

34.Cerner Corporation, Sales /Revenue, 2015-2018 ($Mn/$Bn)