Email

Email Print

Print

Overview

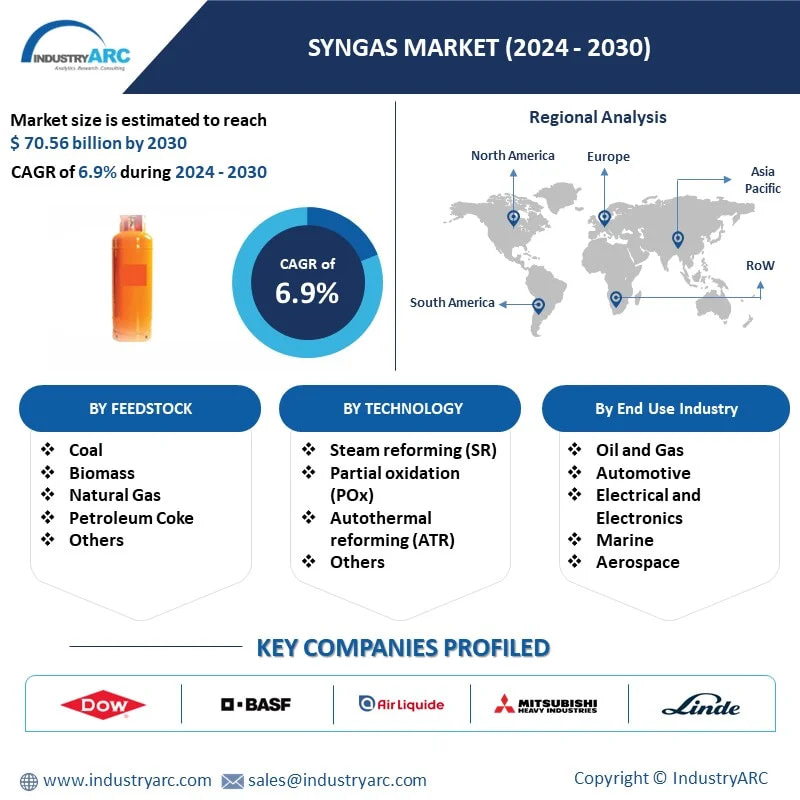

Syngas Market size is forecast to reach US$70.56 billion by 2030, after growing at a CAGR of 6.9% during 2024-2030. Syngas is a gaseous mix consisting primarily of hydrogen and carbon monoxide, which is generated from coal gasification, fluidized bed gasifier, steam reforming, and others. It can be used to fabricated chemicals such as ammonia, butanol, methanol, acetic acid, and dimethyl ether. The competence of syngas to be formed from a widespread variety of feedstock such as coal, synthetic natural gas, biomass and petroleum coke is impacting the market growth constructively. Uprising environmental concerns have been the foremost drivers for the growth of the syngas market in order to afford alternative methods of fuel production. There's a growing trend towards producing syngas from renewable sources such as biomass, municipal solid waste, and agricultural residues. This shift is driven by concerns over climate change and the desire to reduce greenhouse gas emissions. Biomass gasification, for instance, is gaining traction as it offers a carbon-neutral alternative to traditional fossil fuel-based syngas production methods. Advances in gasification technologies are driving efficiency improvements and cost reductions in syngas production. These advancements include developments in reactor design, catalysts, and process optimization techniques. Integrated gasification combined cycle (IGCC) plants, for example, are becoming more efficient in converting coal or biomass into syngas, which can then be used to generate electricity with lower emissions compared to conventional coal-fired power plants.

Market Snapshot:

The

report: “Syngas Market”- Forecast (2024-2030)”, by

IndustryARC, covers an in-depth analysis of the following segments of

the Syngas Market Industry.

By Feedstock: Coal, Biomass, Natural Gas, Petroleum

coke, and Others

By Technology: Steam

reforming (SR), Partial oxidation (POx), Autothermal reforming (ATR), and

Others

By Gasification: Fixed

Bed Gasifier, Fluidized Gasifiers, Entrained Flow Gasifiers, and Others

By Application:

Fuel, Power Generation, Generators, Refineries, Fertilizers and Pesticides,

Textiles, and Others

By End-Use Industry: Oil

and Gas, Automotive, Electrical and Electronics, Marine, Aerospace, Chemical,

Energy, Agriculture, and Others

By Geography: North

America (USA, Canada and Mexico), Europe (UK, France, Germany, Italy, Spain,

Russia, Netherlands, Belgium, and Rest of Europe), APAC (China, Japan, India,

South Korea, Australia and New Zealand, Indonesia, Taiwan, Malaysia and Rest of

APAC), South America (Brazil, Argentina, Colombia, Chile, Rest of South

America), and Rest of the world (Middle East and Africa).

Key Takeaways

·

Asia Pacific dominates

the Syngas Market owing to rapid increase in Chemical and Oil and Gas

sector. For instance, an investment of US$107.4 billion is estimated in the

Indian chemicals and petrochemicals sector by 2025

·

The market drivers and restraints have

been assessed to understand their impact over the forecast period.

·

The report further identifies the key

opportunities for growth while also detailing the key challenges and possible

threats.

·

The other key areas of focus include

the various applications and end use industry in Syngas Market and their

specific segmented revenue.

· The fuel application is expected to augment the syngas market’s growth over the forecast period due to increase in the consumption of liquid and gaseous fuels in various end-use industry.

Syngas Market Segment Analysis - By Feedstock

Coal segment held the largest share of 40% in the Syngas Market in 2023. Coal is primarily used as a fuel. The production of syngas, a mixture consisting primarily of carbon monoxide, carbon dioxide, hydrogen, natural gas, and water vapor from coal and water, and oxygen is majorly achieved by the gasification of coal. Coal formulates a rich energy resource and utilizing its energy requires a greener and cleaner approach. This is likely to initiate research for widening efficient and eco-friendly coal technologies. The high availability of coal for energy production and the excellent compatibility of the feedstock with various syngas production technologies further drives the growth of the coal segment in the syngas market.

Syngas Market Segment Analysis - By Gasification

Fluidized Gasifiers segment held the largest share in the Syngas

Market in 2023. This segment holds the largest share in the syngas market as

they are best suited to relatively reactive coals, low rank coals, and other

fuels such as biomass. These gasifiers engage back-mixing, and effectively

admix feed coal elements with coal particles previously enduring gasification.

It is normally use to sustain fluidization, or suspension of coal particles

within the gasifier, coal of small particles sizes. The decent fluidized bed

devices present a carbon conversion of 97% and in contrast, both entrained-flow

and moving-beds processes offer about 99%. The requirement for fluidized

gasifiers as an alternative for clean energy supply is increasing continuously

with its increased approval in the industrial sectors of oil and gas,

chemicals, power, and others. Due to its properties like fuel flexibility and

oxidant to certify effective heat and mass transfer, and their aptitude to deal

with small particles the demands are escalation in the end-use industries which

enhance the growth of syngas market.

Syngas Market Segment Analysis - By Application

Fuel segment held the largest share in the Syngas Market in 2023. The demand for syngas is rapidly increasing mostly in liquid fuel, gaseous fuel, and hydrogen-based electricity. Fuel is produced from syngas as it is obtained from waste materials which would otherwise be thrown away. Ethanol is obtained from syngas which is currently use as biofuel which help reduce greenhouse gas effects and lower domestic dependence on foreign petroleum. Syngas can be used to produce hydrogen, has the potential to be efficient as a fuel source. Hydrogen-based electricity produce no carbon or any harmful byproducts to the atmosphere. Syngas is also use as an intermediate to produce other chemicals. It also extends potential for greenhouse gas emissions in challenging activities, thereby offering significant life cycle reductions as compared to crude oil derivatives which directly boost the growth of syngas market.

Syngas Market Segment Analysis - By End-Use Industry

Chemical segment held the largest share in the Syngas Market in

2022 and is growing at a CAGR of 9.4% during 2024-2030. Syngas is widely used

in the processing of chemicals for manufacturing fertilizers, petrochemicals,

and oxo chemicals, and others. The chemicals segment is fragmented by

derivative into methanol, ammonia, and FT synthesis products. Ammonia is the

most manufactured chemical in the world and widely use in production of

fertilizers and plant nutrition products. And with the increasing population,

redoubled demand for food crops. The need to increase yield per unit of

cultivated land in order to meet increasing production requirements is driving

large-scale adoption of fertilizers in agriculture sector. As ammonia is a key

basic material used as fertilizers, its demand is rising. For instance, global

production of ammonia is about 180 million metric tons annually, and 120 ports

are fitted out with ammonia terminals. Ammonia being the major chemical used in

the production of fertilizers is the major motivation for the growth of the

chemical segment for the syngas market.

Syngas Market Segment Analysis -

By Geography

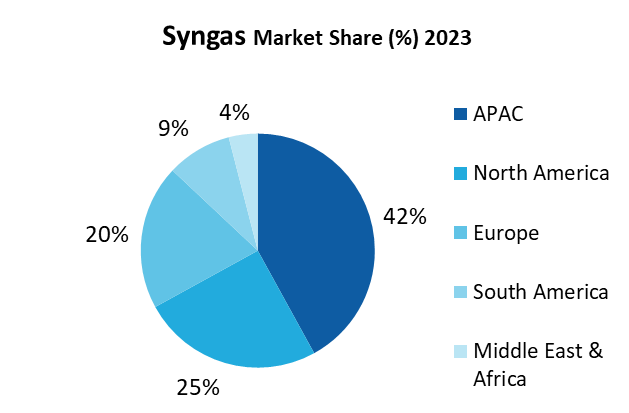

Asia-Pacific region held the largest share in the Syngas in 2023

up to 42% followed by North America and Europe. The region is the largest

consumer in the chemical industry which offers high growth opportunities for

the syngas market. The demand for syngas is rapidly rising in the Asia-Pacific

countries such as China, India, and Japan in various applications specially in

chemicals, fuel, and electricity. In addition, the growth is attributed to the

high availability of coal reserves in countries, for instance, World coal

reserves in 2023 stood at 1074 billion tonnes and China holds about 13% of it

and on the other hand, India has produced about 729 million tonnes of coal in

2023. Due to increasing demand of syngas in the region, new production plants

of syngas are being constructed, for instance, Air Products, one of the world's

largest hydrogen producer, is all set to launch a 30 tonnes per day liquid

hydrogen production plant in eastern China in 2023. Moreover, the consumption

of both liquid and gaseous fuels is increasing exponentially in the country.

This is anticipated to enhance the growth of syngas market over the forecast

period.

For more details on this report - Request for Sample

Syngas Market Drivers

Usage of syngas in various industrial applications

Rising demand for fuels, fertilizers in agricultural products and

others are influencing the growth of the syngas market. Polygeneration is the

leading factor that is boosting the syngas market due to the reason that it can

be used to derive fuels and chemicals for the purpose of power generation.

Furthermore, syngas is use to produce Ammonia which is used to produce

nitrogen-based fertilizer for agricultural sectors. In 2022, about 15.5 million

tons of total nitrogen-based fertilizers used for agricultural purposes in

Europe. Therefore, the factors are expected to show a significant impact on the

market in the forecast years. The increasing use of the derivatives in

different industrial applications is driving the demand of syngas market.

Syngas for the production of Natural Gas

Syngas is primarily used to produce SNG that is used in the form

of Liquified Natural Gas (LNG) and Compressed Natural Gas (CNG) in various

industries including railways, marine, transportation and others. It can also

be utilized as fuel gas engines for power supply owing to benefits such as low

energy costs, increased stability and predictability. The increasing

urbanization and rising income are accelerating the number of passengers which

apparently drives the growth for the railway sector, for instance, compared to

2019 the revenue for Canadian railways anticipated increase of 10% in 2022.

Whereas, India’s export of railways has grown at a CAGR of 23.51% during 2024-2030.

Exports of railways in 2022 stood at US$635 million.

Syngas Market Challenges

Heavy capital investments

One of the major restraints to the market is the high capital

investments requirements and the long duration and time taken for the

installation latest gasification techniques in the operational plants. And

moreover, no existing commercial catalyst and usually requires oxygen

plant. Besides, the plant has to build in such an area where there is constant

availability of the required feedstock and would require heat and mass

management. The limitation with the installation plant to a very extend hamper

the growth of syngas market.

Syngas Market Landscape

Technology launches, acquisitions and R&D activities are key

strategies adopted by players in the Syngas. Major players in the Syngas Market

are Dow Chemical, BASF, KBR, Mitsubishi Heavy Industries, Oxea, Methanex, Linde

PLC, and Air Liquide.

Acquisitions/Technology Launches/ Product Launches

· In July 2022, Maire Tecnimont SpA announced that NextChem had secured a contract from Storengy to assess the feasibility of establishing a waste wood and solid recovered fuel conversion plant in France, aimed at producing biomethane. NextChem will provide technical expertise and cost assessments for the syngas purification process, methanation units, and methane enhancement.

·

In June 2022, Shell PLC forged a

decarbonization pact with Osaka Gas Co. and Tokyo Gas Co., focusing on natural

gas and carbon capture, utilization, and storage (CCUS) initiatives. These

Japanese firms aim to potentially substitute 1% of their current gas supply

with biomethane-derived synthetic gas, or syngas, by the year 2030.

LIST OF TABLES

1.Global MARKET SEGMENTATION Market 2023-2030 ($M)1.1 End-user Industry Market 2023-2030 ($M) - Global Industry Research

1.1.1 Power Generation Market 2023-2030 ($M)

1.1.2 Chemicals Market 2023-2030 ($M)

1.1.3 Liquid Fuels Market 2023-2030 ($M)

1.1.4 Gaseous Fuels Market 2023-2030 ($M)

1.2 Feedstock Market 2023-2030 ($M) - Global Industry Research

1.2.1 Coal Market 2023-2030 ($M)

1.2.2 Natural Gas Market 2023-2030 ($M)

1.2.3 Petroleum Market 2023-2030 ($M)

1.2.4 Pet-coke Market 2023-2030 ($M)

1.2.5 Biomass Market 2023-2030 ($M)

1.3 Technology Market 2023-2030 ($M) - Global Industry Research

1.3.1 Steam Reforming Market 2023-2030 ($M)

1.3.2 Partial Oxidation Market 2023-2030 ($M)

1.3.3 Auto-thermal Reforming Market 2023-2030 ($M)

1.3.4 Combined or Two-step Reforming Market 2023-2030 ($M)

1.3.5 Biomass Gasification Market 2023-2030 ($M)

1.4 Gasifier Type Market 2023-2030 ($M) - Global Industry Research

1.4.1 Fixed Bed Market 2023-2030 ($M)

1.4.2 Entrained Flow Market 2023-2030 ($M)

1.4.3 Fluidized Bed Market 2023-2030 ($M)

2.Global COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

2.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Global Industry Research

3.Global MARKET SEGMENTATION Market 2023-2030 (Volume/Units)

3.1 End-user Industry Market 2023-2030 (Volume/Units) - Global Industry Research

3.1.1 Power Generation Market 2023-2030 (Volume/Units)

3.1.2 Chemicals Market 2023-2030 (Volume/Units)

3.1.3 Liquid Fuels Market 2023-2030 (Volume/Units)

3.1.4 Gaseous Fuels Market 2023-2030 (Volume/Units)

3.2 Feedstock Market 2023-2030 (Volume/Units) - Global Industry Research

3.2.1 Coal Market 2023-2030 (Volume/Units)

3.2.2 Natural Gas Market 2023-2030 (Volume/Units)

3.2.3 Petroleum Market 2023-2030 (Volume/Units)

3.2.4 Pet-coke Market 2023-2030 (Volume/Units)

3.2.5 Biomass Market 2023-2030 (Volume/Units)

3.3 Technology Market 2023-2030 (Volume/Units) - Global Industry Research

3.3.1 Steam Reforming Market 2023-2030 (Volume/Units)

3.3.2 Partial Oxidation Market 2023-2030 (Volume/Units)

3.3.3 Auto-thermal Reforming Market 2023-2030 (Volume/Units)

3.3.4 Combined or Two-step Reforming Market 2023-2030 (Volume/Units)

3.3.5 Biomass Gasification Market 2023-2030 (Volume/Units)

3.4 Gasifier Type Market 2023-2030 (Volume/Units) - Global Industry Research

3.4.1 Fixed Bed Market 2023-2030 (Volume/Units)

3.4.2 Entrained Flow Market 2023-2030 (Volume/Units)

3.4.3 Fluidized Bed Market 2023-2030 (Volume/Units)

4.Global COMPETITIVE LANDSCAPE Market 2023-2030 (Volume/Units)

4.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 (Volume/Units) - Global Industry Research

5.North America MARKET SEGMENTATION Market 2023-2030 ($M)

5.1 End-user Industry Market 2023-2030 ($M) - Regional Industry Research

5.1.1 Power Generation Market 2023-2030 ($M)

5.1.2 Chemicals Market 2023-2030 ($M)

5.1.3 Liquid Fuels Market 2023-2030 ($M)

5.1.4 Gaseous Fuels Market 2023-2030 ($M)

5.2 Feedstock Market 2023-2030 ($M) - Regional Industry Research

5.2.1 Coal Market 2023-2030 ($M)

5.2.2 Natural Gas Market 2023-2030 ($M)

5.2.3 Petroleum Market 2023-2030 ($M)

5.2.4 Pet-coke Market 2023-2030 ($M)

5.2.5 Biomass Market 2023-2030 ($M)

5.3 Technology Market 2023-2030 ($M) - Regional Industry Research

5.3.1 Steam Reforming Market 2023-2030 ($M)

5.3.2 Partial Oxidation Market 2023-2030 ($M)

5.3.3 Auto-thermal Reforming Market 2023-2030 ($M)

5.3.4 Combined or Two-step Reforming Market 2023-2030 ($M)

5.3.5 Biomass Gasification Market 2023-2030 ($M)

5.4 Gasifier Type Market 2023-2030 ($M) - Regional Industry Research

5.4.1 Fixed Bed Market 2023-2030 ($M)

5.4.2 Entrained Flow Market 2023-2030 ($M)

5.4.3 Fluidized Bed Market 2023-2030 ($M)

6.North America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

7.South America MARKET SEGMENTATION Market 2023-2030 ($M)

7.1 End-user Industry Market 2023-2030 ($M) - Regional Industry Research

7.1.1 Power Generation Market 2023-2030 ($M)

7.1.2 Chemicals Market 2023-2030 ($M)

7.1.3 Liquid Fuels Market 2023-2030 ($M)

7.1.4 Gaseous Fuels Market 2023-2030 ($M)

7.2 Feedstock Market 2023-2030 ($M) - Regional Industry Research

7.2.1 Coal Market 2023-2030 ($M)

7.2.2 Natural Gas Market 2023-2030 ($M)

7.2.3 Petroleum Market 2023-2030 ($M)

7.2.4 Pet-coke Market 2023-2030 ($M)

7.2.5 Biomass Market 2023-2030 ($M)

7.3 Technology Market 2023-2030 ($M) - Regional Industry Research

7.3.1 Steam Reforming Market 2023-2030 ($M)

7.3.2 Partial Oxidation Market 2023-2030 ($M)

7.3.3 Auto-thermal Reforming Market 2023-2030 ($M)

7.3.4 Combined or Two-step Reforming Market 2023-2030 ($M)

7.3.5 Biomass Gasification Market 2023-2030 ($M)

7.4 Gasifier Type Market 2023-2030 ($M) - Regional Industry Research

7.4.1 Fixed Bed Market 2023-2030 ($M)

7.4.2 Entrained Flow Market 2023-2030 ($M)

7.4.3 Fluidized Bed Market 2023-2030 ($M)

8.South America COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

8.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

9.Europe MARKET SEGMENTATION Market 2023-2030 ($M)

9.1 End-user Industry Market 2023-2030 ($M) - Regional Industry Research

9.1.1 Power Generation Market 2023-2030 ($M)

9.1.2 Chemicals Market 2023-2030 ($M)

9.1.3 Liquid Fuels Market 2023-2030 ($M)

9.1.4 Gaseous Fuels Market 2023-2030 ($M)

9.2 Feedstock Market 2023-2030 ($M) - Regional Industry Research

9.2.1 Coal Market 2023-2030 ($M)

9.2.2 Natural Gas Market 2023-2030 ($M)

9.2.3 Petroleum Market 2023-2030 ($M)

9.2.4 Pet-coke Market 2023-2030 ($M)

9.2.5 Biomass Market 2023-2030 ($M)

9.3 Technology Market 2023-2030 ($M) - Regional Industry Research

9.3.1 Steam Reforming Market 2023-2030 ($M)

9.3.2 Partial Oxidation Market 2023-2030 ($M)

9.3.3 Auto-thermal Reforming Market 2023-2030 ($M)

9.3.4 Combined or Two-step Reforming Market 2023-2030 ($M)

9.3.5 Biomass Gasification Market 2023-2030 ($M)

9.4 Gasifier Type Market 2023-2030 ($M) - Regional Industry Research

9.4.1 Fixed Bed Market 2023-2030 ($M)

9.4.2 Entrained Flow Market 2023-2030 ($M)

9.4.3 Fluidized Bed Market 2023-2030 ($M)

10.Europe COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

10.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

11.APAC MARKET SEGMENTATION Market 2023-2030 ($M)

11.1 End-user Industry Market 2023-2030 ($M) - Regional Industry Research

11.1.1 Power Generation Market 2023-2030 ($M)

11.1.2 Chemicals Market 2023-2030 ($M)

11.1.3 Liquid Fuels Market 2023-2030 ($M)

11.1.4 Gaseous Fuels Market 2023-2030 ($M)

11.2 Feedstock Market 2023-2030 ($M) - Regional Industry Research

11.2.1 Coal Market 2023-2030 ($M)

11.2.2 Natural Gas Market 2023-2030 ($M)

11.2.3 Petroleum Market 2023-2030 ($M)

11.2.4 Pet-coke Market 2023-2030 ($M)

11.2.5 Biomass Market 2023-2030 ($M)

11.3 Technology Market 2023-2030 ($M) - Regional Industry Research

11.3.1 Steam Reforming Market 2023-2030 ($M)

11.3.2 Partial Oxidation Market 2023-2030 ($M)

11.3.3 Auto-thermal Reforming Market 2023-2030 ($M)

11.3.4 Combined or Two-step Reforming Market 2023-2030 ($M)

11.3.5 Biomass Gasification Market 2023-2030 ($M)

11.4 Gasifier Type Market 2023-2030 ($M) - Regional Industry Research

11.4.1 Fixed Bed Market 2023-2030 ($M)

11.4.2 Entrained Flow Market 2023-2030 ($M)

11.4.3 Fluidized Bed Market 2023-2030 ($M)

12.APAC COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

12.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

13.MENA MARKET SEGMENTATION Market 2023-2030 ($M)

13.1 End-user Industry Market 2023-2030 ($M) - Regional Industry Research

13.1.1 Power Generation Market 2023-2030 ($M)

13.1.2 Chemicals Market 2023-2030 ($M)

13.1.3 Liquid Fuels Market 2023-2030 ($M)

13.1.4 Gaseous Fuels Market 2023-2030 ($M)

13.2 Feedstock Market 2023-2030 ($M) - Regional Industry Research

13.2.1 Coal Market 2023-2030 ($M)

13.2.2 Natural Gas Market 2023-2030 ($M)

13.2.3 Petroleum Market 2023-2030 ($M)

13.2.4 Pet-coke Market 2023-2030 ($M)

13.2.5 Biomass Market 2023-2030 ($M)

13.3 Technology Market 2023-2030 ($M) - Regional Industry Research

13.3.1 Steam Reforming Market 2023-2030 ($M)

13.3.2 Partial Oxidation Market 2023-2030 ($M)

13.3.3 Auto-thermal Reforming Market 2023-2030 ($M)

13.3.4 Combined or Two-step Reforming Market 2023-2030 ($M)

13.3.5 Biomass Gasification Market 2023-2030 ($M)

13.4 Gasifier Type Market 2023-2030 ($M) - Regional Industry Research

13.4.1 Fixed Bed Market 2023-2030 ($M)

13.4.2 Entrained Flow Market 2023-2030 ($M)

13.4.3 Fluidized Bed Market 2023-2030 ($M)

14.MENA COMPETITIVE LANDSCAPE Market 2023-2030 ($M)

14.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements Market 2023-2030 ($M) - Regional Industry Research

LIST OF FIGURES

1.US Syngas Market Revenue, 2023-2030 ($M)2.Canada Syngas Market Revenue, 2023-2030 ($M)

3.Mexico Syngas Market Revenue, 2023-2030 ($M)

4.Brazil Syngas Market Revenue, 2023-2030 ($M)

5.Argentina Syngas Market Revenue, 2023-2030 ($M)

6.Peru Syngas Market Revenue, 2023-2030 ($M)

7.Colombia Syngas Market Revenue, 2023-2030 ($M)

8.Chile Syngas Market Revenue, 2023-2030 ($M)

9.Rest of South America Syngas Market Revenue, 2023-2030 ($M)

10.UK Syngas Market Revenue, 2023-2030 ($M)

11.Germany Syngas Market Revenue, 2023-2030 ($M)

12.France Syngas Market Revenue, 2023-2030 ($M)

13.Italy Syngas Market Revenue, 2023-2030 ($M)

14.Spain Syngas Market Revenue, 2023-2030 ($M)

15.Rest of Europe Syngas Market Revenue, 2023-2030 ($M)

16.China Syngas Market Revenue, 2023-2030 ($M)

17.India Syngas Market Revenue, 2023-2030 ($M)

18.Japan Syngas Market Revenue, 2023-2030 ($M)

19.South Korea Syngas Market Revenue, 2023-2030 ($M)

20.South Africa Syngas Market Revenue, 2023-2030 ($M)

21.North America Syngas By Application

22.South America Syngas By Application

23.Europe Syngas By Application

24.APAC Syngas By Application

25.MENA Syngas By Application