Email

Email Print

Print

White Cement Market - Industry Analysis, Market Size, Share, Trends, Application Analysis, Growth And Forecast 2024-2030

White Cement Market Overview

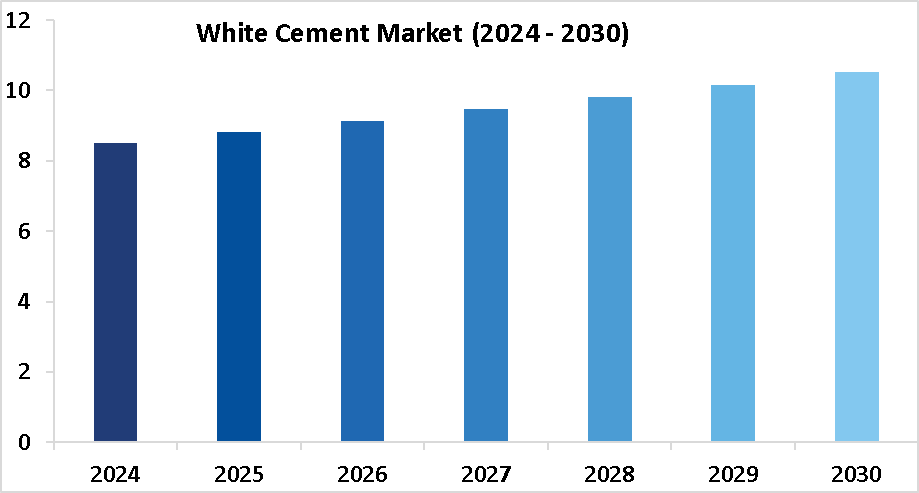

The White Cement Market size is forecast to reach USD 10.5 billion by 2030, after growing at a CAGR of 3.8% during the forecast period 2024-2030. White cement, traditionally used in architectural applications and specialty concrete products, is witnessing several notable trends reshaping its market landscape. One prominent trend is the increasing demand for white cement in decorative and aesthetic construction projects worldwide. Architects and designers are incorporating white cement into building facades, flooring, and decorative elements due to its versatility, durability, and ability to enhance the visual appeal of structures. Additionally, white cement is gaining traction in the production of high-quality tiles, countertops, and precast elements, driven by the growing preference for sophisticated and modern interior designs.

The significant trend in the white cement market is the focus on sustainability and eco-friendly manufacturing processes. Companies are investing in sustainable sourcing of raw materials and implementing energy-efficient production techniques to reduce environmental impact. Moreover, advancements in technology and innovation are enabling manufacturers to develop white cement formulations with enhanced performance characteristics, such as improved workability, setting time, and strength development. Furthermore, the construction industry's emphasis on premiumization and luxury is driving the demand for white cement-based products in high-end residential and commercial projects. White cement offers a luxurious aesthetic and contributes to the creation of sophisticated architectural designs, thereby fueling its adoption among upscale clientele. Additionally, the expansion of infrastructure projects, particularly in emerging economies, presents lucrative opportunities for white cement manufacturers to capitalize on the growing demand for premium construction materials.

Market Snapshot:

Report Coverage

The report “White Cement Market – Forecast (2024-2030)”, by IndustryARC, covers an in-depth analysis of the following segments of the White Cement Market.

By Type: White Portland Cement, White Masonry Cement and Others

By End Use: Residential, Commercial and Industrial

By Geography: North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Russia, Netherlands and Others), APAC (China, Japan India, South Korea, Australia & New Zealand, Indonesia, Malaysia, Taiwan and Others), South America (Brazil, Argentina, Chile, Colombia and others), and RoW (Middle East and Africa).

Key Takeaways

- APAC held the largest market share with 55% in 2023. According to BMI estimates, India's household spending is forecasted to surpass $3 trillion as disposable income grows at a compounded annual rate of 14.6% until 2027, with an anticipated 25.8% of Indian households reaching $10,000 in annual disposable income by then. The rising disposable income levels in APAC countries result in higher consumer spending on luxury housing, renovation projects, and premium construction materials. White cement is often chosen for upscale residential and commercial properties, fueled by the aspirational lifestyle choices of the growing middle-class population across the APAC region.

- White cement is experiencing a surge in demand due to extensive infrastructure projects worldwide. As urbanization and construction activities escalate, the need for high-quality materials like white cement grows. Its aesthetic appeal, durability, and versatility make it a preferred choice for architectural designs, residential buildings, commercial complexes, and infrastructure developments.

- The rise in demand for decorative concrete applications fuels the demand for white cement. From polished floors to intricate sculptures, white cement offers a pristine canvas for creative expression in architectural and interior designs. Its ability to achieve vibrant colors, smooth finishes, and intricate detailing enhances the aesthetic appeal of various construction projects, driving its adoption across residential and commercial sectors.

By Type - Segment Analysis

White Portland dominated the White Cement Market in 2023. White Portland cement serves as a crucial driver in the White Cement Market, influenced by several factors shaping the industry landscape. The versatility and compatibility with various construction applications propel demand, especially in architectural and decorative projects where aesthetic appeal is paramount. Additionally, the growing preference for eco-friendly and sustainable construction materials drives the adoption of white Portland cement due to its lower carbon footprint compared to traditional gray cement. Moreover, advancements in manufacturing processes and technologies enhance the quality and performance of white Portland cement, meeting stringent industry standards and consumer expectations for durability and strength. Furthermore, the rise in urbanization and infrastructure development projects globally fuels the demand for white Portland cement as a key ingredient in high-quality concrete formulations, driving growth and innovation in the white cement market.

By End Use - Segment Analysis

Residential end use dominated the White Cement Market in 2023. The burgeoning residential sector, fueled by urbanization and population growth, propels the need for white cement in various applications such as flooring, walls, and decorative elements. As homeowners increasingly prioritize aesthetics and luxury, white cement emerges as a preferred choice due to its ability to impart a clean, modern look to residential spaces. Moreover, the surge in renovation and remodeling activities further boosts the consumption of white cement in residential settings, as homeowners seek to upgrade and enhance the visual appeal of their properties. Additionally, the growing trend towards sustainable and eco-friendly construction materials amplifies the demand for white cement, given its durability, energy efficiency, and recyclability, thereby driving its adoption in residential projects. These factors collectively contribute to the sustained growth and prominence of white cement in the residential segment of the construction industry.

By Geography - Segment Analysis

APAC dominated the White Cement Market in 2023. The APAC White Cement Market is projected to experience significant growth during the forecast period. The APAC White Cement market is supported by rapid urbanization and infrastructural development projects across countries like China, India, and Southeast Asian nations contribute significantly to the demand for white cement. The region's burgeoning construction industry, particularly in residential and commercial sectors, fuels the need for high-quality building materials, including white cement, renowned for its aesthetic appeal and durability. Additionally, the growing trend towards modern architectural designs, coupled with increased disposable income in emerging economies, fosters consumer preference for luxury finishes and premium construction materials like white cement. Moreover, government initiatives aimed at promoting sustainable construction practices and eco-friendly materials further propel the adoption of white cement in the APAC region, reflecting a shift towards environmentally conscious building solutions. Overall, these drivers underscore the promising outlook for the white cement market in the APAC region, driving innovation and investment opportunities in the construction sector.

For More Details on This Report - Request for Sample

Drivers – White Cement Market

Growing use of white cement in infrastructure development projects

Infrastructure projects, including bridges, roads, dams, and airports, increasingly utilize white cement due to its durability, aesthetic appeal, and ability to withstand harsh environmental conditions. White cement's versatility and strength make it a preferred choice for various construction applications, particularly in projects where longevity and resilience are paramount. Moreover, the trend towards modern architectural designs and the emphasis on sustainable construction practices further contribute to the rising demand for white cement in infrastructure development. As governments and private investors continue to invest in improving and expanding infrastructure globally, the demand for white cement is expected to escalate, driving growth and innovation in the construction industry.

Growing demand for high-quality building materials

With increasing emphasis on architectural aesthetics and structural integrity, builders and developers are turning towards premium materials like white cement to meet stringent quality standards. White cement's exceptional properties, including superior strength, durability, and versatility, make it a preferred choice for various construction applications, ranging from residential projects to commercial complexes and infrastructure developments. Moreover, the growing awareness among consumers about the importance of using high-quality materials to enhance the longevity and visual appeal of structures further propels the demand for white cement. As sustainability and eco-consciousness gain traction in the construction industry, the inherent eco-friendly characteristics of white cement also contribute to its rising popularity among environmentally conscious builders and developers. This trend underscores the significant role of the growing demand for high-quality building materials in driving the white cement market forward.

Challenges – White Cement Market

Rising energy costs impacting overall production expenses

As energy-intensive manufacturing processes are integral to white cement production, increases in energy prices directly affect production costs. The extraction and processing of raw materials, including limestone and gypsum, require substantial energy inputs. Additionally, the high-temperature kiln processes involved in white cement manufacturing demand considerable energy consumption. Fluctuations in energy prices, driven by factors such as geopolitical tensions and supply chain disruptions, further exacerbate cost pressures on white cement producers. Rising energy expenses not only inflate operational costs but also pose challenges in maintaining competitive pricing and profit margins in the market. To mitigate these challenges, companies may explore energy-efficient technologies, invest in renewable energy sources, and optimize production processes to enhance cost-effectiveness and sustainability in the white cement manufacturing industry. These limitations are projected to limit market revenue growth.

Market Landscape

Technology launches, acquisitions, and R&D activities are key strategies adopted by players in the White Cement Market. in 2023, The major players in the White Cement Market are Cimsa Cimento, JK Cement, SOTACIB, CEMEX S.A.B. de C.V., Birla White, Federal White Cement, Saveh Cement co., Cementos Portland Valderrivas, S.A., Aalborg Portland Holding A/S, CRH (SLOVAKIA) A.S., and Others.

Developments:

- In July 2023, Dyckerhoff introduced Dyckerhoff Weiss Blue Star, a pozzolanic white cement with lower CO2 emissions, approved by VDZ, now produced at the Amöneburg plant, offering a 15% reduction in CO2 compared to CEM I cements and distinguished as a blended white cement.

For more Chemicals and Materials Market reports - Please click here

1. White Cement Market- Overview

1.1. Definitions and Scope

2. White Cement Market- Executive Summary

3. White Cement Market- Comparative Analysis

3.1. Company Benchmarking - Key Companies

3.2. Global Financial Analysis - Key Companies

3.3. Market Share Analysis - Key Companies

3.4. Patent Analysis

3.5. Pricing Analysis

4. White Cement Market- Start-up Companies Scenario

4.1. Key Start-up Company Analysis by

4.1.1. Investment

4.1.2. Revenue

4.1.3. Venture Capital and Funding Scenario

5. White Cement Market– Market Entry Scenario Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Case Studies of Successful Ventures

6. White Cement Market- Forces

6.1. Market Drivers

6.2. Market Constraints

6.3. Market Challenges

6.4. Porter's Five Force Model

6.4.1. Bargaining Power of Suppliers

6.4.2. Bargaining Powers of Customers

6.4.3. Threat of New Entrants

6.4.4. Rivalry Among Existing Players

6.4.5. Threat of Substitutes

7. White Cement Market– Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Market Life Cycle

8. White Cement Market– by Type (Market Size – $Million/$Billion)

8.1. White Portland Cement

8.2. White Masonry Cement

8.3. Others

9. White Cement Market – by End Use (Market Size – $Million/$Billion)

9.1. Residential

9.2. Commercial

9.3. Industrial

10. White Cement Market – by Geography (Market Size – $Million/$Billion)

10.1. North America

10.1.1. U.S

10.1.2. Canada

10.1.3. Mexico

10.2. Europe

10.2.1. Germany

10.2.2. France

10.2.3. UK

10.2.4. Italy

10.2.5. Spain

10.2.6. Belgium

10.2.7. Netherlands

10.2.8. Rest of Europe

10.3. Asia-Pacific

10.3.1. China

10.3.2. Japan

10.3.3. South Korea

10.3.4. India

10.3.5. Australia & New Zealand

10.3.6. Indonesia

10.3.7. Malaysia

10.3.8. Taiwan

10.3.9. Rest of Asia-Pacific

10.4. South America

10.4.1. Brazil

10.4.2. Argentina

10.4.3. Chile

10.4.4. Colombia

10.4.5. Rest of South America

10.5. Rest of The World

10.5.1. Middle East

10.5.2. Africa

11. White Cement Market– Entropy

11.1 New product launches

11.2 M&A’s, collaborations, JVs and partnerships

11.2 M&A’s, collaborations, JVs and partnerships

12. White Cement Market– Industry/Segment Competition Landscape

12.1. Market Share Analysis

12.1.1. Market Share by Product Type – Key Companies

12.1.2. Market Share by Region – Key Companies

12.1.3. Market Share by Country – Key Companies

12.2. Competition Matrix

12.3. Best Practices for Companies

13. White Cement Market– Key Company List by Country Premium

14. White Cement Market- Company Analysis

14.1. Cimsa Cimento

14.2. JK Cement

14.3. SOTACIB

14.4. CEMEX S.A.B. de C.V.

14.5. Birla White

14.6. Federal White Cement

14.7. Saveh Cement co.

14.8. Cementos Portland Valderrivas, S.A.

14.9. Aalborg Portland Holding A/S

14.10. CRH (SLOVAKIA) A.S.

"Financials to the Private Companies would be provided on best-effort basis."

Connect with our experts to get customized reports that best suit your requirements. Our reports include global-level data, niche markets and competitive landscape.