Email

Email Print

Print

Ceramics Market Overview:

The Ceramics market size is forecast to reach USD$360billion by 2030,

after growing at a CAGR of 4.5% during 2024-2030.The expansion is

ascribed to the wide use in a variety of applications ranging from refrigerator

magnets to a growing number of sectors such as metals manufacturing and

processing, aerospace, electronics, automotive, and personnel protection.

Nanotechnology, double-vitrified tiles, and 3D printing are identified as

ongoing trends in ceramic tile manufacturing.

The necessity for reliable materials such as ceramics has increased due to the rising need for high-quality and functional safety in medical equipment. These are favored in the medical sector due to their adaptable and scalable qualities that may be adapted to specific application needs. Acetabular cups and femoral heads for hip replacement, dental implants and restorations, bone fillers, and scaffolds for tissue engineering are just a few of the medical industry's many uses for ceramics.

Report Coverage:

The report “Ceramics Market–

Forecast (2024-2030)”,by IndustryARC, covers an in-depth analysis of the

following segments of the ceramics market.

By Type: Classic Ceramics, Advanced Ceramics

By Material: Classic (Clay, Quartz, Other

Natural Materials), Advanced (Alumina, Silicon Carbide, Zirconia, Titanate,

Silicon Nitride, Others)

By Product: Classic Ceramics (Glazed, Porcelain, Other Products), Advanced

Ceramics (Monolithic Ceramics, Ceramic Coatings, Ceramic Matrix Composites)

By Application: Tiles, Sanitary ware, Pottery, Bricks & Pipes, Abrasives,

Electrical Equipment, Wear Parts, Engine Parts, Others

By End-User: Building & Construction, Medical, Automotive, Aerospace, Electrical

& Electronics, Others

By Geography: North America, South America, Europe, Asia-Pacific, and RoW

Key Takeaways:

· The growth in aircraft production is driving the ceramics market. For instance, Boeing intends to produce at least 50 MAX versions per month by 2025 from a usual output of 31 MAX per month and is confident in the coordinated supply chain's capacity to meet this target. The ceramics are used for shielding a hot-running airplane engine from damaging other components, used as high-stress, high-temperature, and lightweight bearing and structural components in airframes, missile nose cones (shielding the missile internals from heat), and others.

· The 5G network will also drive

ceramics growth for millimeter wave applications, which require small parts and

tight tolerances. Since not all of these components can be manufactured with

existing technology, there is a growing need to advance the current

manufacturing infrastructure to fill this space in the industry. Thus, the

demand for ceramics is expected to increase for 5G wireless communication

systems.

· The U.S. is the dominant Country in

the ceramics market, driven by the increasing demand from construction and the

easy availability of raw materials. For instance, according to the National

Association of Home Builders, the number of housings starts in the U.S.

increased from 1,250 in 2018 to 1,553 in 2022.

By Type - Segment Analysis:

Classic ceramics dominated the ceramics market in 2023.Improvements

in building design, new building construction, and rising consumer expectations

for infrastructure development resulted in rising market demands for the

development of ceramics, which supports the growth of the classic ceramics

market.

The strong performance of ceramic tiles is driven by a vibrant

construction industry. For instance, when it comes to the United States

construction industry, single-family new home starts increased 13.4% from the

previous year to 1.12 million units in 2021, accounting for 70.4% of total home

starts and multi-family starts rose 21.3% from 2020 to 472,100 units, according

to the U.S. Census Bureau. As they are necessary components for any real estate

construction, these new home start growth rates will increase demand for

ceramics, particularly for tiles and sanitaryware. As a result, both of these applications

present appealing development prospects for both current participants and

potential new startups.

By Application - Segment Analysis:

Floor tiles dominated the ceramics market in 2023. A five-year

forecast survey conducted by the Research Department of the Italian Ceramic

Machinery and Equipment Manufacturers' Association predicts that from 2021 to

2025, the production of ceramic tiles will increase globally at a rate of 5%

annually. Owing to incredibly resilient and hygienic buildings, tiles enhance

any application with unparalleled beauty, ceramic tiles are commonly used

indoors to cover floors, walls, kitchen countertops, and fireplaces. Also,

Ceramic tiles are typically used to pave terraces, patios, stairways, porches,

driveways, and pool sides outdoors.

By End-User- Segment Analysis:

Building & Construction dominated the ceramics market in 2023. Factors

such as rapid urbanization, infrastructure development, and an increasing

emphasis on aesthetic appeal in construction projects contribute to the

market's expansion. For instance, according to the Japan Federation of

Construction Contractors of Japan, the number of domestic construction orders received

in FY2022 was 16.2609 trillion yen($124.43 billion), an increase of 8.4% from

FY21.

In 2023, Homes England offered construction loans ranging from

£250,000 ($2.7 million) to £10 million+ ($10.8 million) to assist

hundreds of micro and small building companies in launching their projects. The

rise in funds and loans is also anticipated to drive the market growth.

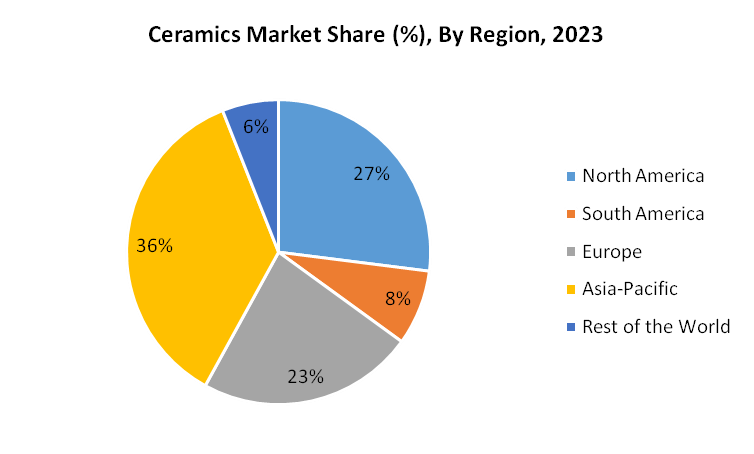

By Geography- Segment Analysis:

Asia-Pacific dominated the dominated the ceramics market in 2023.

China is a significant producer of ceramic tiles in the Asia-Pacific region.

Low production costs and a plentiful supply of raw materials are the primary

forces behind the industry's development in China. Government support like GST

on ceramic tiles, sanitary ware, and tableware lowered to 18% from 28% in

India.

The thriving construction sector in this region will be the biggest driver of the increase in ceramics consumption. For instance, according to Invest India, the construction Industry in India is expected to reach $1.4 Tn by 2025. An estimated 600 million people are likely to be living in urban centers by 2030, creating a demand for the ceramics market.

For More Details on This Report- Request for Sample

Drivers – Ceramics Market:

· Increasing Demand for Advanced Ceramics from the Electronics Sector

The demand for advanced ceramics has increased, owing

to its special features such as the wide range of electrical conductivity, that

extends more than 15 orders of magnitude and cannot be matched by any other

class of materials. They frequently allow for reduced product sizes and, hence,

more commercially appealing items when compared to metallic materials.

The wide-ranging application of advanced ceramic

materials in electrical engineering and electronics has increased over the past

year to a correspondingly high number of variants in electrically passive and

active materials. These days, a wide range of materials are available, such as

ceramics for NTC, PTC, piezoelectric, and dielectrics. The key application of

advanced ceramics is the manufacture of semiconductors. Some of the widely used

advanced ceramics in semiconductor manufacturing are silicon carbide (SiC) and

pyrolytic boron nitride (PBN). The increasing demand for advanced ceramics from

the electronics industry, especially for manufacturing semiconductors is

driving its market growth.

· Increased Spending

on Remodeling

Renovation activities are in growing demand for

easy-to-maintain, better aesthetic, durable, and moisture, fire, and

scratch-resistant tiles. Owing to the increasing comforts and interest in

bathroom renovations, consumers prefer decorative bathroom tiles and are

ensuring that the quality remains useful and noticeable for years with

different looks like Stone Bathrooms look, Timber Bathrooms look, and so on.

Increasing home renovation and

modular kitchen projects is one of the significant

global ceramic market growth drivers. For instance, the Houzz

& Home Survey of 70,000 U.S. respondents found that, in 2022, 55% of

homeowners planned to renovate their house, while 46% planned to decorate it.

In addition, homeowners with higher-budget renovations planned to spend $75,000

on projects in 2022 compared with $60,000 in 2021.

Challenges – Ceramics Market:

· Fluctuating Costs of Raw Materials

Volatile raw material

prices are a major challenge for the ceramic tile market, as they ultimately

raise production costs and reduce profit margins. Clays, silica, sand, or

feldspar are the basic raw materials. Raw material prices have risen as the

material's use has expanded into new applications. The price of bentonite clay

was approximately $67 per ton in 2018, but as its applications increased, so did

its price, which reached approximately $94 per ton in 2023. Because of the high

cost of raw materials, tile companies may lose market share; therefore,

companies must develop strategies to maintain a stronghold on the market.

Apart from machining,

the materials which are used to manufacture ceramics are more expensive. Except

for alumina and silicon, other ceramic materials such as zirconia, titanium,

and other materials are expensive, due to this, the ceramic components which

are used in aerospace, and automotive are of higher costs.

·

Machining

in Aerospace Design may Hamper the Market Growth

Despite the advantages, ceramics are not

necessarily the be-all, end-all for materials designed. Advanced ceramic

manufacturers have also found both machining and cost challenges. Ceramics are

filled with an abundance of heat-insulating properties, allowing them an

effective tool in tandem with elevated aircraft turbine temperatures. In

addition to being incredibly light and non-corrosive, these can also endure

contact with jet fuel, reach higher speeds, and cover larger geographical

areas. However, molding and using it can be sluggish and challenging.

Market Landscape:

Technology launches, acquisitions, and R&D activities are key

strategies adopted by players in the ceramics market. In 2023, the classic ceramics

market share has been consolidated by the major players accounting for 56.7% of

the share. Major players in the classic ceramics market are Asahi Glass, AGC

Ceramics, Saint-Gobain, Kyocera Corp, Mohawk Industries, Morimura Group, 3M,

Corning Inc., and Kajaria Ceramics Limited among others.

Developments:

ØIn September 2023, a multi-year supply agreement was established between ION Storage Systems (ION), a Maryland-based maker of safe, high-energy density, solid-state lithium metal batteries, and Saint-Gobain Ceramics. As per the terms of the deal, Saint-Gobain Ceramics would create premium ceramic powder using its exclusive production method.

In August 2023, Kyocera, a manufacturer of innovative ceramics worldwide, introduced INNOVATION white, a new collection of ceramic kitchen knives created by Yohei Kuwano, a celebrated designer from Japan. For a brief period, the new collection, which comes in five vivid colors, is only available on Indiegogo.

In June 2022, Mohawk Industries acquiredthe Vitromex ceramic tile business from Grupo Industrial Saltillo for $293M in cash. The acquisition is to expand its customer base, manufacturing efficiencies, and logistical capabilities in Mexican operations.

For more chemical and Materials Market reports, please click here