Email

Email Print

Print

Electronics Ceramics and Electrical Ceramics Market- Industry Analysis, Market Size, Share, Trends, Growth And Forecast 2024-2030

Electronics Ceramics and Electrical Ceramics Market Overview

The Electronics Ceramics and Electrical Ceramics Market size is estimated to grow at a CAGR of 5.2% during 2024-2030 to reach revenue of $18 billion by 2030. Electronics Ceramics and Electrical Ceramics refer to a class of ceramic materials that exhibit unique electrical properties, making them valuable for various electronic and electrical applications. These materials possess specific characteristics such as piezoelectricity, ferroelectricity, and high dielectric constants, which make them suitable for a range of technological purposes. With the global emphasis on sustainable and renewable energy sources, Electronics Ceramics and Electrical Ceramics are being developed to address challenges in energy harvesting, storage, and conversion. Innovations in ferroelectric and piezoelectric materials contribute to the creation of efficient energy harvesting devices, converting mechanical vibrations or ambient energy into electrical power. Electronics Ceramics and Electrical Ceramics are integral to the functioning of electronic devices such as smartphones, computers, sensors, and medical equipment. They play a crucial role in signal processing, energy storage, and conversion. A prominent trend in the Electronics Ceramics and Electrical Ceramics market is the increasing integration of these materials in Internet of Things (IoT) devices. As the IoT ecosystem expands, connecting devices and enabling seamless communication becomes crucial. Electronics Ceramics and Electrical Ceramics, with their unique electrical properties like piezoelectricity and high dielectric constants, play a pivotal role in sensors and transducers essential for IoT applications. These materials contribute to the development of efficient and responsive sensor technologies that enable real-time data collection and transmission. With the growing demand for smart homes, industrial automation, and wearable devices, Electronics Ceramics and Electrical Ceramics are becoming integral components, facilitating the miniaturization and enhanced functionality of IoT devices.

Electronics Ceramics and Electrical Ceramics Market Report Coverage

The report: “Electronics Ceramics and Electrical Ceramics Industry Outlook – Forecast (2024-2030)”, by IndustryARC covers an in-depth analysis of the following segments of the Electronics Ceramics and Electrical Ceramics industry.

By Product: Dielectric Ceramics, Ceramic insulators, Piezoelectric Ceramics, Ferroelectric Ceramics.

By Application: Capacitors, Data Storage Devices, Optoelectronic Devices, Actuators and Sensors, Power Distribution Devices, and Others.

By End Use: Automotive, Electronics, Energy & Power, Others.

By Geography: North America (Canada, Mexico, U.S), South America (Argentina, Brazil, Chile, Colombia, Rest of South America), Europe (France, Germany, Italy, Netherlands, Russia, Spain, UK, Rest of Europe), APAC (Australia, China, India, Taiwan, Japan, Malaysia, South Korea, Rest of APAC), and RoW (Africa, Middle East)

For more details on this report - Request for Sample

Key Takeaways

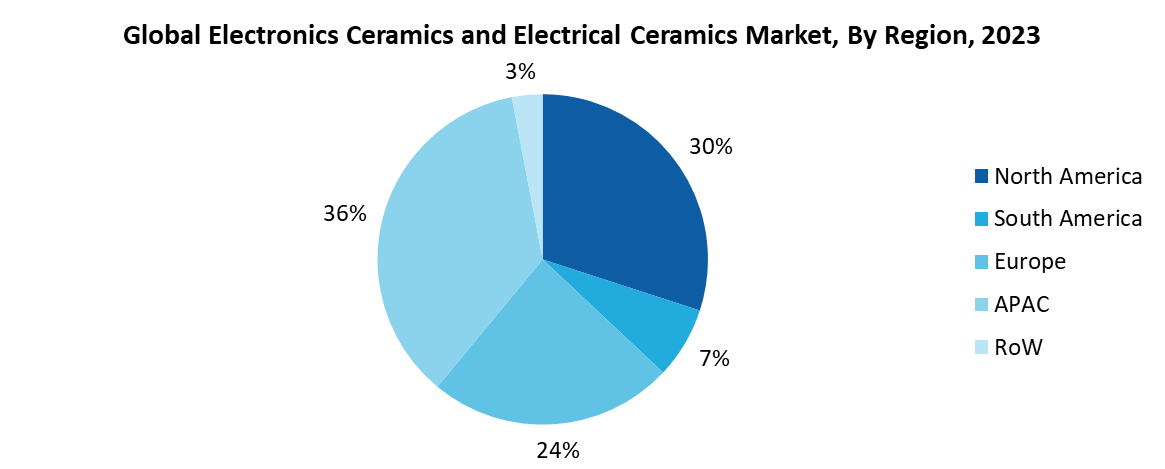

- Asia-Pacific dominates the Electronics Ceramics and Electrical Ceramics market owing to increasing demand from applications from industries such as automotive, electronics, energy & power.

- Increase in demand of Electronics products, is likely to aid in the market growth of Electronics Ceramics and Electrical Ceramics.

- Stringent Governments’ regulations towards digitalization will further enhance the market growth of Electronics Ceramics and Electrical Ceramics.

- High cost and technical complexity in manufacturing and deposition of the ceramics are likely to negatively affect the Electronics Ceramics and Electrical Ceramics market.

Electronics Ceramics and Electrical Ceramics Market Segment Analysis - By Product

Dielectric ceramic segment dominated the Electronics Ceramics and Electrical Ceramics with a market share of approximately 35% in 2023. Dielectric ceramics are widely used in the manufacturing of capacitors. Capacitors store and release electrical energy by utilizing the electrical properties of dielectric materials placed between conducting plates. Dielectric ceramics, with their high dielectric constants, enhance the capacitance and energy storage capacity of these components and is driven by applications in telecommunications and electronic devices. As the electronics industry continues to advance, there is an increasing need for compact and high-performance components. Dielectric ceramics contribute to the miniaturization of electronic devices while maintaining or improving their efficiency. They are employed in resonators, filters, and oscillators, supporting the stable and reliable operation of electronic systems.

Electronics Ceramics and Electrical Ceramics Market Segment Analysis - By End Use

Electronics segment of Electronics Ceramics and Electrical Ceramics Market is projected to reach a highest CAGR of 5.5% during the forecast period 2024-2030. Electronics Ceramics and Electrical Ceramics, with their unique electrical properties such as piezoelectricity, ferroelectricity, and high dielectric constants, serve as essential components in numerous electronic applications. Capacitors, one of the fundamental building blocks in electronic circuits, heavily rely on Electronics Ceramics and Electrical Ceramics, particularly dielectric ceramics. The capacitors manufactured with Electronics Ceramics and Electrical Ceramics find applications in virtually all electronic devices, including smartphones, computers, televisions, and industrial electronics. As the electronics industry continues to evolve with advancements in consumer electronics, communication technologies, and emerging fields like the Internet of Things (IoT), the demand for Electronics Ceramics and Electrical Ceramics remains robust.

Electronics Ceramics and Electrical Ceramics Market Segment Analysis - By Geography

Geographically, in the global Electronics Ceramics and Electrical Ceramics Market share, APAC is analyzed to grow with a market share of 40% in 2023, as Electronics Ceramics and Electrical Ceramics are mostly used in the electronics products. Countries such as Taiwan, South Korea, China among with others are the largest market in the APAC region for Electronics Ceramics and Electrical Ceramics market as, these countries are the largest electronics market. Huawei, a Chinese company, has submitted most 5G-related patent applications. China Mobile, China Telecom, and China Unicom, three state-backed operators, started 5G services in major Chinese cities. Because most of the population works from home due to the epidemic, businesses must have access to high-speed internet to operate efficiently. As more individuals opt for 5G networks, the requirement for electronic ceramic-based 5G infrastructure becomes inevitable.

Electronics Ceramics and Electrical Ceramics Market Drivers

Growing Demand for Electronic Devices and Components

The increasing reliance on electronic devices and components across various industries is a primary driver for the Electronics Ceramics and Electrical Ceramics market. With the surge in consumer electronics, automotive technologies, and the Internet of Things (IoT), there is a heightened demand for advanced electronic components. Electronics Ceramics and Electrical Ceramics, known for their electrical and thermal properties, play a crucial role in manufacturing capacitors, sensors, and other essential electronic components. As consumers seek more powerful, compact, and energy-efficient devices, the demand for Electronics Ceramics and Electrical Ceramics continues to grow. This trend is further fueled by innovations in telecommunications, healthcare, and smart infrastructure, where Electronics Ceramics and Electrical Ceramics contribute to the development of cutting-edge technologies.

Stringent Government Regulations

Stringent government regulations serve as a significant market driver for the Electronics Ceramics and Electrical Ceramics industry. Governments worldwide are enforcing regulations aimed at enhancing energy efficiency, reducing environmental impact, and ensuring product safety. Electronics Ceramics and Electrical Ceramics, with applications in energy-efficient devices, electronic vehicles, and renewable energy systems, align with these regulatory initiatives. Mandates promoting the use of eco-friendly materials and technologies drive the adoption of Electronics Ceramics and Electrical Ceramics in compliance with environmental standards. Additionally, regulations emphasizing the importance of reliable and high-performance electronic components contribute to the market's growth, fostering innovation and the development of advanced electroceramic materials that meet or exceed regulatory requirements. The interplay between regulatory compliance and technological advancements positions Electronics Ceramics and Electrical Ceramics as a key player in the modern electronics landscape.

Electronics Ceramics and Electrical Ceramics Market Challenges

High Cost and Technical Complexity

The intricate manufacturing processes involved in producing high-quality electroceramic components contribute to elevated production costs, limiting their widespread adoption. Moreover, the technical complexity associated with designing and implementing Electronics Ceramics and Electrical Ceramics in various applications poses barriers for smaller enterprises and may hinder market growth. Research and development efforts to enhance manufacturing efficiency and reduce costs are crucial for addressing this challenge. Additionally, the need for specialized knowledge and expertise in handling electroceramic materials may further impede market expansion. Overcoming these obstacles requires collaborative efforts from industry stakeholders to streamline production processes, invest in skill development, and explore cost-effective alternatives, ultimately fostering a more accessible and economically viable Electronics Ceramics and Electrical Ceramics market.

Electronics Ceramics and Electrical Ceramics Industry Outlook

Product launches, acquisitions, Partnerships and R&D activities are key strategies adopted by players in the Electronics Ceramics and Electrical Ceramics Market. Electronics Ceramics and Electrical Ceramics top 10 companies include:

- TDK Corporation

- CoorsTek Inc.

- Murata Manufacturing Co. Ltd.

- Kyocera Corporation

- Taiyo Yuden

- National Magnetics Group, Inc.

- Electro Ceramics Co. Ltd.

- NTK Ceratec Co. Ltd.

- Morgan Advanced Materials

- PI Ceramic GmbH

Recent Developments

- At COMPAMED 2023 event, PI Ceramic GmbH, the focus of PI Ceramic will be on piezo solutions for microfluidics and it has presented the extensive solution potential of piezoceramics for microfluidic applications.

- In October 2023, Electro Ceramic Industries is expanding its product offering to provide customers with a wider range of electronic packaging solutions. They have announced the recent acquisition of United Glass to Metal Sealing, Inc.

- In August 2023, Ceramic Technologies - Integral Molding with Complex Internal Shape: "F-Molding" is a new molding method developed by Kyocera that achieves a large near-net shape by pouring a slurry of raw materials into a mold.

For more Chemicals and Materials Market reports, please click here

1. Electronics Ceramics and Electrical Ceramics Market - Overview

1.1. Definitions and Scope

2. Electronics Ceramics and Electrical Ceramics Market - Executive Summary

3. Electronics Ceramics and Electrical Ceramics Market - Comparative Analysis

3.1. Company Benchmarking - Key Companies

3.2. Global Financial Analysis - Key Companies

3.3. Market Share Analysis - Key Companies

3.4. Patent Analysis

3.5. Pricing Analysis

4. Electronics Ceramics and Electrical Ceramics Market - Start-up Companies Scenario

4.1. Key Start-up Company Analysis by

4.1.1. Investment

4.1.2. Revenue

4.1.3. Venture Capital and Funding Scenario

5. Electronics Ceramics and Electrical Ceramics Market – Market Entry Scenario Premium

5.1. Regulatory Framework Overview

5.2. New Business and Ease of Doing Business Index

5.3. Case Studies of Successful Ventures

6. Electronics Ceramics and Electrical Ceramics Market - Forces

6.1. Market Drivers

6.2. Market Constraints

6.3. Market Challenges

6.4. Porter's Five Force Model

6.4.1. Bargaining Power of Suppliers

6.4.2. Bargaining Powers of Customers

6.4.3. Threat of New Entrants

6.4.4. Rivalry Among Existing Players

6.4.5. Threat of Substitutes

7. Electronics Ceramics and Electrical Ceramics Market – Strategic Analysis

7.1. Value Chain Analysis

7.2. Opportunities Analysis

7.3. Market Life Cycle

8. Electronics Ceramics and Electrical Ceramics Market – by Product (Market Size – $Million/$Billion)

8.1. Dielectric ceramics

8.2. Ceramic insulators

8.3. Piezoelectric ceramics

8.4. Ferroelectric Ceramics

9. Electronics Ceramics and Electrical Ceramics Market – by Application (Market Size - $Million/$Billion)

9.1. Capacitors

9.2. Data Storage Devices

9.3. Optoelectronic Devices

9.4. Actuators and Sensors

9.5. Powder Distribution Devices

9.6. Others.

10. Electronics Ceramics and Electrical Ceramics Market – by End Use (Market Size – $Million/$Billion)

10.1. Automotive

10.2. Electronics

10.3. Energy and Power

11. Electronics Ceramics and Electrical Ceramics Market – by Geography (Market Size – $Million/$Billion)

11.1. North America

11.1.1. Canada

11.1.2. Mexico

11.1.3. U.S

11.2. South America

11.2.1. Argentina

11.2.2. Brazil

11.2.3. Chile

11.2.4. Colombia

11.2.5. Rest of South America

11.3. Europe

11.3.1. France

11.3.2. Germany

11.3.3. Italy

11.3.4. Netherlands

11.3.5. Russia

11.3.6. Spain

11.3.7. UK

11.3.8. Rest of Europe

11.4. APAC

11.4.1. Australia

11.4.2. China

11.4.3. India

11.4.4. Taiwan

11.4.5. Japan

11.4.6. Malaysia

11.4.7. South Korea

11.4.8. Rest of APAC

11.5. RoW

11.5.1. Africa

11.5.2. Middle East

12. Electronics Ceramics and Electrical Ceramics Market – Entropy

13. Electronics Ceramics and Electrical Ceramics Market – Industry/Segment Competition Landscape

13.1. Market Share Analysis

13.1.1. Market Share by Region – Key Companies

13.1.2. Market Share by Country – Key Companies

13.2. Competition Matrix

13.3. Best Practices for Companies

14. Electronics Ceramics and Electrical Ceramics Market – Key Company List by Country Premium

15. Electronics Ceramics and Electrical Ceramics Market - Company Analysis

15.1. TDK Corporation

15.2. CoorsTek Inc.

15.3. Murata Manufacturing Co. Ltd.

15.4. Kyocera Corporation

15.5. Taiyo Yuden

15.6. National Magnetics Group, Inc.

15.7. Electro Ceramics Co. Ltd.

15.8. NTK Ceratec Co. Ltd.

15.9. Morgan Advanced Materials

15.10. PI Ceramic GmbH

"Financials to the Private Companies would be provided on best-effort basis."