Email

Email Print

Print

Cider Market Overview

The Cider Market size is estimated to be $17.6 billion by 2030 growing at a CAGR of 4.6% over the forecast period of 2024-2030. Cider is often known as an alcoholic drink or a beverage made from different apples, and now various fruits have also been bought into the mix to make the offerings diverse. Cider is produced on similar lines to that of wine. The fruits are bought in from the cultivars whereby they are scratted and pressed. The process of fermentation allows the conversion of simple sugars into ethanol using yeasts. Thus, cider most commonly is also referred to as “fermented fruit juice.” Conversely, any many popular cultures, cider is covertly used in places of beer or malt beverage. Furthermore, it exhibits antioxidant properties, and the fruits selected for making ciders are usually bitter and rich in tannins. The rising adoption of millennials to adapt to healthy alcoholic beverages in their daily routines, along with product manufacturers' varied product offerings, is one of the key factors driving the cider industry forward during the forecast period of 2024-2030.

One prominent trend shaping the cider market is the relentless pursuit of flavor innovation. Cider producers are continually pushing boundaries, introducing a diverse array of fruit-infused and exotic flavor profiles to captivate consumers. The traditional apple-centric approach has expanded to include unique combinations such as berries, citrus, and spices, appealing to adventurous taste preferences. This trend not only caters to the evolving palate of consumers but also fosters a dynamic and competitive market where producers strive to offer distinctive and memorable cider experiences. The emphasis on flavor innovation reflects the industry's commitment to staying ahead of consumer expectations and embracing creativity in product development. A significant trend in the cider market is the growing demand for low and no-alcohol alternatives. As consumers prioritize health-conscious choices and seek refreshing beverages with reduced alcohol content, the cider industry responds with a variety of low-alcohol and alcohol-free options. Brands are introducing innovative cider variants that maintain the crisp and flavorful characteristics of traditional ciders while catering to a broader consumer base. This trend aligns with the broader movement towards mindful drinking and offers consumers the freedom to enjoy the distinct taste of cider without the higher alcohol content, reflecting the industry's adaptability to shifting consumer preferences.

Cider Market Report Coverage

The report: “Cider Market Forecast (2024-2030)”, by Industry ARC covers an in-depth analysis of the following segments of the Cider Market.

By Product Type- Dry Cider, Hard Cider, Soft Cider, Sweet Cider, and Others.

By Packaging Type – Glass Bottles, Plastic Bottles, Aluminium Cans, and Others.

By Source- Organic and Conventional.

By Flavour – Apple Base and Flavoured Ciders.

By Distribution Channel – Hypermarkets, Supermarkets, Specialty Stores, Online Retail, and Others.

By Alcohol Content- 1.2-8.5% ABV, 0.5%-1.2% ABV, and <0.5%ABV.

By Geography- North America (U.S., Canada, Mexico), Europe (Germany, United Kingdom (U.K.), France, Italy, Spain, Russia, and Rest of Europe), Asia Pacific (China, Japan India, South Korea, Australia, and New Zealand, and Rest of Asia Pacific), South America (Brazil, Argentina, and Rest of South America), and Rest of the World (the Middle East, and Africa)

Key Takeaways

• Geographically, Europe’s Cider Market held a dominant market share in the year 2023. This is due to the high regional adoption of the following alcoholic beverages; moreover, the UK is constituted as the largest cider consumer in the world. However, Asia-Pacific shows lucrative growth opportunities owing to a cultural shift being adopted by health-conscious consumers.

• The adoption of millennials to fruit alcoholic beverages is one of the leading market drivers. However, the market addresses colossal competition within the product categories, thereby posing a grave challenge.

• Detailed analysis of the Strengths, Weaknesses, and Opportunities of the prominent players operating in the market will be provided in the Cider Market report.

For More Details on This Report - Request for Sample

For More Details on This Report - Request for Sample

Cider Market Segment Analysis- By Source

The Cider Market based on the source can be further segmented into organic and conventional. Conventional cider had the largest market share in the year 2023. It is owing to the age-old practices of producing cider. Moreover, cider is procreated from the apple. However, apple harvest time is often long, and hence the cultivars use pesticides and other synthetics to make the production fall in line with cider demand. Moreover, the trade practices followed are not fair. Additionally, conventional cider costs substantially less than organic ones.

However, the organic sub-segment is estimated to be the fastest-growing, with a CAGR of 4.9% over the forecast period of 2024-2030. It is owing to the sustainable trade practices followed while producing fruits organically, and organically procured fruits and ciders will be largely benefitted. Moreover, organic apples are free from pesticides, and they taste better; thereby, the cider created from such apples will taste elegant and become a leading factor.

Cider Market Segment Analysis- By Packaging Type

The Cider Market based on the packaging type can be further segmented into glass bottles, plastic bottles, and aluminum cans. The aluminum cans segment held a dominant share in the year 2023. It is owing to the ease by which consumers can carry the cider to their homes at ease. Aluminum cans carry an average of 470 ml of cider, and the content is kept at a stable setting due to excellent aluminum chemical properties.

Moreover, the can segment is estimated to be the fastest-growing, with a CAGR of 5.1% over the forecast period of 2024-2030. This is owing to the rising climate awareness amongst the significant populations. Aluminum cans have the physical properties of getting recycled indefinitely, and as per the Aluminium Association, nearly 75% of all aluminum ever produced is still in circulation. Moreover, only 9% of the plastic is in circulation after their make. The following recyclability properties and excellent chemical composition for storage will help this segment grow.

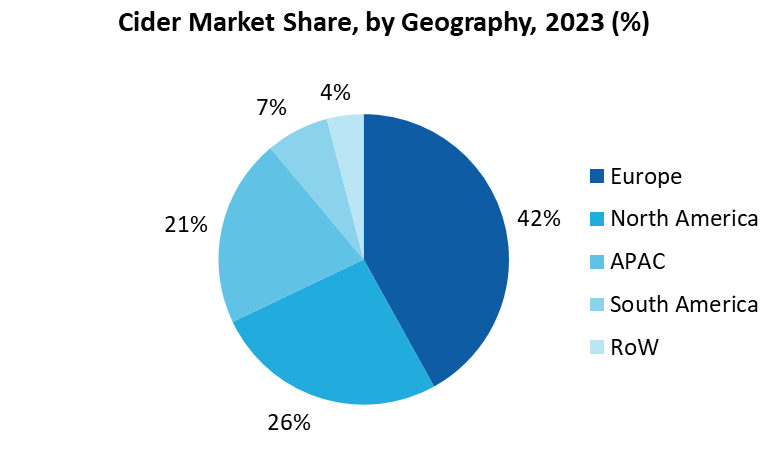

Cider Market Segment Analysis- By Geography

The Cider Market based on Geography can be further segmented into North America, Europe, Asia-Pacific, South America, and the Rest of the World. Europe’s Cider Market held the largest market share of 42% as compared to the other regions. Europe is accounted as the most prominent “apple” producer in the world. Additionally, the region has the highest aggregation hold over the unfermented apple juice. Moreover, the UK accounted for the maximum consumption of 800 million liters of cider in a year.

However, Asia-Pacific shows lucrative growth opportunities for the Cider Market in the projected period. This is owing to the rising prevalence of millennials consuming healthy alcoholic beverages or even preferring- alcoholic drinks such as ciders. Moreover, the region has dynamic preferences which can be fuelled by customizing the apple cider with different fruits.

Cider Market Drivers

Low alcoholic beverages are now gaining traction, which is driving the Cider Market

As the world is recovering from the colossal damage created by the COVID-19 pandemic, it is yet to break free from cardiovascular-related ailments. WHO has regarded such ailments under the category of the silent killer, as more than most of the fatality below the age of 70 is due to such ailments. Moreover, alcohol consumption has strong ties with developing such diseases over time. Hereby, the product offerings made by the Cider Market in terms of “alcohol-free cider” and “low alcohol cider” have gained reasonable traction. Firstly, the former beverage offerings have an ABV of less than 0.5% and hence are known as alcohol-free. Moreover, the low-alcohol cider variant offers an ABV to be less than 1.2%. With such variants present in the market, the interested population is reaping the benefits of cider without gaining any new disease.

Beneficial anti-platelet and anti-inflammatory properties are now propelling people to adopt cider-made beverages

Researchers have readily shown that apple cider is a functional beverage with the presence of bioactive polyphenols. Moreover, the bioactive polyphenols exhibit all the properties of strong anti-platelet activities against the inflammatory and thrombotic lipid mediator PAF. In addition, the PL from all cider product sources was found to be rich in PUFA and especially beneficial in n-3 PUFA, but also MUFA, providing a rationale for their potent anti-inflammatory and anti-platelet properties. Moreover, the presence of polyphenols created a structural analogy, which creates the properties of strong antagonism on various cell receptors.

Cider Market Challenges

The presence of sugar content in cider poses a grave challenge for the market

Firstly, cider weighs lower on the glycemic index when compared to wine as grapes have higher sugar content than most apples. Regardless, the fermented product contains high amounts of sugar. Recent research uncovered that a “natural cider” can of 470 ml contains 20.5 grams of sugar; the following quantity is the only recommended intake of sugar for an adult in a day. Moreover, the quantities of sugar can go up to 5x or 10x as and when the cider is taken in lager or ale. It is a formidable challenge for the Cider Market to address as diabetes is one of the most prevalent cardiovascular issues, and people have changed their food preferences around such indices.

Cider Market Competitive Landscape

Product launches, mergers and acquisitions, joint ventures, and geographical expansions are key strategies adopted by players in the Cider Market. The top Cider Market companies include:

1. Asahi Premium Beverages

2. Aston Manor,

3. C&C Group plc,

4. Carlsberg Breweries A/S,

5. Carlton & United Breweries (CUB)

6. Agrial

7. Heineken UK Limited,

8. The Boston Beer Company

9. Seattle Cider Company

10. Molson Coors Brewing Company

Recent Developments

• In December 2022, Hill Station Hard Cider Ale was Bira 91's first offering in the cider category. According to the growing demand for ready-to-drink products, the company is expanding its product line beyond beers with this introduction.

• In December 2022, Buskey Heritage Blend Cider will be available from Buskey Cider. With a blend of Ruby Red Crab, Ashmead's Kernel, and Gold Rush apples, Buskey Heritage Blend Cider is an off-dry premium cider that is complex, tannic, and full of flavor. It honors the rich Virginian apple legacy.

Relevant Titles

Alcohol Ingredients Market- Forecast (2021-2026)

Report Code- FBR 63780

Denature Alcohol Market- Forecast (2021-2026)

Report Code- FBR 0993

For more Food and Beverage Market reports, please click here

1. Cider Market- Overview

1.1 Definitions and Scope

2. Cider Market- Executive Summary

2.1 Market Revenue, Market Size and Key Trends

2.2 Key Trends by Source

2.3 Key Trends by Type

2.4 Key Trends by Flavor

2.5 Key Trends by Packaging Type

2.6 Key Trends by Distribution Channel

2.7 Key Trends by Alcohol Content

2.8 Key Trends by Geography

3. Cider Market- Comparative Analysis

3.1 Company Benchmarking – Key Companies

3.2 Financial Analysis– Key Companies

3.3 Market Share Analysis– Key Companies

3.4 Patent Analysis

3.5 Pricing Analysis- Average Selling Price

4. Cider Market- Startup Companies Scenario

4.1 Key Startup Company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Venture Capital and Funding Scenario

5. Cider Market– Industry Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Case Studies of Successful Ventures

6. Cider Market- Forces

6.1 Market Drivers

6.2 Market Constraints/Challenges

6.3 Porters Five Force Model

6.3.1 Bargaining power of suppliers

6.3.2 Bargaining powers of customers

6.3.3 Threat of New Entrants

6.3.4 Rivalry among existing players

6.3.5 Threat of Substitutes

7. Cider Market– Strategic Analysis

7.1 Value Chain Analysis

7.2 Opportunities Analysis

7.3 Market Life Cycle

8. Cider Market– By Source (Market Size –$Million/$Billion)

8.1 Organic

8.2 Conventional

9. Cider Market– By Type (Market Size –$Million/$Billion)

9.1 Dry Cider

9.2 Hard Cider

9.3 Soft Cider

9.4 Sweet Cider

9.5 Others

10. Cider Market– By Flavor (Market Size –$Million/$Billion)

10.1 Apple Base

10.2 Flavored Ciders

11. Cider Market– By Distribution Channel (Market Size –$Million/$Billion)

11.1 Hypermarkets

11.2 Supermarkets

11.3 Specialty Stores

11.4 Online Retails

11.5 Others

12. Cider Market- By Packaging Type (Market Size –$Million/$Billion)

12.1 Glass Bottle

12.2 Plastic Bottle

12.3 Aluminum Can

12.4 Others

13. Cider Market- By Alcohol Content (Market Size –$Million/$Billion)

13.1 1.2-8.5% ABV

13.2 0.5%-1.2% ABV

13.3 <0.5% ABV

14. Cider Market- By Geography (Market Size –$Million/$Billion)

14.1 North America

14.1.1 U.S.

14.1.2 Canada

14.1.3 Mexico

14.2 Europe

14.2.1 U.K.

14.2.2 Germany

14.2.3 France

14.2.4 Italy

14.2.5 Spain

14.2.6 Russia

14.2.7 Rest of Europe

14.3 Asia-Pacific

14.3.1 China

14.3.2 India

14.3.3 Japan

14.3.4 South Korea

14.3.5 Australia & New Zealand

14.3.6 Rest of Asia-Pacific

14.4 South America

14.4.1 Brazil

14.4.2 Argentina

14.4.3 Rest of South America

14.5 Rest of the World

14.5.1 Middle East

14.5.2 Africa

15. Cider Market- Entropy

16. Cider Market– Industry/Segment Competition Landscape

16.1 Market Share Analysis

16.1.1 Global Market Share – Key Companies

16.1.2 Market Share by Region – Key companies

16.1.3 Market Share by Countries – Key Companies

16.1.4 Competition Matrix

16.1.5 Best Practices for Companies

17. Cider Market– Key Company List by Country Premium

18. Cider Market Company Analysis

18.1 Company 1

18.2 Company 2

18.3 Company 3

18.4 Company 4

18.5 Company 5

18.6 Company 6

18.7 Company 7

18.8 Company 8

18.9 Company 9

18.10 Company 10

"*Financials for private companies would be provided on a best efforts basis”.

\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\nCider Market is forecast to grow at 4.6% CAGR during the forecast period 2023-2030.

Cider Market size is estimated to reach $17.6 billion by 2030

Top Companies in the Cider Market are Asahi Premium Beverages,\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\nAston Manor, C&C Group plc,Carlsberg Breweries A/S,\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\nCarlton & United Breweries (CUB)\\\\\\\\\\\\\\\\r\\\\\\\\\\\\\\\\nAgrial, Heineken UK Limited, The Boston Beer Company ,Seattle Cider Company, Molson Coors Brewing Company