Email

Email Print

Print

Satellite Communication Market- By Technology, By Communication Network, By Satellite Services , By Communication Equipment , By End User , Government & Military (Space Agencies, Defence, Academic Research & others)), By Geography - Global Opportunity Analysis & Industry Forecast, 2024-2030

Satellite Communication Market Overview

The Market for Satellite Communication is projected to reach $15.18 billion by 2030, progressing at a CAGR of 9.4% from 2024 to 2030. Satellite communication refers to the transmission of data, voice, and video signals using artificial satellites as relay stations. This technology enables communication over long distances, including areas where traditional terrestrial communication infrastructure is unavailable or impractical. Satellite communication systems typically involve the use of ground stations to uplink data to orbiting satellites, which then downlink the data to other ground stations or directly to end-users. These systems are employed in various applications, including telecommunications, broadcasting, navigation, remote sensing, and military operations. The rising demand for various applications such as audio broadcasting and voice communications in end-user industries is analyzed to fuel the growth of the satellite communication industry. The significant adoption of direct-to-home (DTH) in media and entertainment applications is set to positively impact the growth of the market as satellite communication plays a crucial role in communication in providing subscribers with high-quality content. An increase in the use of High Throughput Satellite (HTR) and Low Earth Orbit Satellite for high-speed broadcasting satellite services, cellular backhaul, and other value-added services such as video conferencing, VOIP is set to be the major driver for the growth of the market. The rising adoption of satellite telemetry, automatic identification systems, and Very Small Aperture Terminal markets with improved uplink frequency will drive the market growth.

Report Coverage

The report based on: “Satellite Communication Market – Forecast (2024-2030)”, by IndustryARC covers an in-depth analysis of the following segments.

By Technology: Satellite Telemetry, AIS, VSAT and Others.

By Communication Network: Satellite Internet Protocol Terminals, Gateways, Modems and others.

By Satellite Services: FSS, BSS, MSS, RNSS, Metrological Satellite Services, SBS, RSS.

By Communication Equipment: Network Equipment, Consumer Devices.

By End User: Commercial (Power and Utilities, Maritime, Mining, Healthcare, Telecommunication & others), Government & Military (Space Agencies, Defence, Academic Research & others).

By Geography: North America (U.S, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, and Others), APAC (China, Japan India, South Korea, Australia and Others), South America (Brazil, Argentina and others), and ROW (Middle East and Africa).

Key Takeaways

- Media and Entertainment is set to dominate the satellite communication market owing to the rising demand from a growing population. This is mainly attributed to the increasing demand for the internet and online streaming services such as Amazon Prime Video, Netflix and so on.

- North America has dominated the market share in 2023, however APAC is analysed to grow at highest rate during the forecast period due to the high implementation of 5G in the mobile broadband technologies.

- Deployment of 5G, requiring high bandwidth for communication is set to drive the market during the forecast period 2024-2030.

For more details on this report - Request for Sample

Satellite Communication Market Segment Analysis - by Satellite Services

Satellite services is segmented into fixed satellite services, broadcasting satellite services, mobile satellite services, radio navigation satellite services and others. Mobile satellite services is analyzed to hold the highest share in the satellite communication market in 2023 at 39.1% majorly attributed to the high number of subscribers. There are majorly deployed in aeronautical, land, and maritime services for communication thereby contributing to the growth of the market. For instance, SpaceX's Starlink aims to roll out a commercial satellite-to-phone service in 2024, starting with SMS, then expanding to voice, data, and IoT connectivity by 2025. Advertising on their website, they emphasize compatibility with unaltered LTE phones for setup. In November 2023, The Indian Space Research Organization (ISRO) and NASA are launched a collaborative Earth observation satellite in the first quarter of the upcoming year, as confirmed by the deputy minister for science and technology.

Satellite Communication Market Segment Analysis - by End User

Media and Entertainment segment is set to dominate the market in 2023 at 25.9%. The significant rise in usage of services like Netflix, Amazon Prime Video, YouTube and so on for entertainment is set to contribute to the growth of the market. Adding to this, the breakout of COVID-19 has led to the high traffic in entertainment applications due to lockdowns implemented in various countries. This is set to be a major contributing factor for increasing demand for higher bandwidths resulting in the growth of the market during the forecast period. The Telecom and IT segment is analysed to grow at significant rate during the forecast period, majorly attributed to the deployment of technologically advanced internet connectivity solutions in the majority of the firms. All these factors are together impacting the growth of the satellite communication market. As a result, growing the demand for satellite services continues to surge across various sectors, driven by advancements in communication technology and expanding applications

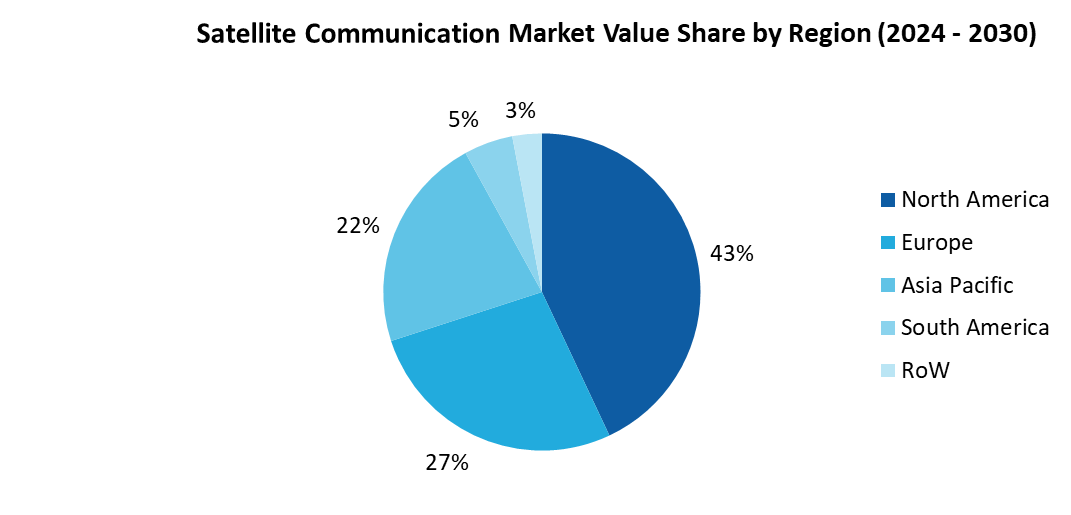

Satellite Communication Market by Geography - Segment Analysis

North America is analyzed to be the dominant region in 2023 at 43%, followed by APAC and Europe. This is mainly attributed to the high adoption of advanced technologies in the region alongside the large infrastructural development for the implementation of high broadband services. APAC is anticipated to showcase the highest growth rate during the forecast period 2024-2030. This is majorly due to the high number of satellite launches aimed at communication. For instance, India launched GSAT-24, a communication satellite, in mid-2022. The satellite is built by ISRO for NewSpace India Limited (NSIL), a government company under the Department of Space. GSAT-24 is a 24-ku band satellite that weighs 4180 kg. Adding to this, the development of advanced technologies in countries such as China and South Korea is set to elevate the market growth rate. In December 2023, China became a pioneering force in 5G, boasting over 3 million base stations and extending services to 750 million mobile users and 17,000 factories. This technological advancement solidifies China's position as a global leader in both the deployment and commercialization of 5G infrastructure. These factors are set to boost the market growth during the forecast period 2024-2030.

Satellite Communication Market Drivers

Growing demand for Maritime Satellite Communication

The increasing demand for maritime satellite communication is significantly set to contribute to the growth of the market. The growing concern for the safety of the people at the borders is creating a dire need for communication. This is set to impact the growth of the maritime communication satellite market. In February 2022, The Russian Satellite Communications Company (RSCC) 's maritime VSAT network expanded to 400 vessels, including 373 sea-going and river ships, along with 27 ice-class ships, including 12 icebreakers. This marks a significant milestone for the Russian Satellite Communications Company in providing connectivity to maritime fleets. This is mainly attributed to providing satellite Automatic Identification System (AIS) data used for ship tracking and specific maritime projects.

Increased Investments for Deployment of 5G

The rise in demand for the 5G and the rising investments for the infrastructure development is to boost the wireless connectivity market. However, the deployment of 5G requires high bandwidth resulting in the launch of satellites thereby contributing to the growth of the satellite communication market. In 2022, For the deployment of 5G, SpaceX has received approval to launch nearly 12,000 starlink internet satellites. Therefore, the launch of these satellites is set to drive the satellite communication market.

Satellite Communication Market Challenges

Space Debris Hindering Launch of Satellites

The presence of space debris is set to pose severe challenges to the communication satellite market. In 2022, the ESA's Space Environment Report reported that over 30,000 pieces of space debris have been recorded and are regularly tracked by space surveillance networks. Space debris poses a significant threat, hindering satellite launches due to collision risks. This dead satellite is also a liability for other satellites that are on a similar trajectory as it’s a popular spot to deposit communications and surveillance satellites. The presence of dead satellites is resulting in the space debris is posing a severe threat to the various other satellites as well as the environment. These factors are set to hinder the growth of the market.

Satellite Communication Market Landscape

Partnerships, acquisitions, collaboration, technological innovation along with product launches are the key strategies adopted by the players in the Satellite Communication Market. The top players of the market include AsiaSat, Hughes, Bharti Airtel, Space Star Technology, Airbus SE, Thales Group, L3Harris Technologies Inc., Swarm Technologies, Inc., Viasat, Inc., General Dynamics, among others

Acquisitions/Technology Launches/Partnerships

- In September 2022, Hughes Communications India has launched India's first High-Throughput Satellite broadband service, utilizing ISRO's GSAT-11 and GSAT-29 satellites along with Hughes JUPITER™ Platform ground technology. It delivers high-speed connectivity across India, supporting enterprise and government networks, community internet access, SD-WAN solutions, mobile network extension, and satellite internet for small businesses.

- In November 2023, Viasat, Inc. and Skylo Technologies introduced the world's inaugural global direct-to-device (D2D) network, revolutionizing connectivity for consumers, businesses, and governments worldwide. Leveraging Viasat's expertise in satellite communications and Skylo's non-terrestrial network (NTN) services, this partnership unlocks vast potential for direct connectivity.

- In July 2023, the SYRACUSE 4B secure military communications satellite, developed by Airbus and Thales Alenia Space, was triumphantly launched from the Guiana Space Center. This historic event marked the final mission for the Ariane 5, Europe's esteemed heavy launcher.

For more Information and Communications Technology Market reports, please click here

1.1 Definitions and Scope

2. Satellite Communication Market - Executive Summary

2.1 Key Trends by Technology

2.2 Key Trends by Communication Network

2.3 Key Trends by Satellite Services

2.4 Key Trends by Communication Equipment

2.5 Key Trends by End User

2.6 Key Trends by Geography

3. Satellite Communication Market - Comparative Analysis

3.1 Company Benchmarking

3.2 Global Financial Analysis

3.3 Market Share Analysis

3.4 Patent Analysis

3.5 Pricing Analysis

4. Satellite Communication Market - Start-up Companies Scenario

4.1 Key Start-up Company Analysis by

4.1.1 Investment

4.1.2 Revenue

4.1.3 Venture Capital and Funding Scenario

5. Satellite Communication Market – Market Entry Scenario Premium

5.1 Regulatory Framework Overview

5.2 New Business and Ease of Doing Business Index

5.3 Case Studies of Successful Ventures

6. Satellite Communication Market - Forces

6.1 Market Drivers

6.2 Market Constraints/Challenges

6.3 Porter’s Five Force Model

6.3.1 Bargaining power of suppliers

6.3.2 Bargaining powers of customers

6.3.3 Threat of new entrants

6.3.4 Rivalry among existing players

6.3.5 Threat of substitutes

7. Satellite Communication Market – Strategic Analysis

7.1 Value Chain Analysis

7.2 Opportunities Analysis

7.3 Market Life Cycle

8. Satellite Communication Market– By Technology (Market Size -$Million/Billion)

8.1 Satellite Telemetry

8.2 Automatic Identification Systems (AIS)

8.3 Very Small Aperture Terminal (VSAT)

8.4 Others

9. Satellite Communication Market– By Communication Network (Market Size -$Million/Billion)

9.1 Satellite Internet Protocol Terminals

9.2 Gateways

9.3 Satellite Modems

9.4 Others

10. Satellite Communication Market– By Satellite Services (Market Size -$Million/Billion)

10.1 Fixed Satellite Service (FSS)

10.2 Broadcasting Satellite Service (BSS)

10.3 Mobile-Satellite Service (MSS)

10.4 Radio navigation-Satellite Service

10.5 Metrological-Satellite Service

10.6 Satellite Broadband Service

10.7 Remote Sensing Services

11. Satellite Communication Market – By Communication Equipment (Market Size -$Million/Billion)

11.1 Network Equipment

11.1.1 Earth Station Antennas Systems

11.1.2 Frequency and Baseband Equipment

11.1.3 Modems

11.1.4 Multiplexing

11.1.5 Packet Processing

11.2 Consumer Devices

11.2.1 Satellite TV Dishes

11.2.2 Satellite Radio Equipment

11.2.3 Satellite Broadband Dishes

11.2.4 Others

12. Satellite Communication Market – By End Users (Market Size -$Million/Billion)

12.1 Media & Entertainment

12.2 Aviation

12.3 Retail

12.4 Telecom & IT

12.5 Tele-Education

12.6 Marine

12.7 Transportation

12.8 Others

13. Satellite Communication Market – By Geography (Market Size - $Million/$Billion)

13.1 North America

13.1.1 U.S.

13.1.2 Canada

13.1.3 Mexico

13.2 Europe

13.2.1 U.K.

13.2.2 Germany

13.2.3 France

13.2.4 Italy

13.2.5 Rest of Europe

13.3 Asia-Pacific

13.3.1 China

13.3.2 Japan

13.3.3 India

13.3.4 South Korea

13.3.5 Australia & New Zealand

13.3.6 Rest of Asia-Pacific

13.4 South America

13.4.1 Brazil

13.4.2 Argentina

13.4.3 Chile

13.4.4 Rest of South America

13.5 Rest of The World

13.5.1 Middle East

13.5.2 Africa

14. Satellite Communication Market - Entropy

15. Satellite Communication Market – Industry/Segment Competition Landscape

15.1 Market Share Analysis

15.1.1 Global Market Share – Key Companies

15.1.2 Market Share by Region – Key Companies

15.1.3 Market Share by Countries – Key Companies

15.2 Competition Matrix

15.3 Best Practices for Companies

16. Satellite Communication Market – Key Company List by Country Premium

17. Satellite Communication Market- Company Analysis

17.1 AsiaSat

17.2 Hughes

17.3 Bharti Airtel

17.4 Space Star Technology

17.5 Airbus SE

17.6 Thales Group

17.7 L3Harris Technologies Inc.

17.8 Swarm Technologies, Inc.

17.9 Viasat, Inc.

17.10 General Dynamics

* "Financials would be provided to private companies on best-efforts basis."